Loading

Loading

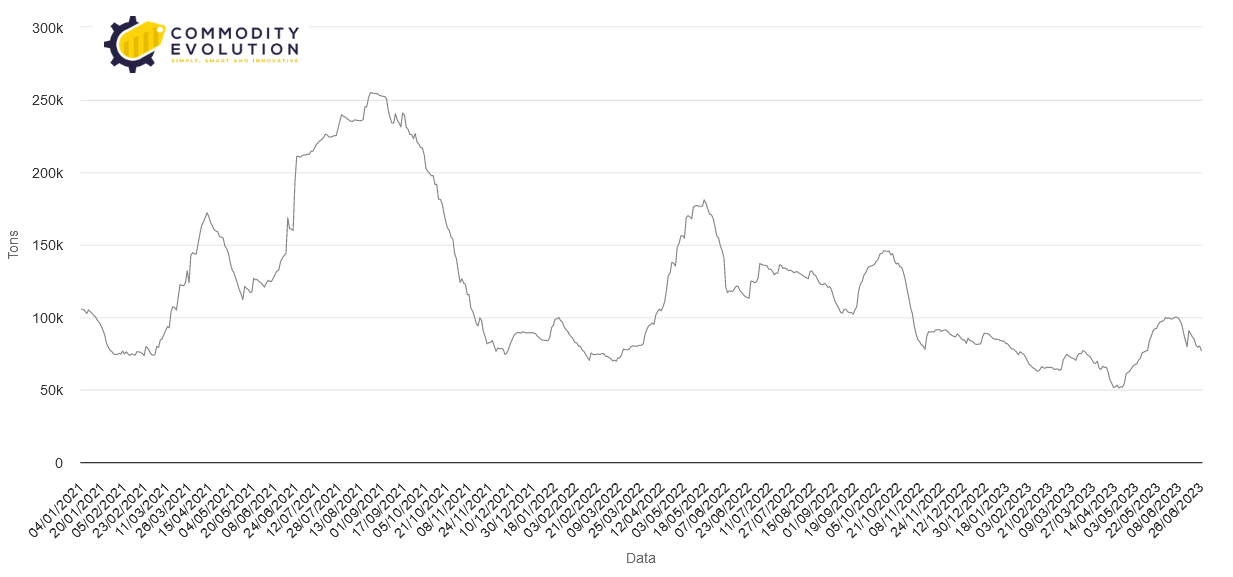

There is a renewed rush for copper in London Metal Exchange (LME) warehouses. In the past three weeks, LME copper stocks have fallen from 100,100 to 77,050 tons, despite nearly 30,000 tons of arrivals.

There is a renewed rush for copper in London Metal Exchange (LME) warehouses. In the past three weeks, LME copper stocks have fallen from 100,100 to 77,050 tons, despite nearly 30,000 tons of arrivals.

What arrives turns just as quickly into new output. The available tonnage is just 31,900 tons, enough to supply the global market for about 11 hours.

Not surprisingly, the stock incursion has ignited LME time-spreads, with the cash-to-threes reporting period closing Monday with a backwardation of $31 per ton. This is the highest premium for cash since November last year.

The depletion of LME copper stocks is surprising considering the weakening manufacturing activity in both Europe and the United States.

The closure of Swedish producer Boliden’s Ronnskar smelter opened a 220,000-ton supply gap in the European market, but the assault on LME stocks began before the June 13 plant fire and focused on Asian and U.S., not European, sites.

LME Copper Inventories – Powered by Commodity Evolution

But this is not just a London market phenomenon. Visible stocks are low everywhere. At the end of last week, copper stocks recorded by the LME, its U.S. counterpart CME and the Shanghai Futures Exchange (ShFE) totaled 165,000 tons.

Global stocks are now down 45,500 tons from the beginning of the year and are the lowest since 2008. The small replenishment of LME inventory in April and May was reversed this month.

CME inventories are up, but from a very low base, and at 27,859 tons are still down 3,975 tons from the beginning of the year.

ShFE stocks rose sharply during the seasonal pause in demand during the Lunar New Year holiday, but stabilized at 252,455 tons in February and have since declined rapidly to only 60,424 tons.

The Shanghai Futures Exchange has experienced tension at the front end of the curve since March, with time spreads now the widest since November.

The rigidity of the Shanghai Futures Exchange seems to be attracting metal from the city’s captive storage areas.

Captive stocks held by ShFE’s international arm, the International Energy Exchange, have plummeted from nearly 89,000 at the beginning of the month to just 35,000. Other captive stocks are estimated at 66,400 tons, down from the March peak of 185,600 tons.

Trade data for the past two months also suggest a movement out of bonded warehouses to mainland China.

China “imported” nearly 30,000 tons of Chinese copper in April and May, likely indicating that the metal qualified for duty-free export under a contract for toll processing was reintroduced into the domestic market.

The counter-flow significantly offset Chinese “exports” of 45,000 tons in the same two months. The increase in domestic production is expected to help ease Shanghai’s tension.

In May, China imported a record 2.56 million tons of concentrates and churned out a record 1.1 million tons of refined copper. But net copper offtake from the rest of the world also increased last month to 276,000 tons, the highest monthly total since January.

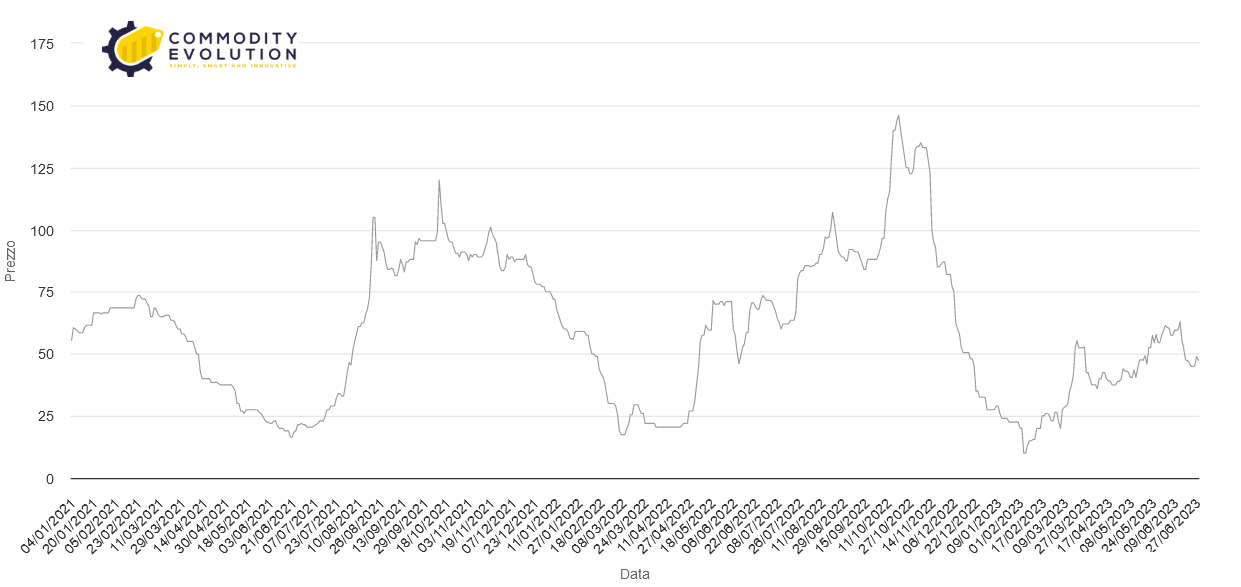

The premium on Yangshan copper, a closely watched indicator of China’s import propensity, rose from $22.50 per ton in May to $47.50 today.

Premium Copper China Yangshan $/ton – Powered by Commodity Evolution

It is noted that LME stocks in Asia have been particularly in demand, with only 4,475 tons still available in the region.

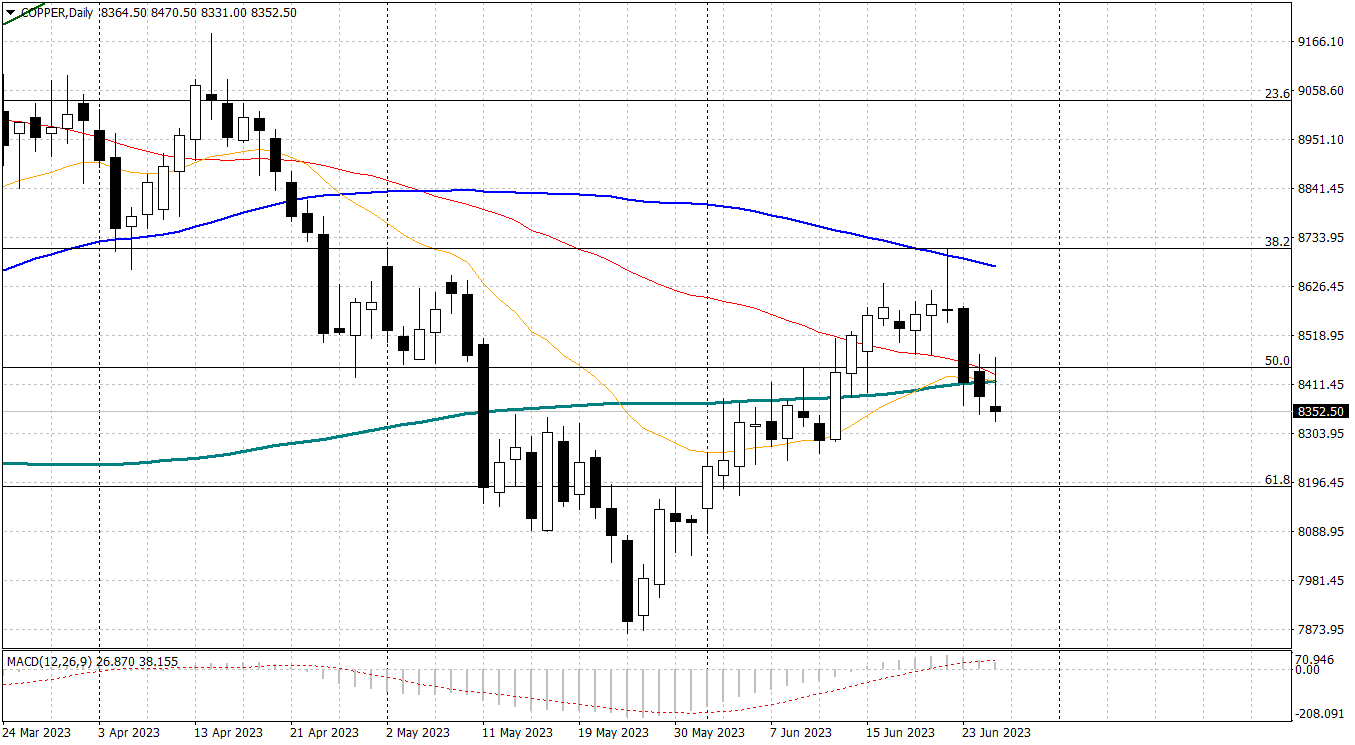

Last week, three-month LME copper briefly reached a two-month high of $8,868 per ton, but has since fallen back to the current $8,380.

The limited price reaction and relatively limited feedback at the front end of the curve imply that the market is betting that there is much more copper in circulation in private stocks.

The pace of arrivals at the LME in recent days shows that there are units available for trading collateral. Physical premiums are weak in all three regions due to weak spot demand.

Surplus metal, however, does not remain in the LME warehouse system, leaving visible stocks to be a bull flag in an otherwise bearish landscape.

Either global trading stocks will rebuild during the summer seasonal weakness in Northern Hemisphere demand, or the market will have to reconsider how much copper is actually in circulation.

Copper – 3 month $/ton daily