Loading

Loading

The Italian cast iron market was mostly quiet in April. The holiday period and plant closures for maintenance work played a part in the market downturn. While most steelmakers expect their prices to fall, they are unwilling to adjust.

The Italian cast iron market was mostly quiet in April. The holiday period and plant closures for maintenance work played a part in the market downturn. While most steelmakers expect their prices to fall, they are unwilling to adjust.

The gap between prices in the global market has further widened. The lowest prices were recorded in Europe and Turkey, while in the United States, which mainly purchases pig iron from Brazil, prices increased by at least $100/mt despite slightly lower purchases. Demand from steelmakers continues to decline and supply is good.

Production of hematite cast iron, on the other hand, was limited in April as some producers carried out maintenance work during the holidays. Overproduction occurred due to a slight decline in orders. The supply of cast iron of different origins, such as those from Brazil and Russia, continues to be at high levels.

Prices have fallen slightly due to the sluggish market and producers expecting further decreases only buy according to their needs.

Also, it was noted that while energy costs were incurred and this is not a cause for concern, it still played a significant role in profitability. Although the smelting industry has declined and is wary of accepting orders in the coming weeks, production has continued.

Italian Ferrous Scrap – Cast iron euro/ton Powered by Commodity Evolution

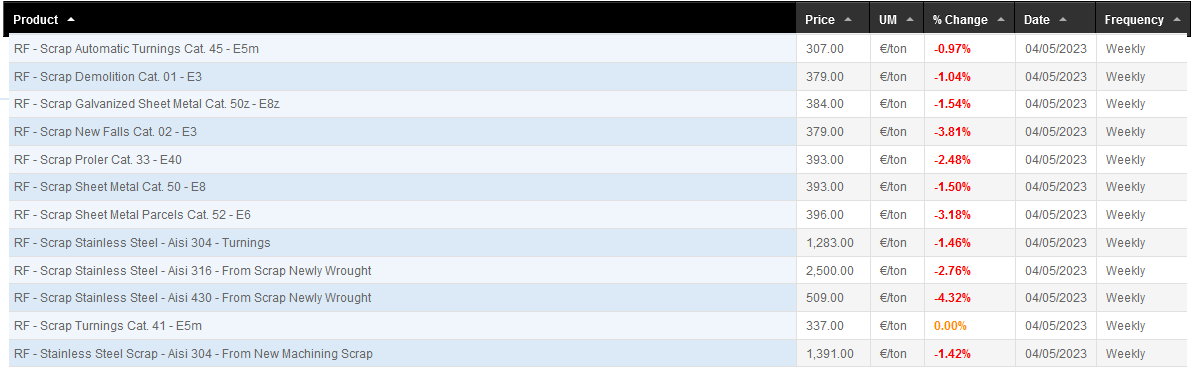

The Italian domestic scrap market was hit by numerous holidays and weak demand in April, with prices declining at the end of the month. The market started May with an uncertain outlook. This is mainly due to the reduction of the production tonnages of the rebar producers, who have received fewer orders.

The inability to regularly sell raw materials to steelmakers is partly due to steelmakers halting production due to technical problems or maintenance work. However, there could be a drop in prices in May despite low inventory levels from traders.

Since the beginning of the year, we’ve seen a market that has been consistently up and down. While we never want such a market, we have to live with this reality now. The wait-and-see attitude dominated the global scrap market in April. Prices in the European markets were more stable than in the Turkish and Asian markets, even though demand was not at an ideal level.

This is mainly due to the limited offer in the shredded segment. The downward movement accelerated towards the end of the month. The stainless steel market, on the other hand, spent the month of April at low levels both in terms of production and consumption. Italian steelmakers expect further price decreases despite low scrap supply.

Italian Ferrous Scrap – euro/ton – Powered by Commodity Evolution