Loading

Loading

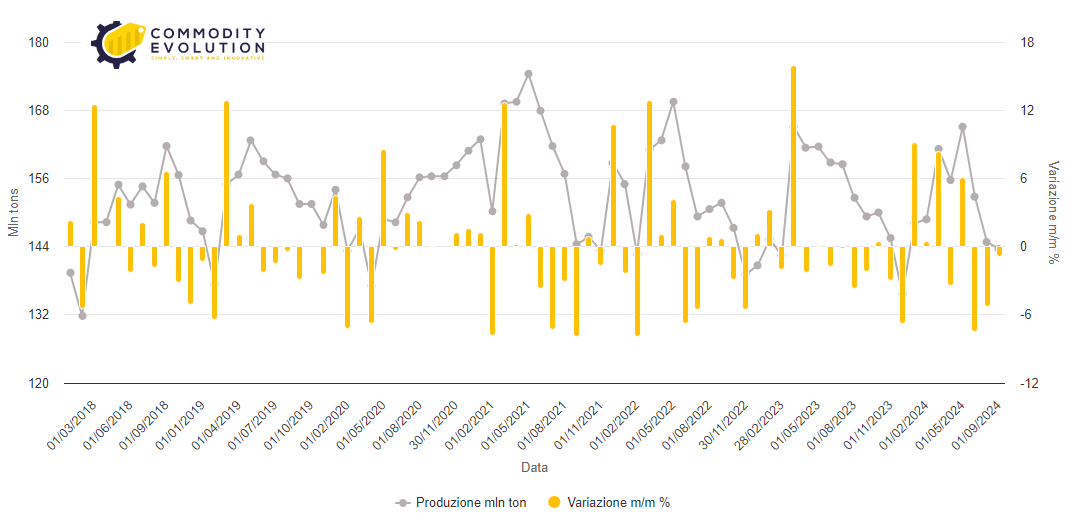

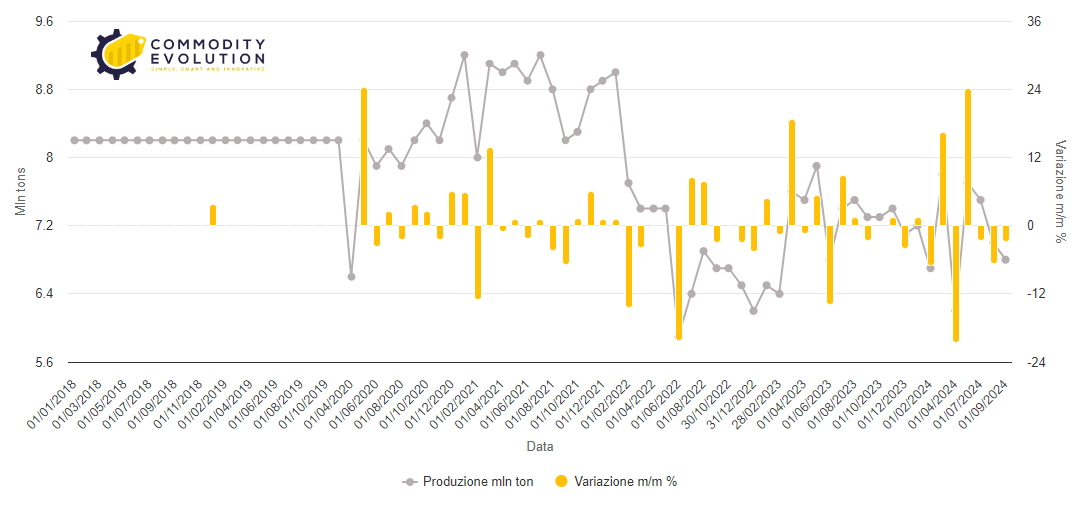

The World Steel Association (worldsteel) recently released data on world crude steel production for September 2024, showing a significant contraction globally.

Total production stood at 143.6 million tonnes, marking a decrease of 4.7 per cent year-on-year. This decline is part of a broader trend for the entire year: from January to September 2024, global crude steel production decreased by 1.9% to a total of 1.39 billion tonnes.

World Crude steel production – Powered by Commodity Evolution

The Decline in Asia: A Signal for the Industry

Asia, which is the most productive region in the global steel scene, suffered a 5% decline in crude steel production compared to the same month last year. With 105.3 million tonnes produced, Asia continues to be a dominant player, but data show signs of a slowdown.

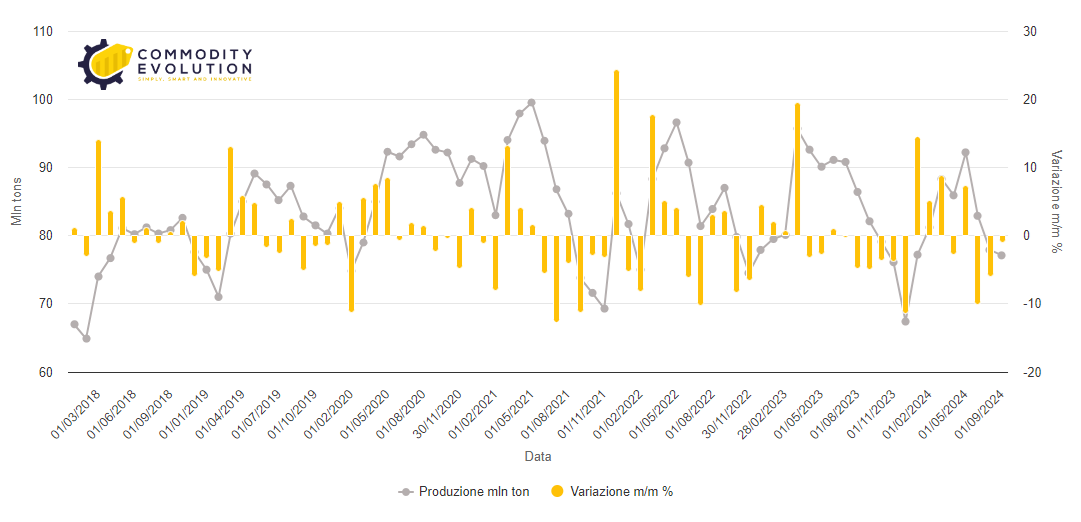

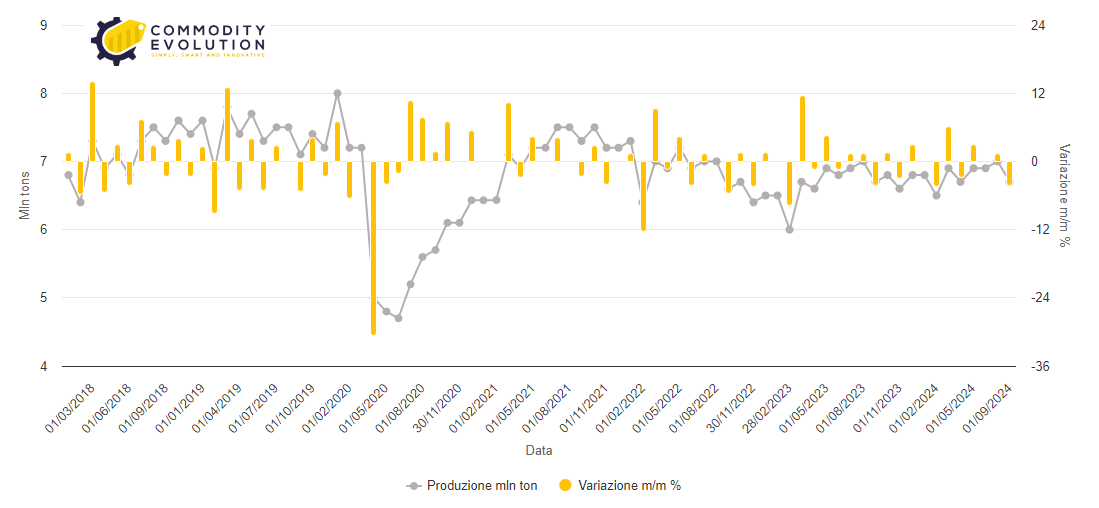

China, the world’s largest steel producer, recorded a year-on-year decline of 6.1% to 77.1 million tonnes. This figure is particularly significant because it reflects the challenges China is facing, including weak domestic demand and economic difficulties related to the slowdown in the real estate sector Read more

The decline in Chinese production significantly affects the global market, given China’s importance in steel production.

China Crude steel production – Powered by Commodity Evolution

Japan also suffered a significant drop, with a year-on-year decrease of 5.8% to 6.6 million tonnes of crude steel in September. The decline in Japanese production follows a slowing trend in the country’s manufacturing industry, which continues to suffer from global economic difficulties and Asian competition.

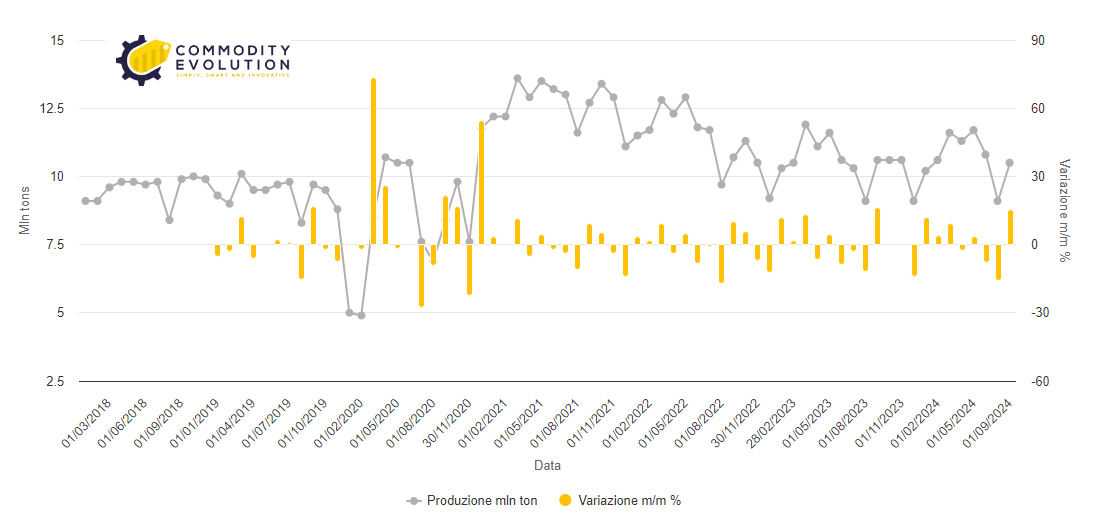

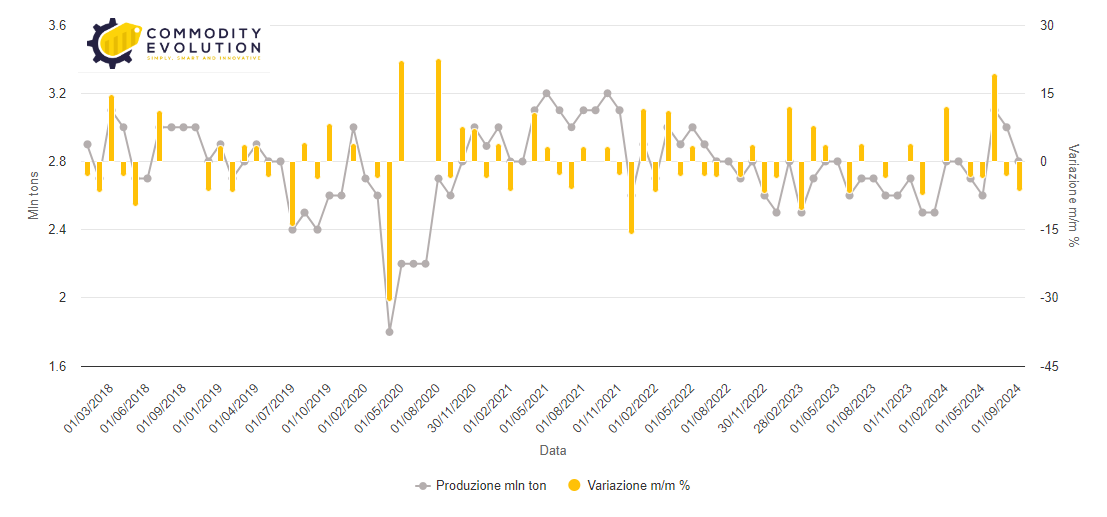

In contrast, India, the world’s second largest steel producer, recorded a much smaller decrease of 0.2%, with production of 11.7 million tonnes. India continues to be an attractive market, with domestic demand growing thanks to massive investment in infrastructure.

India Crude steel production – Powered by Commodity Evolution

South Korea, on the other hand, was the only Asian nation to record an increase in production in September, up 1.1% year-on-year to 5.5 million tonnes. This reflects the resilience of the Korean steel sector, which continues to benefit from strong domestic demand and stable export markets.

Europe: Signs of Recovery in Some Countries

In September, EU-27 countries produced a total of 10.5 million tonnes of crude steel, up slightly by 0.3% year-on-year. Although this increase seems modest, it is a positive sign for the European steel industry, which has faced many challenges in recent years, including global competition and changes in energy demand.

Eu 27 Crude steel production – Powered by Commodity Evolution

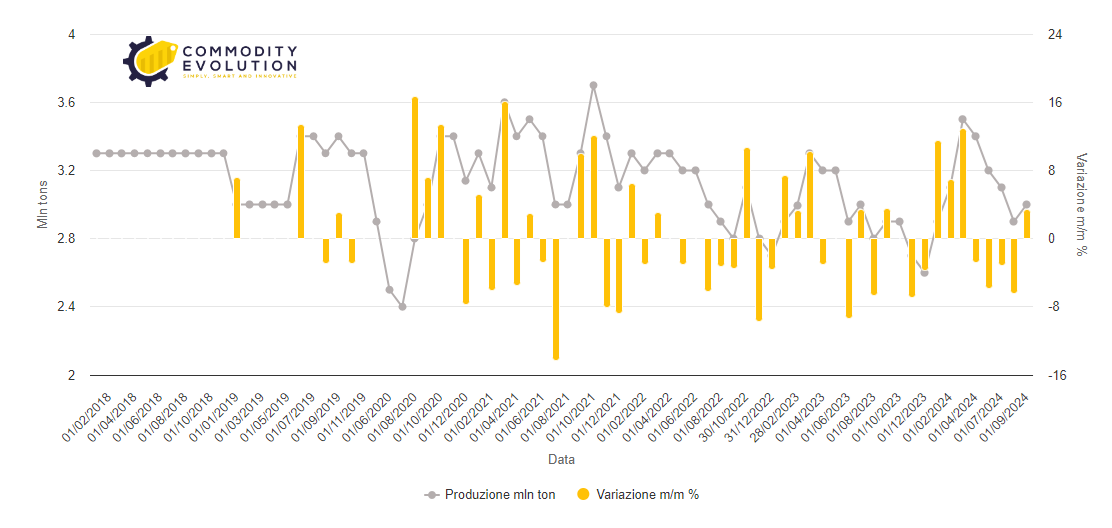

Germany, the largest steel producer in the European Union, recorded a 4.3% growth to 3 million tonnes in September. This increase is linked to a recovery in industrial production and greater stability in the automotive and construction sectors.

Germany Crude steel production – Powered by Commodity Evolution

However, the European steel industry continues to face high energy costs and stringent environmental regulations, which may limit further production increases in the long term.

Turkey and the CIS Area: Between Increases and Declines in Production

Turkey stands out as one of the few countries to record significant growth in steel production as of September 2024. With a year-on-year increase of 6.5%, Turkish production reached 3.1 million tonnes.

Turkey Crude steel production – Powered by Commodity Evolution

This increase reflects the resilience of the Turkish steel industry, which continues to benefit from domestic demand and exports to Europe and the Middle East. However, Turkey also has to contend with fluctuating raw material costs and domestic economic volatility.

In sharp contrast, the countries of the Commonwealth of Independent States (CIS) saw a 7.6% decrease in production to 6.8 million tonnes. In particular, Russia’s estimated production decreased by 10.3% to 5.6 million tonnes.

CIS Crude steel production – Powered by Commodity Evolution

The Russian steel sector was hit by a combination of international economic sanctions and falling demand, which limited the country’s production capacity and exports.

North and South America: Contrasting Trendsù

In North America, crude steel production declined 3.4% year-on-year to 8.6 million tonnes in September. In the US, production increased 1.2% to 6.7 million tonnes, signalling a slight recovery in domestic industrial demand.

Us Crude steel production – Powered by Commodity Evolution

However, the US steel sector remains under pressure due to global competition and economic uncertainty.

In contrast, South America saw a 3.3% growth in crude steel production, reaching 3.5 million tonnes. Brazil, the continent’s largest producer, recorded a significant increase of 9.9%, producing 2.8 million tonnes. Strong demand for steel for infrastructure projects and the manufacturing industry continues to support the sector’s growth in South America.

Brazil Crude steel production – Powered by Commodity Evolution

Africa and the Middle East: Between Growth and Decline

In September, crude steel production in Africa increased by 2.6% year-on-year to 1.9 million tonnes. This increase is a positive sign for the continent, which is trying to strengthen its production capacity and meet the growing domestic demand for construction materials.

On the other hand, the Middle East saw a dramatic 23% drop in production, with 3.5 million tonnes produced in September. This decline reflects the economic difficulties and geopolitical uncertainties that are affecting the region, negatively affecting industrial production and steel demand.

In conclusion, global crude steel production is facing a period of contraction, with some regions showing signs of recovery and others continuing to struggle with economic and geopolitical challenges.

While Asia, particularly China, is slowing down, Europe and South America are showing tentative signs of growth. However, the future of the global steel industry remains uncertain, with many producers facing rising energy costs, global competition and fluctuating demand.