Loading

Loading

As the August 1 deadline for suspending reciprocal tariffs approaches, the White House announced a series of last-minute agreements with several major trading partners, including the European Union and Japan.

As the August 1 deadline for suspending reciprocal tariffs approaches, the White House announced a series of last-minute agreements with several major trading partners, including the European Union and Japan.

These agreements aim to avoid a tariff escalation that could have further disrupted global supply chains.

The agreement with the European Union includes a 15% base U.S. tariff on most European exports to the United States. This represents an increase from the current 10%, but is lower than the recent threat of a 30% tariff.

The new rate will also apply to EU automotive exports, which, along with all global exports of vehicles and parts to the United States, have been subject to 25% tariffs since April and May, respectively.

The agreement could also include a quota-based reduction in US tariffs on European steel and aluminum exports. Furthermore, the EU commits to purchasing energy from the United States and investing significantly in the American energy sector.

In return, the United States will enjoy zero or very low tariffs on most of its exports to the European bloc.

These terms are expected to come into force on August 1, once the joint declaration is finalized, although the full details and legally binding text will still be available.

Agreements With Japan, Southeast Asia, and the United Kingdom

The agreement with Japan follows a similar structure, with US tariffs also set at 15% for automotive exports. In return, Tokyo has committed to increasing investment in the United States.

President Trump also announced agreements with Vietnam, subject to a 20% tariff rate, and with Indonesia and the Philippines, both at 19%.

Considering the previous agreement with the United Kingdom, the United States has now concluded or is finalizing agreements with countries that represent approximately 30% of total US goods imports in 2024, in value terms.

Stress Remains with China, Mexico, and Canada

However, progress with the United States’ three largest trading partners—China, Mexico, and Canada—which together account for a further 41% of imports, remains uneven.

Negotiations with Mexico and Canada are ongoing, while both countries risk 30% tariffs starting August 1st. Meanwhile, US and Chinese representatives are meeting this week in Stockholm ahead of the August 12th deadline, with expectations of a further 90-day extension of the tariff status quo, following signs of easing tensions.

Since mid-May, US tariffs on China have been set at a baseline of 30%, but for many goods, the effective rate is already significantly higher, a legacy of tariffs imposed by the previous Trump administration.

Effects on Freight Transportation: Unbalanced Demand and Altered Tariffs

The numerous waves of announcements, suspensions, and deadlines have generated a substantial shift in seasonal demand and tariff patterns in the freight transportation sector. Many importers have moved shipments forward to avoid the impact of higher tariffs, while others—particularly those importing from China—suspended operations when tariffs reached prohibitive levels.

This behavior served as a hedge against the potential failure of negotiations, which could have led to tariffs rising above the provisional 10%. However, developments in recent weeks suggest that even with the agreements in place, Washington aims to maintain a stable tariff range between 15% and 20%.

Impact on Transatlantic Trade: Volumes Decline, Tariffs Steady

Ocean freight volumes between Europe and the United States remained stable overall through April 2025. However, the implementation of tariffs on automobiles in April coincided with a 7% year-over-year decline in monthly volumes, suggesting an initial negative impact on shipments.

Tariffs imposed in May on auto parts may also have discouraged any attempts at frontloading during the suspension of reciprocal tariffs, which lasted from April to July.

The agreement signed this week, reducing tariffs on European vehicles by 10%, could stimulate a slight rebound in volumes. However, the general 15% tariff on European exports—a 5% increase over the regime in effect since April—makes a sharp recovery unlikely in the near term.

The fate of specific categories such as wines and spirits, which could further impact the trend, remains uncertain.

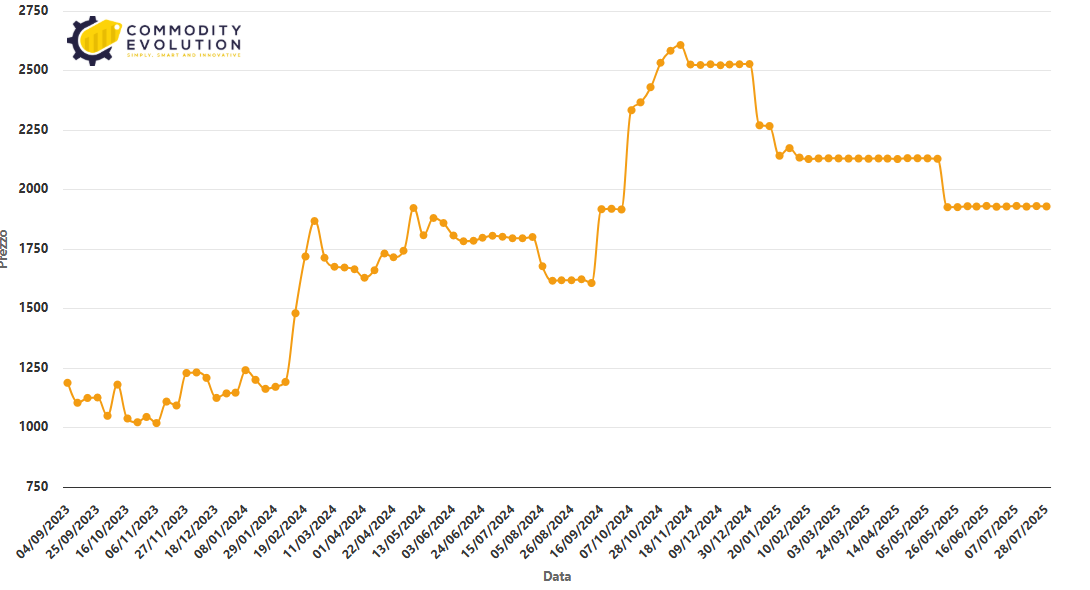

Ocean container freight rates on the transatlantic route remained virtually unchanged.

From Northern Europe to North America East Coast – by sea $/FEU – Powered by Commodity Evolution

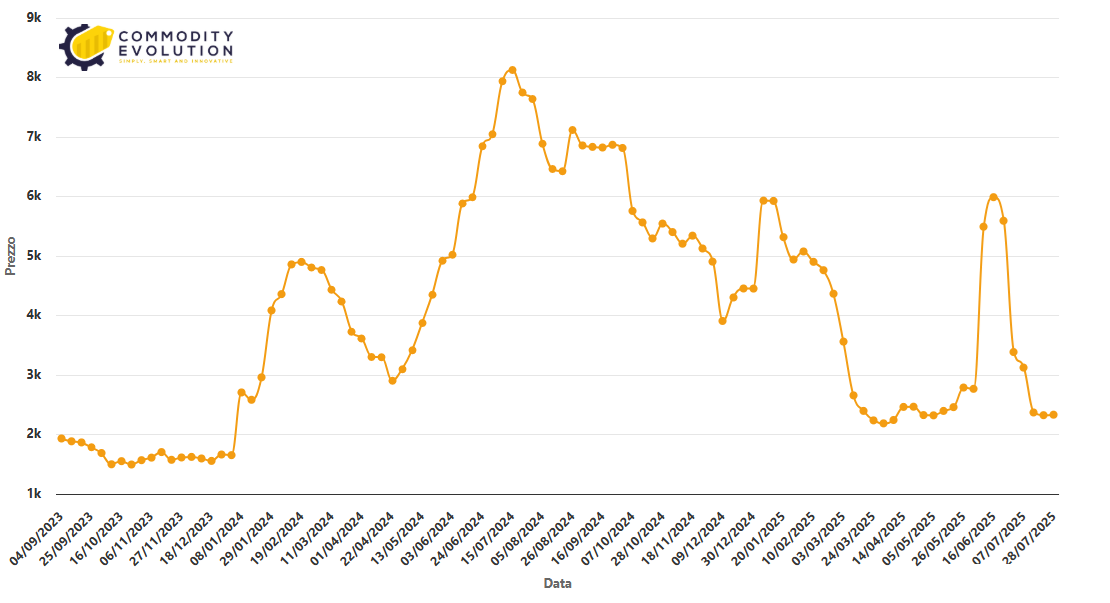

Trans-Pacific Trade: Brief but Intense Effect, Then Return to Normal

In trade between Asia and the US West Coast, the reduction in US tariffs towards China—from 145% to 30% in mid-May—triggered an early and brief peak in the peak shipping season. Container rates from Asia to the US West Coast peaked at $6,000/FEU by mid-June.

However, by mid-July, rates had already returned to their previous levels of around $2,300/FEU, signaling a drastic drop in demand. Rates subsequently remained unchanged, thanks in part to carriers reducing capacity to accommodate lower volumes, making the implementation of the General Rate Increases (GRIs) scheduled for August unlikely.

From China-East Asia to North America West Coast – by sea $/FEU – Powered by Commodity Evolution

A further 90-day extension of the current 30% tariff, as envisioned in US-China talks, would cover the traditional peak season. This could encourage some shippers who had moved imports forward between May and June, or who were waiting for greater clarity, to resume seasonal bookings.

However, given the already significant frontloading effect, it is likely that the seasonal “peak of the peak” has already passed.

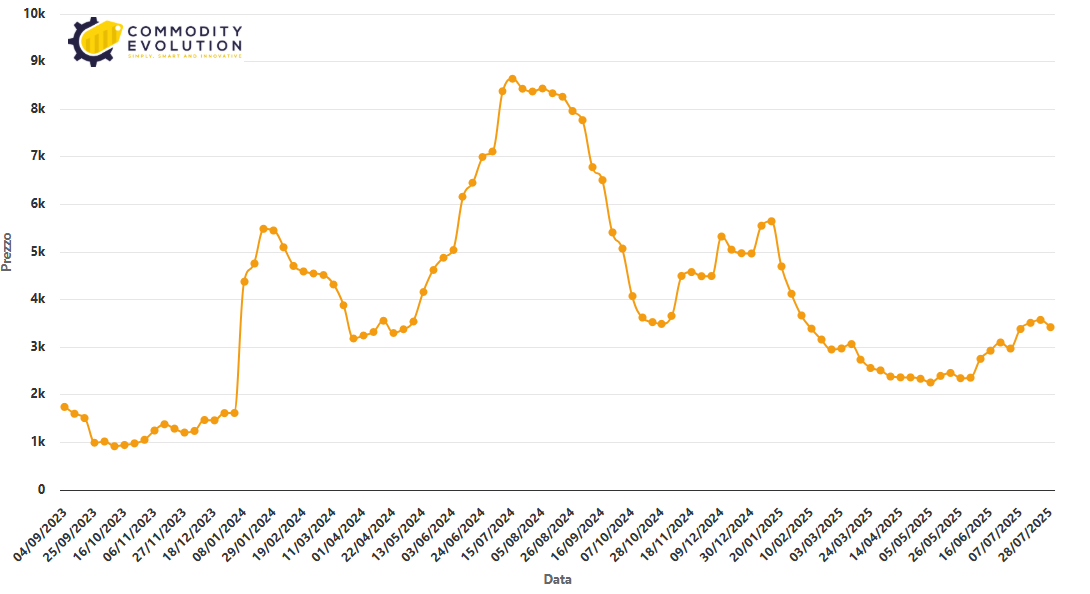

Asian Routes to Europe: Congestion and Still High Rates

Freight rates from Asia to Northern Europe fell 4% last week, settling at $3,420/FEU, similar to the start of the month but still 45% higher than at the end of May. This elevated level is supported by peak-season demand and persistent congestion at major European hub ports.

From China-East Asia to Northern Europe – by sea $/FEU – Powered by Commodity Evolution

Should congestion worsen with the continued arrival of peak-season containers, some lines anticipate the introduction of peak-season surcharges (PSS) of up to $500/FEU for August.

However, signs of price stabilization to Northern Europe, combined with a 30% drop in Asia-Mediterranean freight rates since their mid-June peak (to $3,400/FEU), indicate that fleet growth and resulting overcapacity could already negatively impact rate trends.

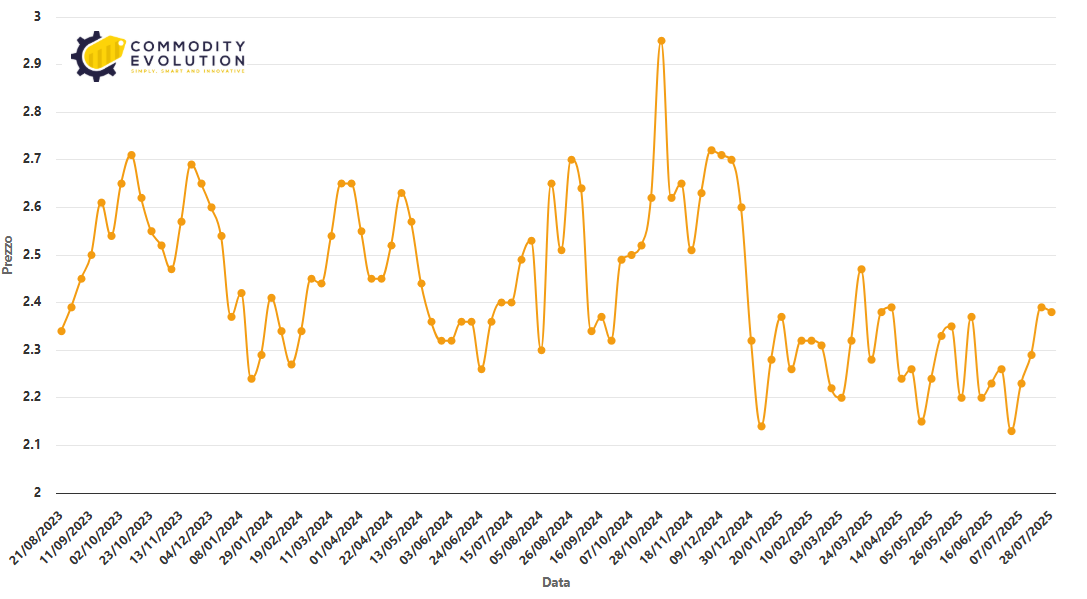

Air Cargo: Limited Impact from New Tariffs

Air freight could receive a slight boost from the reduction of US tariffs on auto parts from the EU and Japan. However, overall, there has been no significant acceleration in air freight volumes ahead of the tariff deadlines, indicating that the market reaction has been limited.

Air cargo rates from China to the United States increased 3% to $5.31/kg, in line with May and June levels. Transatlantic prices remained stable at $1.77/kg, while China-Europe rates increased 11% to $3.72/kg, likely driven by a moderate increase in demand as the tariff deadline approaches.

Global Air Freight Index $/100-3000kg – Powered by Commodity Evolution

Conclusions: Less Uncertainty, But Higher Tariffs Are the New Normal

Despite widespread discontent among importers and exporters over the increased tariffs—which will affect most goods traded on these routes—global trade participants can at least count on greater clarity.

The agreements reached, while imposing higher tariffs than in the recent past, offer a more predictable framework compared to the constant regulatory changes and tariff threats of recent months.

Traders with high inventories due to frontloading may continue to postpone bookings until they run out, slowing the return to usual seasonal shipping patterns. However, once inventory dynamics normalize, seasonality in flows is likely to return—albeit with higher costs passed along the chain to the end consumer.

The clear message emerging from the latest developments is that, for Washington, tariffs in the 15–20% range are no longer exceptional measures, but the new normal in the trade landscape. For global operators, adapting to this new reality will be crucial to maintaining competitiveness and continuity in supply chains.