Loading

Loading

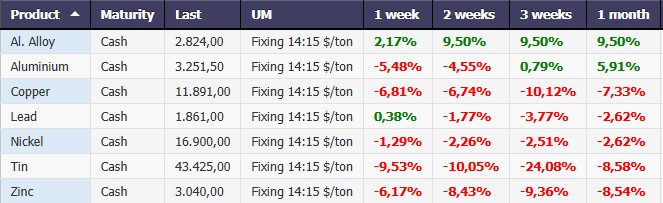

The current evidence is a comprehensive picture for non-ferrous metals listed on the LME, where short-term dynamics are showing mixed signals, but the monthly trend remains clearly negative.

The current evidence is a comprehensive picture for non-ferrous metals listed on the LME, where short-term dynamics are showing mixed signals, but the monthly trend remains clearly negative.

Analyzing performance in dollars, only lead appears to be relatively resilient in the short term (+0.38%), remaining purely negative in the medium term.

In contrast, the rest of the sector’s evidence gives a diffuse impression. Copper, a barometer of the industrial cycle, recorded a significant decline (-6.81% weekly and -7.33% monthly), signaling a weakening of global demand.

The correction in tin (-9.53% weekly, -8.58% monthly) and zinc (-6.17% weekly, -8.54% monthly) was even more pronounced, while nickel continues to operate in a fragile environment, with negative variations across time horizons.

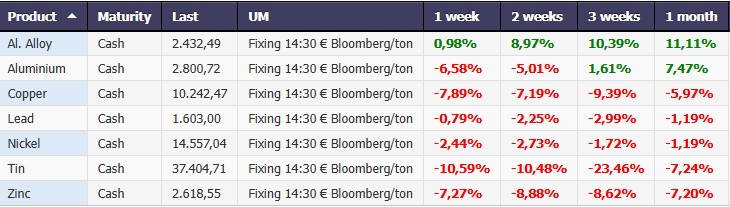

Exchange Rate Effect: Weakness Remains in Euros

The euro reading confirms the general picture, but introduces some nuances related to currency dynamics. Primary aluminum is primarily recovering, evidently compared to the dollar reading (+7.47% monthly), benefiting from the exchange rate effect.

However, weakness remains evident for most metals. Copper continues to decline (-7.89% weekly, -5.97% monthly), as do zinc and tin, which also posted the worst performances in European currencies. Nickel and lead confirm uncertain dynamics, with negative changes reflecting a market lacking momentum.

A Clear Signal: The Industrial Cycle Remains Weak

Overall, the combined dollar and euro reading sends a consistent message: the non-ferrous metals comparison is still under pressure, with a few isolated signs of strength and a general downward trend.

The gains in value are not significant; the trend reversal for most metals indicates that the weakness is structural and tied to the industrial cycle, but this is temporary.

In this context, copper remains the key indicator: its negative performance reinforces the idea of still-fragile global demand, in line with what has also been observed in the steel market.

Performance Metalli Cash $/ton – Powered by Commodity Evolution

Performance Metals Cash €/ton Bloomberg – Powered by Commodity Evolution

European HRC Market Between Apparent Stability and Structural Fragility

The widespread weakness observed in non-ferrous metals is not an isolated phenomenon, but is part of a broader context of a slowdown in the global industrial cycle.

The decline in copper, along with pressure on zinc, nickel, and tin, reflects still-uncertain manufacturing demand. This signal is also reflected in the steel market, where, however, dynamics are manifesting themselves differently.

While the slowdown in non-ferrous metals translates into direct pressure on prices, a more complex pattern emerges in the steel sector: sustained prices despite weak demand.

The global hot-rolled coil (HRC) market is moving in a phase of unstable equilibrium, where prices remain sustained but without real support from demand. Europe, the United States, and China are exhibiting different dynamics, but they share a key element: tension stems from supply and costs, not from a true expansion in consumption.

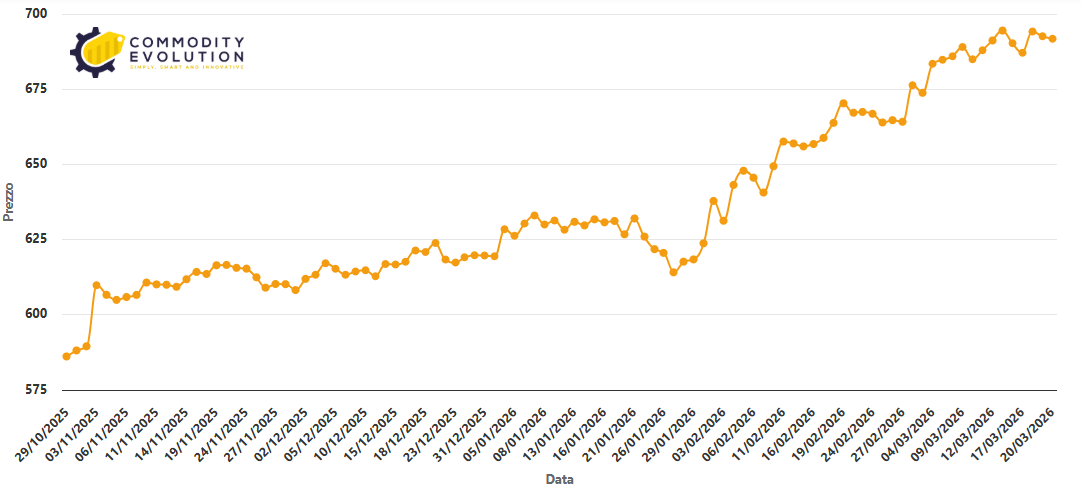

Europe: Prices Supported by Constraints and Costs

In Europe, prices remain in the €690-700/t ex-works range, supported by an increasingly stringent regulatory environment. Defensive measures and the CBAM are progressively reducing the burden of imports, strengthening domestic production.

Added to this are geopolitical tensions impacting energy and logistics, maintaining a high cost structure. However, real demand remains weak, limiting the possibility of further increases and making the market structurally fragile.

HRC Hot Rolled Coils – Northern Europe euro/ton – Powered by Commodity Evolution

Cessi: A Very Tight Market Driven by Costs

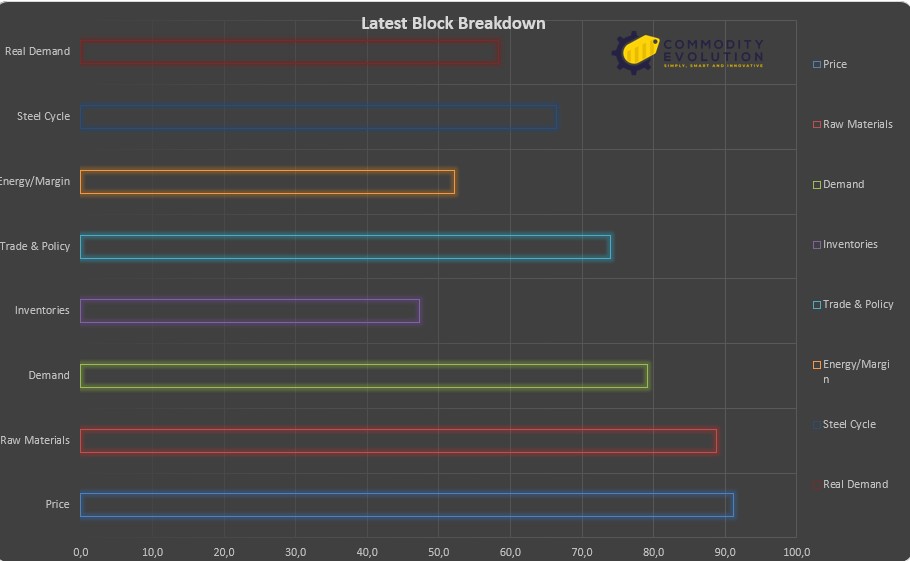

The CESSI (Commodity Evolution Steel Stress Index) model, a proprietary algorithm from Commodity Evolution, confirms this trend. The index stands at 73.0, up from the four-week average (67.8, +7.7%), signaling a “Very Tight” market.

The tension is clearly driven by costs:

- Price Block (91.2) and Raw Materials (88.7) indicate a market strongly anchored to cost-push dynamics.

- Inventories (47.3) highlight low inventories, a key element of rigidity.

- Trade & Policy (74.0) reflects the impact of tariffs and CBAM in compressing supply.

At the same time, signs of weakness are emerging:

- Real Demand (58.3) shows limited effective demand.

- Energy/Margin (52.1) signals compressed margins along the supply chain.

- Steel Cycle (66.4) indicates a cycle under pressure, without real expansion.

The result is a tense but not strong market, where scarcity is partly artificial.

CESSI – Latest Block Breakdown – Powered by Commodity Evolution

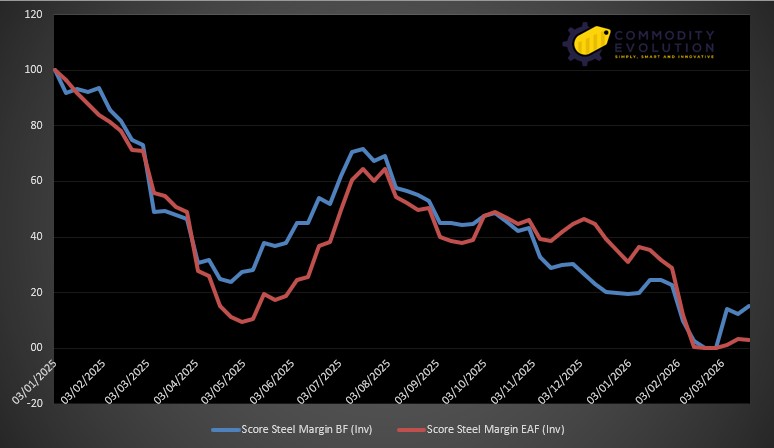

Margins Under Pressure: The Most Critical Signal

The production margin chart adds a key element: the structural compression of profitability.

It is clearly visible that:

- BF (blast furnace) and EAF (electric arc furnace) margins have suffered a sharp decline in 2025;

- after a summer rebound, the trend has returned to negative territory;

- in recent weeks, both production models have shown near-record levels, with EAF particularly under pressure.

This indicates that, despite relatively high prices, the steel industry is operating with extremely compressed margins, consistent with the CESSI Energy/Margin data.

In other words, the market is only partially passing on costs downstream, generating a fragile equilibrium.

CESSI – Score Steel Margin BF- EAF – Powered by Commodity Evolution

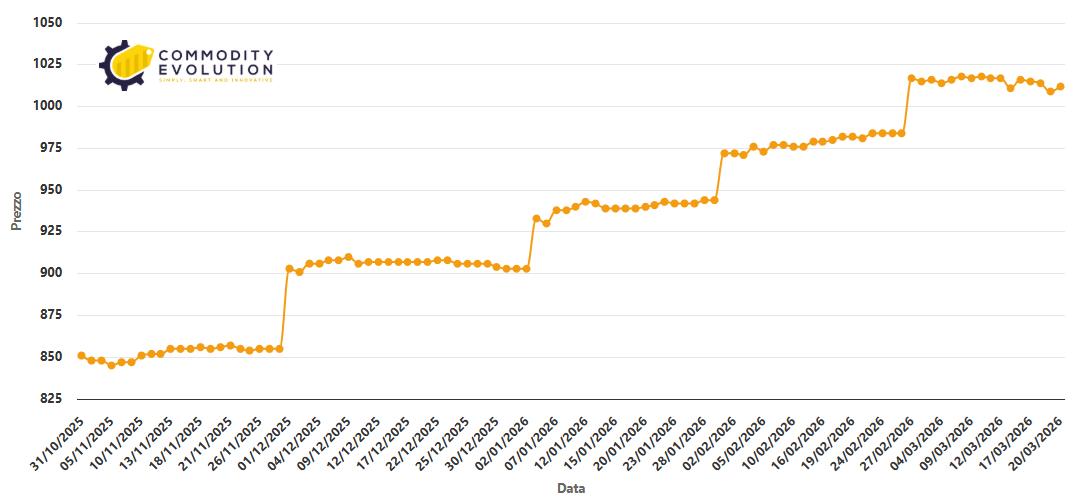

United States: Stabilization After the Rally

In the United States, the market is experiencing a controlled cooling after the strong rally of recent weeks. Prices in the Midwest are hovering around $1,020/ton, down slightly but still elevated.

Here, too, support comes from supply:

- Long-term contracts are reducing spot availability;

- Slab shortages are limiting production;

- Imports remain penalized, with volumes down approximately 50% year-over-year.

Delivery times, between 6 and 12 weeks, confirm a still-tight market, but the loss of momentum highlights how, even in the US, demand is not strong enough to sustain further increases.

HRC Hot Rolled Coils – USA Central West $/ton – Powered by Commodity Evolution

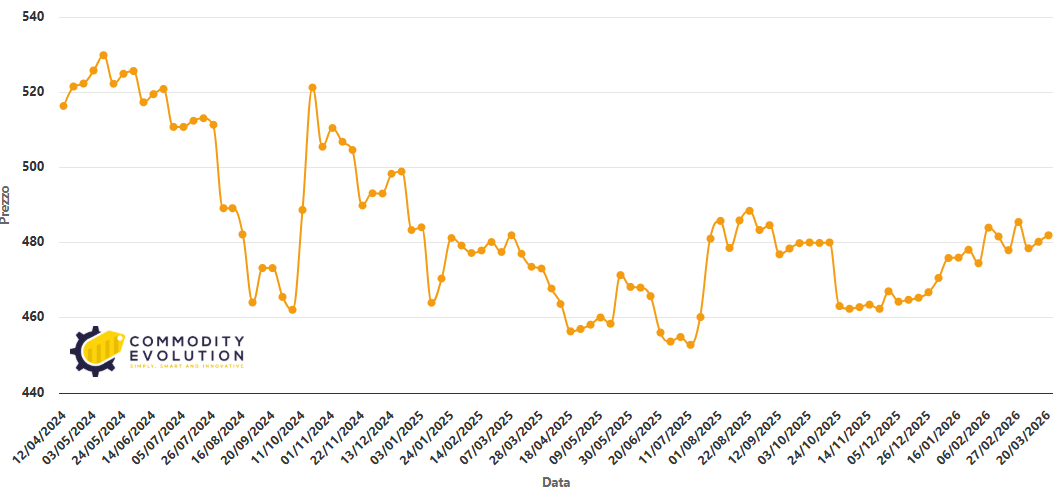

China: Destocking Underway But Weak Demand

In China, the market is in an intermediate phase between destocking and demand uncertainty. Domestic prices are around 3,290–3,300 yuan/t, supported by a reduction in company inventories.

However, demand remains the main source of fragility:

- Operators are purchasing cautiously;

- volumes remain limited;

- visibility is limited.

On the export front, prices are around $483/t FOB, with offers up to $490–500/t, but high logistics costs are holding back competitiveness.

At the same time, the issue of green steel is emerging, with premiums of up to 800 yuan/t, introducing a new structural component in prices linked to the energy transition.

Hot Rolled Coils HRC Q235B 2.75mm In Stock – Shanghai – China $/ton – Powered by Commodity Evolution

Logistics and Energy: Cross-Sector Drivers

A common element across all three markets is the growing impact of logistics and energy costs. The CESSI Freight/Shipping Block (52.6) highlights how tensions on maritime routes are further tightening the market.

These factors reinforce the cost-driven nature of the global steel cycle, reducing trade fluidity and amplifying regional differences.

Conclusions: An Increasingly Unstable Global Balance

The combined reading of CESSI data and the international scenario paints a coherent picture: the HRC market is globally tense but structurally fragile.

- In Europe, prices are supported by regulation and scarcity;

- in the United States, by structural supply constraints;

- in China, by an unstable balance between destocking and weak demand.

The common denominator is clear: demand does not drive the market.

In the short term, the sustainability of this equilibrium will depend on three key variables: geopolitics, energy costs, and the actual recovery of global demand. Without the latter, the risk is that stability will become increasingly fragile and potentially reversible.

For more information on our proprietary CESSI algorithm, contact us at info@commodityevolution.com or support@commodityevolution.com

Commodity Evolution is the ideal solution to support the budgeting and negotiation activities of your corporate purchasing department.

Access to the platform allows you to view real-time prices and comprehensive market information for metals, steel, scrap, and many other sectors, with more than 1,500 products.

Request a Free Demo

Disclaimer

This document was prepared by Commodity Evolution. It is intended for consultation by those to whom it is addressed and, in any case, is not intended to replace the personal judgment of those to whom it is addressed. While Commodity Evolution has taken the utmost care in preparing this document and believes its contents to be reliable, it assumes no responsibility for the accuracy, completeness, or currency of the data and information contained therein or on the resources and data used to prepare it. Consequently, Commodity Evolution declines all liability for errors or omissions. The opinions, forecasts, or estimates contained in this document are expressed exclusively as of the date of this document’s preparation, and there is no guarantee that future results or any other future events will be consistent with the opinions, forecasts, or estimates contained herein. Any information contained in this document may be subject to changes or updates after the date of its preparation, without any obligation to communicate such changes or updates to those to whom this document has previously been distributed. This publication is provided to you for information and illustration purposes only and does not constitute a public offering of financial products or a promotion of investment services and/or activities, either to residents of Italy or to residents of other jurisdictions. Neither Commodity Evolution nor any of its directors, representatives, or employees assumes any liability, in whole or in part, for any damages (including, but not limited to, damages for loss of profits, business interruption, loss of information, or other economic losses of any nature) arising from the use, in any form and for any purpose, of the data and information contained in this document.