Loading

Loading

Global steel scrap prices weakened in the week ended Friday July 3, under pressure from still-fragile finished steel demand and lower appetite from steel mills in the main import markets. The slowdown in rebar sales, the decline in billet prices and the start of the monsoon season in South and Southeast Asia contributed to weighing further on sentiment, pushing several buyers to reduce bids or stay out of the market.

Global steel scrap prices weakened in the week ended Friday July 3, under pressure from still-fragile finished steel demand and lower appetite from steel mills in the main import markets. The slowdown in rebar sales, the decline in billet prices and the start of the monsoon season in South and Southeast Asia contributed to weighing further on sentiment, pushing several buyers to reduce bids or stay out of the market.

The international picture appears increasingly conditioned by a combination of weak demand, broad caution in purchases and the availability of more competitive alternatives to scrap. In several countries, steel mills continue to buy only to cover immediate requirements, avoiding rebuilding inventories in a context in which finished products still do not offer convincing signs of recovery.

The pressure emerged broadly: Turkey continued to book deep-sea cargoes, but at lower prices; US exporters reduced yard buying prices; Vietnam, China, Taiwan and India recorded weaker markets, penalized by slow demand, lower billet offers and contained buying interest.

Turkey: Purchases Still Present, But At Lower Prices

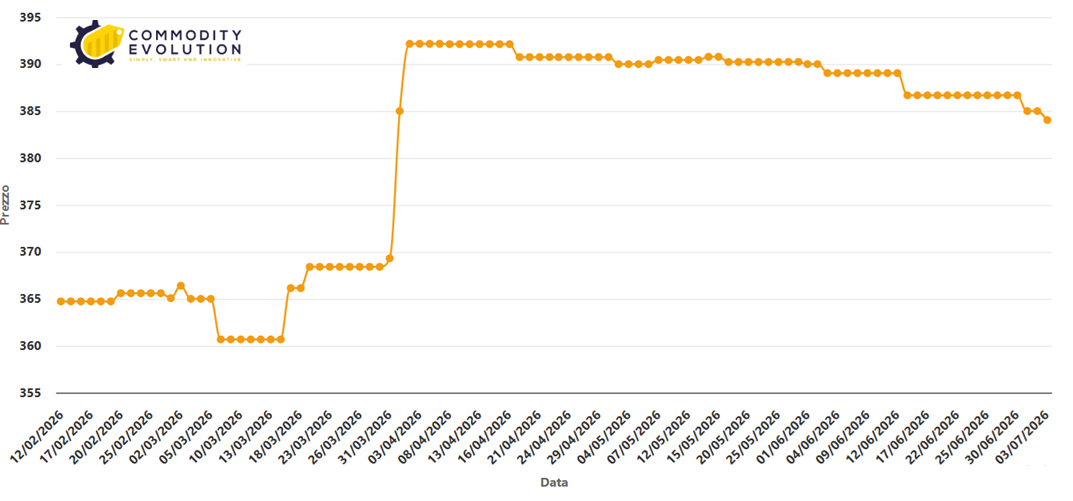

The Turkish deep-sea scrap market continued to show cautious purchases by steel mills in the week to July 3. Several cargoes of heavy melting scrap 1&2, 80:20, were booked in the Marmara and Izmir regions, with origins from the United States, the Baltic Sea, the United Kingdom and Europe.

However, all the agreements were closed at levels lower than the transaction reported on Monday, when a steel mill in Izmir had booked a Baltic Sea cargo of HMS 1&2, 80:20, at $377 per tonne CFR.

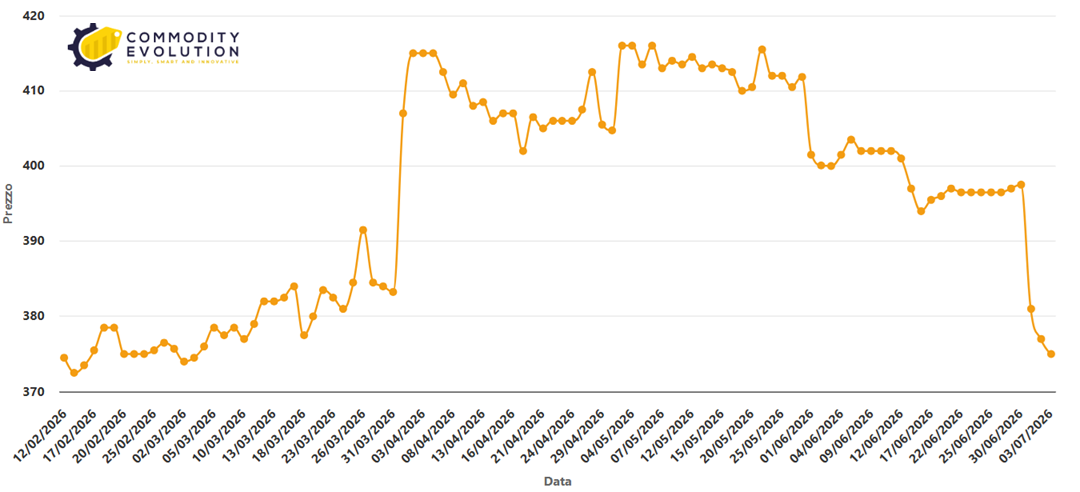

LME Steel Scrap TSI HMS 80:20 CFR – Türkiye $/ton – Powered by Commodity Evolution

Finished steel demand remains the main braking element. The Turkish domestic market and export markets continue to show weak sales, limiting steel mills’ willingness to buy raw material aggressively. At the same time, scrap availability remained sufficient, taking further support away from prices.

In this context, Turkish mills remain active, but with a very selective approach. Producers are trying to keep production covered without bringing purchases too far forward, while weak rebar continues to compress margins and reduce the space for a recovery in scrap.

United States: Exporters Forced To Cut Yard Prices

In the United States, scrap exporters cut their yard buying prices, in a context characterized by the absence of new confirmed deep-sea sales. According to sources, at least four vessels are currently on offer, but no deals have been concluded in almost two weeks.

This lack of activity increased pressure along the US supply chain. Without confirmed export sales, exporters have less room to support domestic collection prices, especially when the main international buyers are aiming to obtain reductions.

Sources expect the next booking to take place at lower levels, consistent with the weaker tone observed in Turkey and Asia. The US market therefore remains exposed to overseas demand: if deep-sea buyers continue to move cautiously, yard prices could face further pressure.

Vietnam: Monsoon And Slow Construction Hold Back The Market

In Vietnam, the scrap market weakened during the week, penalized by monsoon conditions, which interrupted or slowed part of construction activity and reduced steel demand. The seasonal weather had a direct impact on consumption, especially in the construction sector, traditionally one of the main outlets for long products.

Offers for Japanese H2 scrap and for deep-sea bulk material declined, while trades remained limited. Some steel mills returned to the market to buy small containerized cargoes, mainly intended to replenish minimum inventories, but this was not a structural recovery in demand.

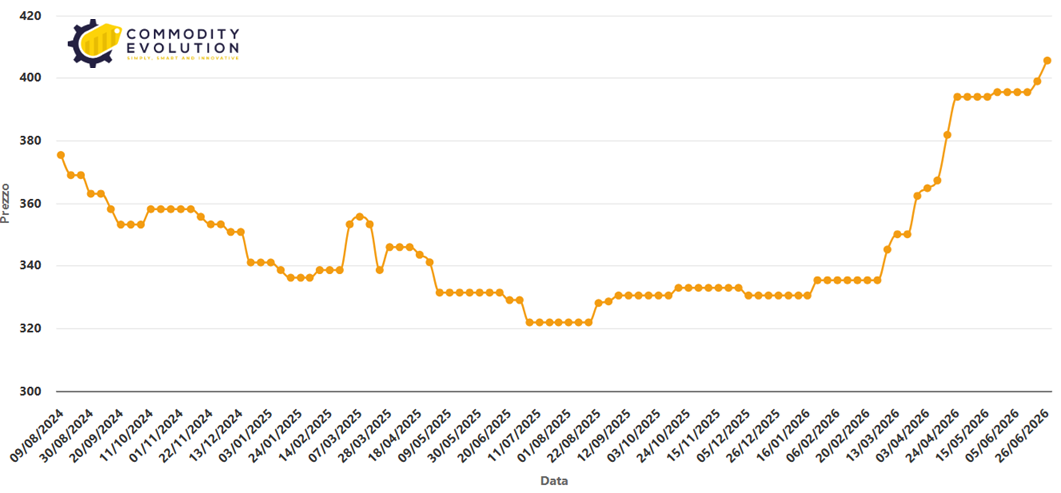

Heavy Steel Scrap Casting HMS I/II 80:20 CFR Vietnam $/ton – Powered by Commodity Evolution

According to some sources, seasonal weakness could continue in the coming months. The combination of monsoon rains, slower construction demand and billet prices under pressure leaves little room for a rapid recovery in imported scrap.

China: Prices Reverse And Purchases Limited To Requirements

In China, imported scrap prices reversed course and declined during June, following the weakening of global markets and greater caution among steel mills. Producers continued to limit purchases to immediate production requirements only, avoiding accumulating material in a phase of weak final demand.

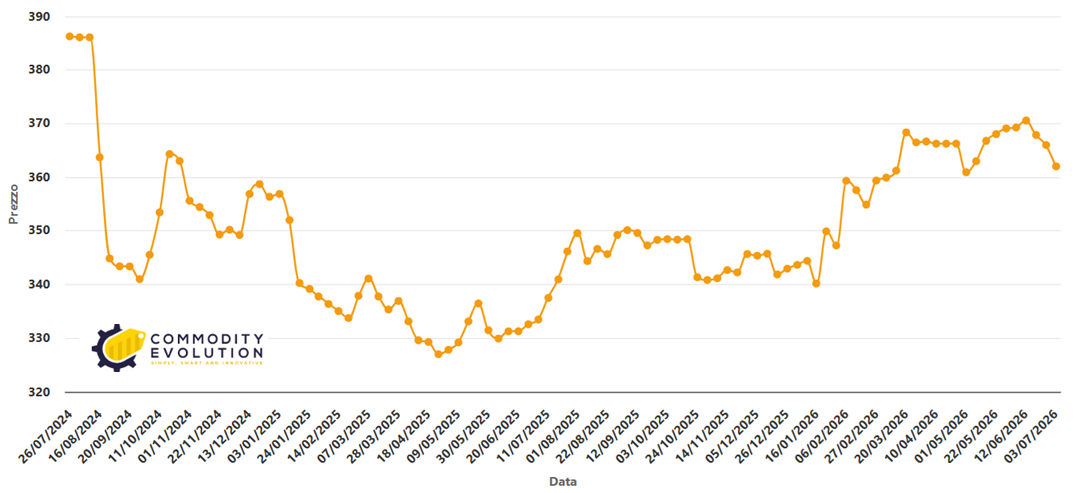

HMS Steel Scrap 8mm min ExW – Wuxi – China $/ton – Powered by Commodity Evolution

The Chinese market remains conditioned by seasonally lower steel demand, reduced margins and greater availability of alternatives to the traditional metallic charge. In particular, expectations of a possible easing of US sanctions on Iranian commodities fueled the idea that Iranian billet could return to regional markets, increasing competition for scrap as a steelmaking raw material.

The possibility of greater supply of billet at competitive prices further reduced appetite for scrap. When billet becomes cheaper, some steel mills may prefer to buy semis instead of increasing the use of scrap, especially if demand for finished products remains weak.

Taiwan: Fourth Week Of Declines For Imports

In Taiwan, imported scrap prices declined for the fourth consecutive week, with bookings of containerized HMS 1&2, 80:20 falling during the week. Pressure came from several fronts: slow rebar sales, lower billet offers from mainland China and weaker sentiment in Turkey.

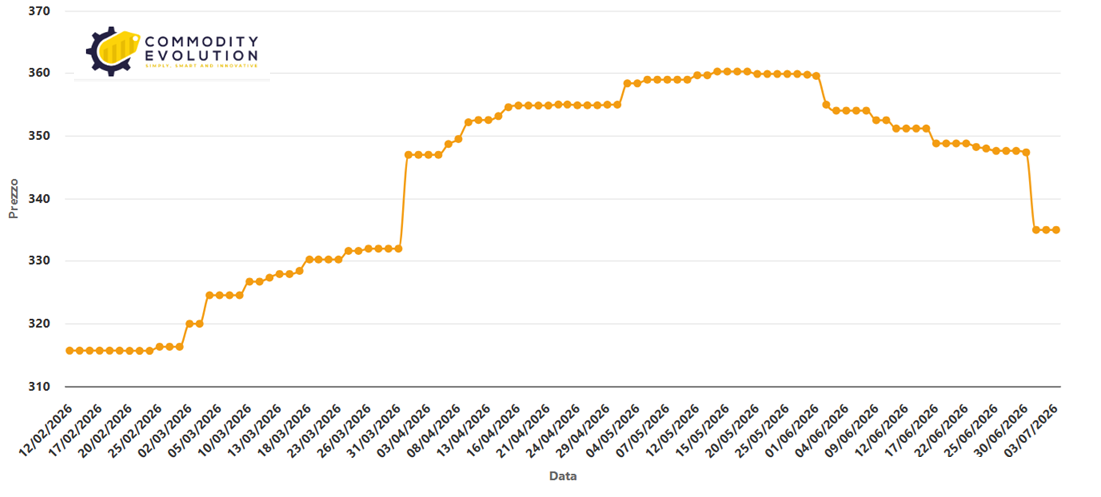

LME Steel Scrap CFR – Taiwan $/ton – Powered by Commodity Evolution

The Taiwanese market is particularly sensitive to the comparison between scrap and billet. When offers of semis fall, steel mills have less urgency to buy imported scrap, especially if margins on finished product sales remain compressed.

The fourth consecutive week of declines therefore confirms a market phase lacking support, in which buyers continue to test lower levels and sellers must decide whether to accept lower prices or wait for an improvement in regional demand.

India: Market Almost Stopped And Bids Too Low For Sellers

In India, the imported scrap market remained largely inactive during the week, with most steel mills silent on fresh offers. The few buyers still present submitted bids considered too low by sellers, preventing a significant recovery in trades.

Only some agreements for small on-arrival containerized shredded scrap cargoes were reported, but overall sentiment remained weak. Weighing on the market were the decline in billet prices, slow rebar demand and the start of the monsoon season, which tends to slow construction activity and therefore steel consumption.

LME Steel Scrap CFR – India $/ton – Powered by Commodity Evolution

The Indian market is therefore in a wait-and-see position. Steel mills have no urgency to buy and prefer to observe the evolution of international prices, while sellers are trying to defend levels that buyers now consider too high compared with actual demand.

Billet Becomes The Main Pressure Factor

One of the most relevant elements of the week was the growing role of billet as an alternative to scrap. In several Asian markets, the decline in semis prices reduced the attractiveness of scrap, especially for steel mills that can choose between different combinations of metallic charge and procurement.

Pressure on billet reflects the weakness of finished steel demand and the possibility of greater regional availability, also in relation to expectations on Iranian commodities. This created a chain effect: cheaper billet means lower willingness by steel mills to pay high prices for scrap, especially in markets where rebar sales are already slow.

For scrap, this competition is particularly problematic because it comes in a phase in which seasonal demand is weak and plants are trying to protect margins. The result is greater pressure on import prices and a more wait-and-see attitude from buyers.

Weak Rebar Demand And Compressed Margins

The common thread across the different markets remains weak rebar demand, which continues to limit steel mills’ appetite for scrap. In Turkey, Asia and India, slow sales of long products are compressing margins and reducing producers’ ability to support higher prices for raw material.

When rebar does not find sufficient demand, steel mills reduce the pace of purchases and try to lower the costs of the metallic charge. This dynamic is becoming evident in almost all major import markets, with direct effects on prices, bids and traded volumes.

In addition, the start of the monsoon season in South and Southeast Asia adds a negative seasonal element. Slower construction sites, lower steel consumption and more complex logistics contribute to further cooling scrap demand, at least in the short term.

A Global Market Seeking A New Balance Point

The global picture for steel scrap therefore remains oriented downward. Turkey continues to buy but only at lower levels, the United States is cutting yard prices, Vietnam is suffering seasonal weakness, China is reducing appetite for scrap, Taiwan is recording its fourth consecutive decline and India remains almost stopped.

The market does not appear to be without trades, but liquidity is selective and dominated by buyers seeking further concessions. Sellers, especially in export markets, must deal with a context in which demand is fragile and alternatives such as billet are becoming more competitive.

For the coming weeks, attention will remain focused on three factors: the next Turkish buying level, the trend in billet offers and the impact of the monsoon season on Asian steel demand. If these elements continue to move unfavorably, global scrap could remain under pressure also in the first part of July, with new declines in the markets most exposed to imports.