Loading

Loading

|

The last month of the industrial metals market closed with a complex and far from uniform picture, characterized by strong divergences between individual metals and a trend that, while showing signs of recovery in some areas, continues to reflect a still-fragile macroeconomic and industrial environment. Overall, the changes observed in dollars and euros tell a consistent story: metals most closely tied to the energy transition and technological demand have shown greater resilience, while those most exposed to traditional industrial cycles remain under pressure. Copper remains one of the strongest metals in the basket. Monthly, prices rose by more than 6% in dollars and approximately 4.6% in euros, supported by constructive sentiment and structurally tight supply fundamentals. The red metal continues to act as a leading indicator, pricing in the risk of future shortages rather than the contingent weakness in year-end demand. The strength of tin, the undisputed star of the month, is even more evident. Prices rose more than 28% in dollars and over 26% in euros, an exceptionally large move reflecting acute supply tensions and sustained demand from the electronics sector. This is the clearest sign of a market reacting aggressively to structural imbalances. Zinc also posted positive growth, closing the month with gains of approximately 7.6% in dollars and 5.9% in euros. This recovery, while not eliminating the European market’s structural weaknesses, suggests a partial rebalancing after the strong downward pressure of previous months. Primary aluminum showed a more modest but significant recovery: 4.1% in dollars and 2.4% in euros. This rebound appears more technical than structural, in a context still characterized by selective physical demand, high inventory levels, and a market struggling to find a clear direction. The situation for nickel is decidedly more fragile. Despite a positive monthly recovery (+4.6% in dollars and +2.9% in euros), the metal continues to show high volatility and underlying weakness, penalized by ample supply—particularly from Indonesia—and by uneven demand for stainless steel. Lead also struggled, closing the month down in both currencies (approximately -0.6% in dollars and -2.2% in euros). Demand for traditional batteries remains insufficient to sustain a sustained recovery, leaving the metal in a phase of persistent weakness.  Performance Metals Cash $/ton  Performance Metals Cash €/ton Bloomberg Primary Aluminum: Strengthening Fundamentals, Physical Markets Increasingly SelectiveThe global primary aluminum market is currently operating in a complex equilibrium, with structurally bullish signals in the medium term coexisting with still–fragmented short-term dynamics. The emerging picture is of a market supported by fundamentals, yet held back by physical demand that, especially in mature markets, remains selective and price-sensitive.

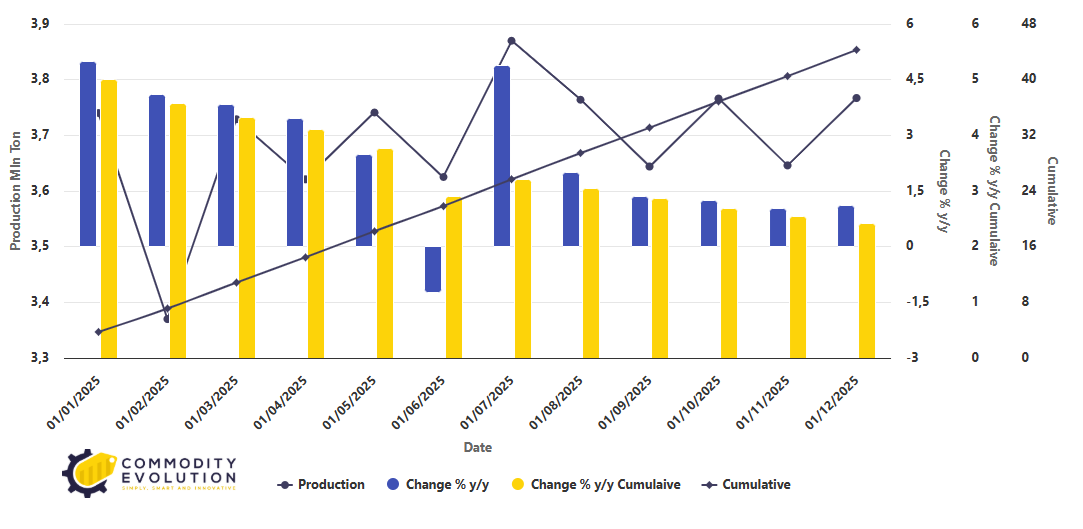

The starting point remains China, where total primary aluminum supply reached approximately 46.6 million tonnes in 2025, essentially in line with domestic consumption. The slight surplus estimated for the current year already appears to be a statistical residue rather than a true market buffer. Looking ahead to 2026, the dynamics are changing significantly. Domestic production growth is set to slow further as the system approaches the regulatory ceiling of 45 million tonnes, while the contribution of imports also appears uncertain. Foreign projects, particularly in Indonesia, are progressing slowly due to energy constraints, while in Europe and North America, electricity costs continue to threaten production stability. On the demand side, however, resilience remains evident. Automotive, photovoltaic, power grids, and energy storage continue to provide a solid structural foundation, potentially pushing the Chinese market into deficit in 2026. In this context, Mysteel’s expectations for strengthening domestic prices appear consistent with a market gradually losing its flexibility.  Primary Aluminum Production in China – Powered by Commodity Evolution

While global fundamentals tell a constructive story, the European premium market reflects a more fragmented reality. P1020A premiums in Rotterdam remain broadly sideways, but with increasingly widening ranges, a sign of growing segmentation by production type. Coal-based material is progressively penalized, with discounted sales widening the lower end of the ranges, while gas-based and low-carbon aluminum continues to defend high premiums. This is not a generalized weakness, but rather an increasingly clear selection pattern, reflecting evolving industrial preferences and the anticipation of the impact of the CBAM. In the short term, the availability of duty-paid metal remains relatively abundant and represents a brake on decisive directional movements. However, the underlying sentiment remains constructive: many operators believe that, once the remaining 2025 inventories are absorbed, premiums will necessarily need to more fully incorporate emissions-related costs.

Segmentation is even more evident in the duty-unpaid market. Here, coal is experiencing marked downward pressure, while non-coal metal is showing signs of actual physical scarcity. The difficulties encountered by operators in sourcing units compliant with contractual specifications have led to anomalous situations, such as the use of duty-paid metal to cover duty-unpaid positions. This imbalance highlights a crucial aspect: beyond average premium levels, the real constraint on the European market is becoming the emission quality of the supply, rather than the overall availability of tonnage. . P1020A Aluminium Premium – DDU – Rotterdam – Powered by Commodity Evolution

In Asia, the premium market is moving defensively. The Japanese MJP quarterly premium continues to act as an anchor for the entire region, supporting valuations even in the absence of particularly buoyant spot demand. In Japan, purchases remain subdued, and spot premiums remain structurally below quarterly levels, consistent with stable but lacking momentum demand. In South Korea, the premium adjustment appears more a technical realignment to the Japanese fixing than a reflection of improving consumption. Finally, in China, an increasingly clear gap is emerging between theoretical levels and prices actually acceptable to the market. The seasonal slowdown linked to the Lunar New Year is accentuating buyers’ caution, squeezing liquidity and pushing premiums toward selective adjustments rather than a generalized repricing.

The key element that emerges from the joint analysis is the temporal misalignment between prices and physical premiums. Primary aluminum fundamentals, particularly on the supply side, point to price strengthening in the medium term. Physical premiums, however, remain anchored to short-term dynamics: inventories, seasonality, and qualitative segmentation. This explains why the market appears sideways and fragmented today, while preparing the conditions for a more structural adjustment in the coming months. Scenario for the Next Month: Apparent Stability, Pressures Building In the coming month, the most likely scenario is continued sideways movement in premiums, accompanied by a high degree of price dispersion based on the metal’s origin and emission profile. No sharp directional movements are expected in the very short term, but upward pressures remain latent, especially for non-coal-based materials. Regarding LME prices, the fundamental context suggests greater resilience compared to other industrial metals. Any corrections should remain limited, with the market continuing to price in the risk of tighter future supplies.

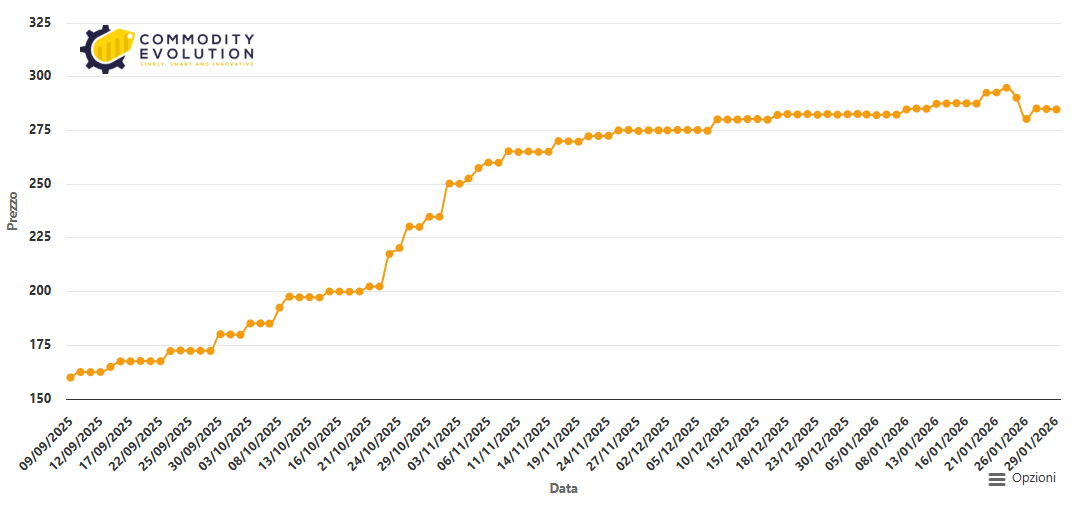

The month of January ended with a clear signal on the LME primary aluminum chart: after an orderly and persistent upward trend, the market suddenly slowed, giving way to a sharper correction. The movement, visually evident in the final part of the chart, does not appear to be a structural reversal, but rather a physiological profit-taking after weeks of almost uninterrupted growth. The trend that accompanied aluminum from late autumn to early 2026 remains well-defined. Prices have constructed a sequence of higher lows and higher highs, supported by a progressive improvement in sentiment and by fundamentals that, especially on the supply side, continue to suggest a less abundant market than in previous years. The acceleration seen between December and January led prices to push above the $3,300/t area, before encountering technical and psychological resistance that triggered the recent correction. The return to the $3,050/t area, where the latest settlements were recorded, now represents a key step. This zone coincides with an initial level of dynamic support, as well as an area where the market had previously consolidated before the final bullish leg. Price reaction at these levels will be crucial in setting the tone for February. Momentum-wise, indicators show a clear cooling from January’s peaks. The negative swing observed in recent days suggests that the market is unloading some of its accumulated excesses, but without yet compromising its underlying structure. In other words, aluminum appears to be entering a phase of normalization, rather than structural weakness.

|

10 min read