Loading

Loading

Aluminium prices still do not have enough strength to form a bearish or bullish trend, as quotations have not yet broken out of range significantly, there is no clear trend and the market remains highly volatile.

Aluminium prices still do not have enough strength to form a bearish or bullish trend, as quotations have not yet broken out of range significantly, there is no clear trend and the market remains highly volatile.

The LME continues to have a Russian problem. After a slight drop in April, the share of Russian aluminium in LME warehouses jumped to 68% in May (read more here). The problem originated last autumn, when the exchange chose not to restrict or ban Russian material from its warehouses. The move came despite a growing number of governments and companies deciding to sanction it.

The LME eventually dismissed the risk of such a build-up. At the time, it argued that a slowdown in the West and the number of countries still willing to buy Russian aluminium would help stocks adjust on their own. However, this did not happen. On the contrary, the use of the LME as a global benchmark appears increasingly at risk.

The LME seems to recognise the market’s growing concern over the disproportionate presence of Russian-origin primary aluminium, as the latest monthly Country of Origin (COO) data was accompanied by a formal update.

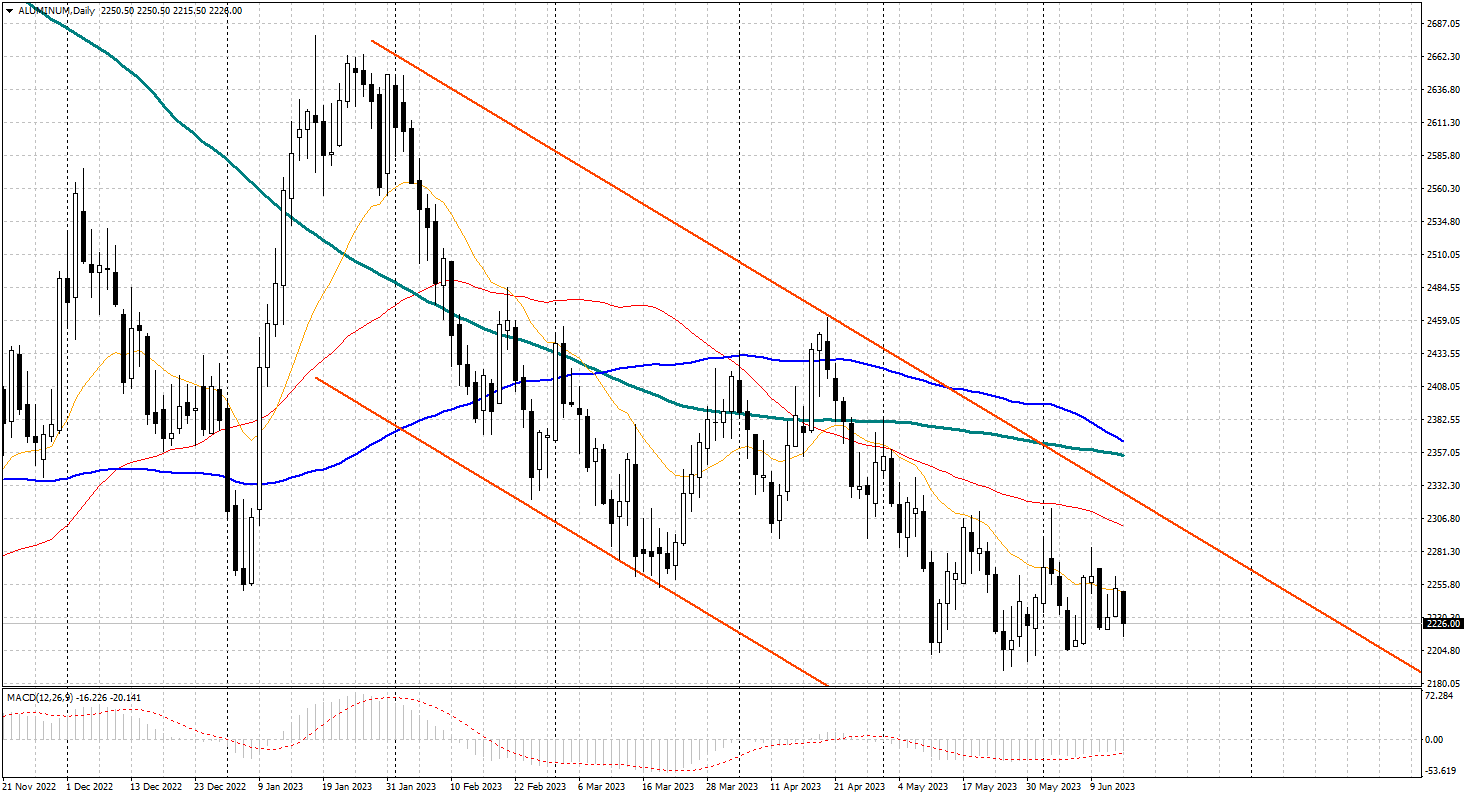

Aluminium 3 months $/ton – daily

The stock exchange began adding COO data to inventories earlier this year to improve transparency and apparently alleviate market concerns. In this case, the additional information that ‘the LME deems useful to provide’ includes data on warrants and outflows from stocks which, at least according to the LME, mean that ‘a significant group of global consumers continue to accept Russian metal’.

However, once again the stock exchange chose not to take further action to regulate Russian inflows. In the absence of any move by the LME, supply from India will play an important role as a counterweight to Russia, as it has done all year.

Aluminium is by no means the only contract at risk for the LME. According to a recent Bloomberg article, the LME has lost its benchmark status for part of the nickel market. As Christel Bories, CEO of ferronickel producer Eramet SA, stated, a Shanghai Metals Market index ‘has become the benchmark’ for the price of ferronickel.

While the CME chose not to create a nickel contract in the wake of the LME squeeze, it does have an aluminium contract with enough liquidity to make it usable as a trading mechanism.

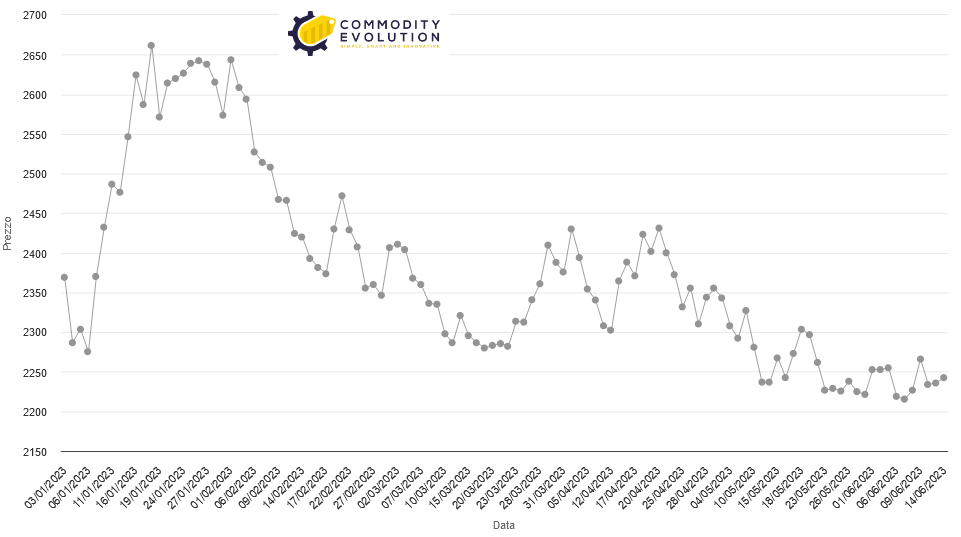

Currently, LME and CME aluminium prices continue to move largely in tandem. Since 2022, CME prices have averaged a premium of $8/mt over LME prices. Currently, the delta is almost $23/tonne, as the increasing presence of discounted Russian material weighs on LME prices.

Aluminium 3 month $/ton LME – Powered by Commodity Evolution

While remaining strong, the correlation between the two prices is now decreasing, albeit modestly. LME and CME aluminium prices boast a correlation of 99.56% that began in early 2022. However, if only the first five and a half months of 2023 are considered, this correlation drops to 97.74%.

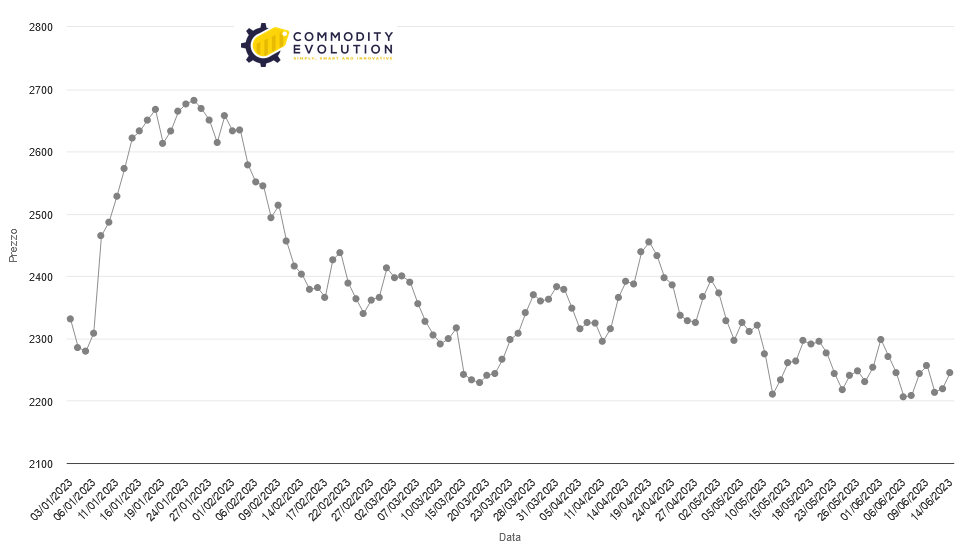

Aluminium CME $/ton – Powered by Commodity Evolution

The correlation between the two prices may continue to diminish as the aluminium market becomes increasingly regionalised and, as a result, LME prices may become less and less relevant for Western buyers.

Meanwhile, India was the latest country to request tariff exemptions for aluminium and steel products. India’s move comes a year after the EU and the UK successfully negotiated tariff rate quotas (TRQs). In its recent request, India offered to remove tariffs on some US agricultural products.

The country took these measures in response to the Trump administration’s 2018 tariffs. The duties marked a 25% duty on steel imports and a 10% duty on aluminium imports. According to market sources, the possibility of approval of the Indian request appears unlikely, meaning that there will be no impact on the market.

Instead, the US is likely to continue to protect its domestic producers in view of the commissioning of several new plants. The completion of the Novelis steel plant in Alabama and the Steel Dynamics plant in Mississippi will add a production capacity of 850,000 tonnes.

Although both will not start production until 2025, the increase in capacity in the US could become a further challenge for the LME. As the market becomes increasingly deglobalised, this could pave the way for greater use of CME prices for contracts.