Loading

Loading

The military escalation between the United States, Israel and Iran is producing an immediate effect on international logistics chains, with consequences that could become increasingly significant for global trade if the conflict were to last over time.

The military escalation between the United States, Israel and Iran is producing an immediate effect on international logistics chains, with consequences that could become increasingly significant for global trade if the conflict were to last over time.

The attacks carried out over the weekend and the subsequent Iranian response targeting several objectives in the region have in fact generated a series of operational disruptions in maritime routes and international transport.

One of the most critical points concerns the Strait of Hormuz, one of the most strategic maritime passages on the planet. At the beginning of the week at least six tanker vessels located in the strait or in its immediate vicinity were struck by attacks, generating a climate of strong tension for commercial navigation.

The situation effectively led to the closure of the maritime corridor already on Sunday, even though the official announcement by Iranian authorities arrived only the following day.

This maritime passage represents one of the most important arteries for global energy and containerized trade, and any prolonged interruption can have significant impacts on trade flows between Asia, the Middle East and Europe.

In an attempt to keep energy traffic active, the United States administration announced the possibility of providing insurance coverage and naval escorts to tankers crossing the strait. However, several observers in the logistics and maritime sector have expressed doubts about the real feasibility and the speed at which such measures could be implemented.

Container Shipping In Crisis: Carriers Divert Routes

Tensions in the Gulf are already causing significant repercussions also in international container shipping.

One of the most visible signs of the crisis occurred at the port of Jebel Ali in Dubai, the largest container hub in the Middle East. Operations were temporarily suspended after a fire caused by the interception of an aerial attack on Saturday night, although port activities resumed on Monday.

Despite the reopening, the situation remains extremely complex.

With the Strait of Hormuz closed and security risks elevated, the main shipping companies are redesigning trade routes to avoid the region.

Among the main measures adopted are:

-

suspension of new bookings;

-

cancellation of scheduled sailings;

-

diversion of vessels to alternative routes.

Some of the world’s largest container shipping operators have already taken drastic decisions.

For example, Hapag-Lloyd and MSC suspended bookings from Persian Gulf ports and to those destinations, including ports located on the Gulf of Oman side, such as those in the United Arab Emirates and Oman, due to their geographical proximity to the crisis area.

Similarly, CMA CGM decided to temporarily stop accepting all bookings to and from Persian Gulf ports.

The shipping company Maersk, meanwhile, suspended refrigerated cargo shipments to the entire region, as well as bookings departing from India to the Gulf, mainly because of the short transit times that increase operational risk.

However, Maersk is still accepting some general bookings from the Far East, a signal that could indicate a certain degree of optimism about the possibility that the Strait of Hormuz could reopen relatively soon.

Containers Accumulating And Risk Of Congestion In Asian Ports

The decisions of the main shipping companies are already generating delays of uncertain duration for shipments heading toward the Persian Gulf region. The cancellation of several sailings has in fact produced a rapid accumulation of containers destined for the Gulf, with the risk of congestion in origin port terminals.

One of the first signs of pressure on the logistics network concerns India, where containers bound for the Middle East are beginning to accumulate in port yards, increasing the probability of operational congestion in the coming days.

If the situation were to continue, the effects could also extend to other Asian ports, creating logistical bottlenecks that could involve shippers not directly connected to Gulf routes.

Meanwhile, vessels still sailing toward the region are diverting part of their cargo to alternative ports, with the aim of temporarily unloading goods in safer logistical hubs.

Among the main transshipment points used during this phase are:

-

Singapore;

-

Malaysia;

-

Sri Lanka.

These logistical hubs represent some of the most important container redistribution centers in global trade. A similar phenomenon had already occurred during the Red Sea crisis in 2024, when the diversion of flows toward transshipment ports caused severe operational congestion.

This time, however, operators believe the impact could be more contained, thanks to slightly lower traffic volumes and greater port capacity available.

An Impact Still Local But With Global Risks

For now, the effects of the war on the container market remain relatively limited to the Gulf region.

Many logistics operators report that operations in other parts of the world are continuing normally. However, the duration of the conflict represents the main risk factor for the evolution of the situation.

The Strait of Hormuz handles about 2–3% of global container traffic, a share that may appear limited but remains strategically relevant for several regional supply chains. According to some estimates, around one hundred container ships are currently stranded in the Persian Gulf, with the share of global capacity involved potentially ranging from less than 1% to around 10% of effective available capacity.

Industry experts agree on one key point: the longer these vessels and related equipment remain outside the global operational circuit, the greater the impact on container and shipping capacity availability in Asian ports.

When traffic through the strait resumes, a phenomenon known as vessel bunching is also likely to occur, meaning many ships arriving simultaneously at ports after accumulated delays.

This phenomenon can generate further congestion in port terminals, slowing loading and unloading operations.

Combined with rising fuel costs, these factors could push freight rates higher even on routes not directly connected to the Persian Gulf.

Maritime Freight Rates Rising And New Cost Pressures

The impact of the geopolitical crisis is also beginning to be reflected in maritime freight costs, at least for routes directly affected by the closure of the Strait of Hormuz.

For the moment rate increases mainly concern containers destined for Persian Gulf ports, where several carriers are applying extraordinary surcharges to cover operational and insurance risks linked to the conflict.

One of the most significant measures was announced by CMA CGM, which introduced an emergency surcharge of $3,000 per forty-foot equivalent unit (FEU) for containers heading to the Gulf region.

Other operators are also applying additional charges for shipments diverted to alternative ports, further increasing logistics costs for exporters and importers involved. The effect of these measures was immediately visible in transport prices.

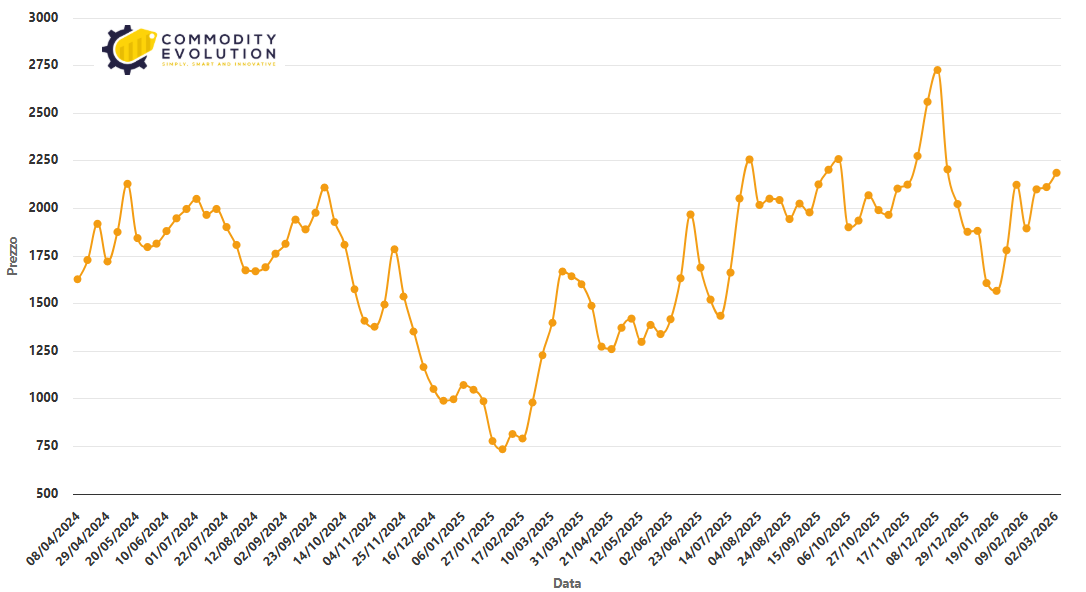

Baltic Dry Index in $ – Powered by Commodity Evolution

Container rates on the Shanghai–Jebel Ali route rose in just a few days from about $1,800 per forty-foot container to more than $4,000, reflecting both extraordinary surcharges and the operational uncertainty generated by the conflict.

In contrast, on the main east-west trade routes prices have remained relatively stable, also because the market is still emerging from the seasonal slowdown linked to the Lunar New Year holiday period.

The Conflict Also Threatens The Red Sea

Military tensions in the region are beginning to generate concerns also for the security of maritime routes in the Red Sea.

The Houthi movement, which had suspended attacks on commercial vessels since October, has threatened to resume military operations against international maritime traffic.

At the moment no new attacks have been reported, but the mere risk of renewed hostilities is already influencing operational decisions by shipping companies. Some operators that had resumed limited sailings through the Red Sea have already decided to divert vessels once again along the alternative route around the Cape of Good Hope.

This diversion results in a significant extension of travel time between Asia and Europe, as well as higher fuel consumption and operating costs.

Consequently, the prospect of a full return to normal operations in the Red Sea could once again be pushed further into the future.

Air Cargo Could Face An Even Greater Impact

While in maritime shipping the effects of the crisis remain relatively localized for now, in air transport the consequences could be even more immediate and significant.

Iranian military operations have in fact targeted several strategic airports in the region, including:

-

Abu Dhabi;

-

Bahrain;

-

Kuwait;

-

Dubai.

Following the attacks, several airports and airspaces were temporarily closed, causing the interruption of numerous international air connections.

These closures are already affecting cargo shipments to and from the Middle East, creating delays and disruptions in global logistics flows. The problem is particularly significant because some of the world’s main cargo airlines operate through Middle Eastern hubs.

Among them are:

-

Qatar Airways Cargo;

-

Emirates SkyCargo;

-

Etihad Cargo.

Together, these operators represent approximately 13% of global air freight capacity.

Their hubs also function as key connection points for air traffic between Asia and Europe, representing about a quarter of total capacity on China–Europe routes.

Disruptions In Cargo Flows Between Asia And Europe

The temporary closure of Middle Eastern hubs is generating strong disruptions in global air routes, especially for shipments connecting Asia, Europe and the United States.

Many trade flows originating from South and Southeast Asia depend on transit through Middle Eastern cargo hubs to reach Western markets.

With several flights cancelled, aircraft grounded and hubs temporarily inaccessible, global air freight capacity has already recorded a significant contraction in recent days. Some signals suggest, however, that direct capacity between Asia and Europe is increasing, in an attempt to compensate for the reduction of connections via the Middle East.

Despite this adjustment, several shippers are already reporting delays and difficulties in securing available capacity, while many companies are scrambling to find alternative routes to avoid the logistics hubs most affected by the conflict.

According to international logistics operators, some freight forwarders are beginning to charter direct cargo flights between the Far East and Europe or the United States, precisely to compensate for the reduction of capacity available through Gulf hubs.

This strategy, however, involves significantly higher costs than traditional transit routes, and could therefore quickly translate into a broader increase in air freight rates. Meanwhile, a backlog of cargo is feared to be forming in major Asian airports, with shipments destined for Europe and the United States potentially starting to accumulate by the end of the week.

If this scenario materializes, the combined effect of logistical backlogs and reduced capacity could lead to further delays and new upward pressure on air freight prices.

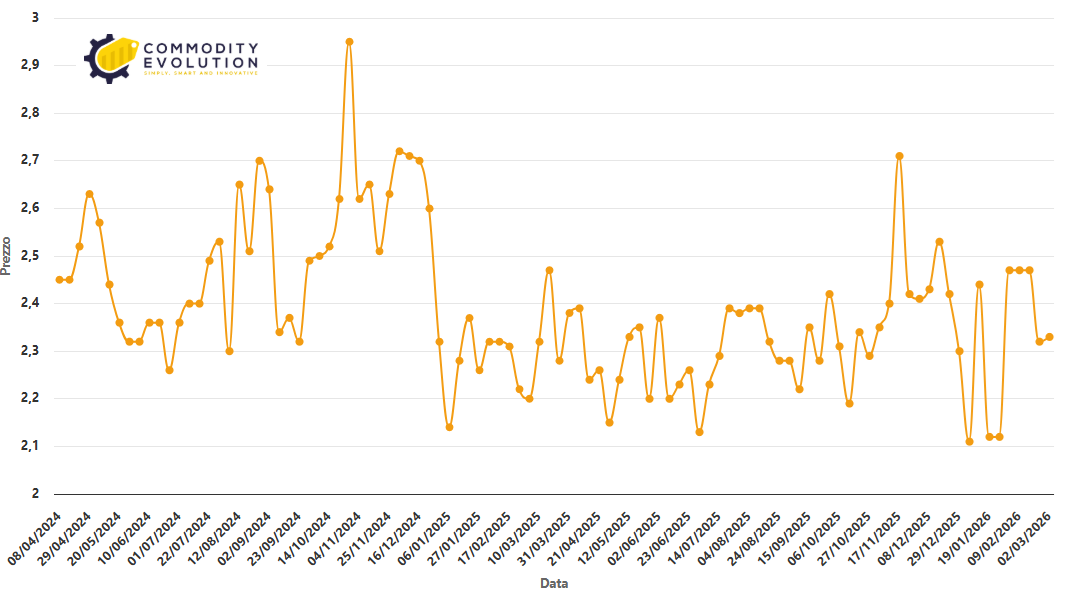

Air Freight Rates Rising On Global Routes

The first signs of tension in air cargo pricing are already visible on several international routes.

According to available global cargo market data, shipping rates from Southeast Asia to Europe have increased by more than 6% in recent days, reaching approximately $3.82 per kilogram.

Routes from South Asia to Europe and the United States are also experiencing significant increases, with prices rising respectively by 3% and 5%.

Shipments between the Middle East and Europe have recorded an increase of about 8%, with rates standing around $1.62 per kilogram. Even stronger increases have been observed on routes between China and the United States, where air cargo prices have risen by 15% to about $6.90 per kilogram.

It should be noted, however, that part of these increases had already begun before the outbreak of the conflict, probably due to the typical demand rebound following the end of the Lunar New Year holiday period.

Despite this seasonal factor, recent geopolitical tensions are contributing to amplifying pressures on international transport prices, especially on routes that depend heavily on Middle Eastern logistics capacity.

Global Air Freight Index $/100-3000kg – Powered by Commodity Evolution