Loading

Loading

Stay updated with Commodity Evolution to follow the industrial market trends and much more.

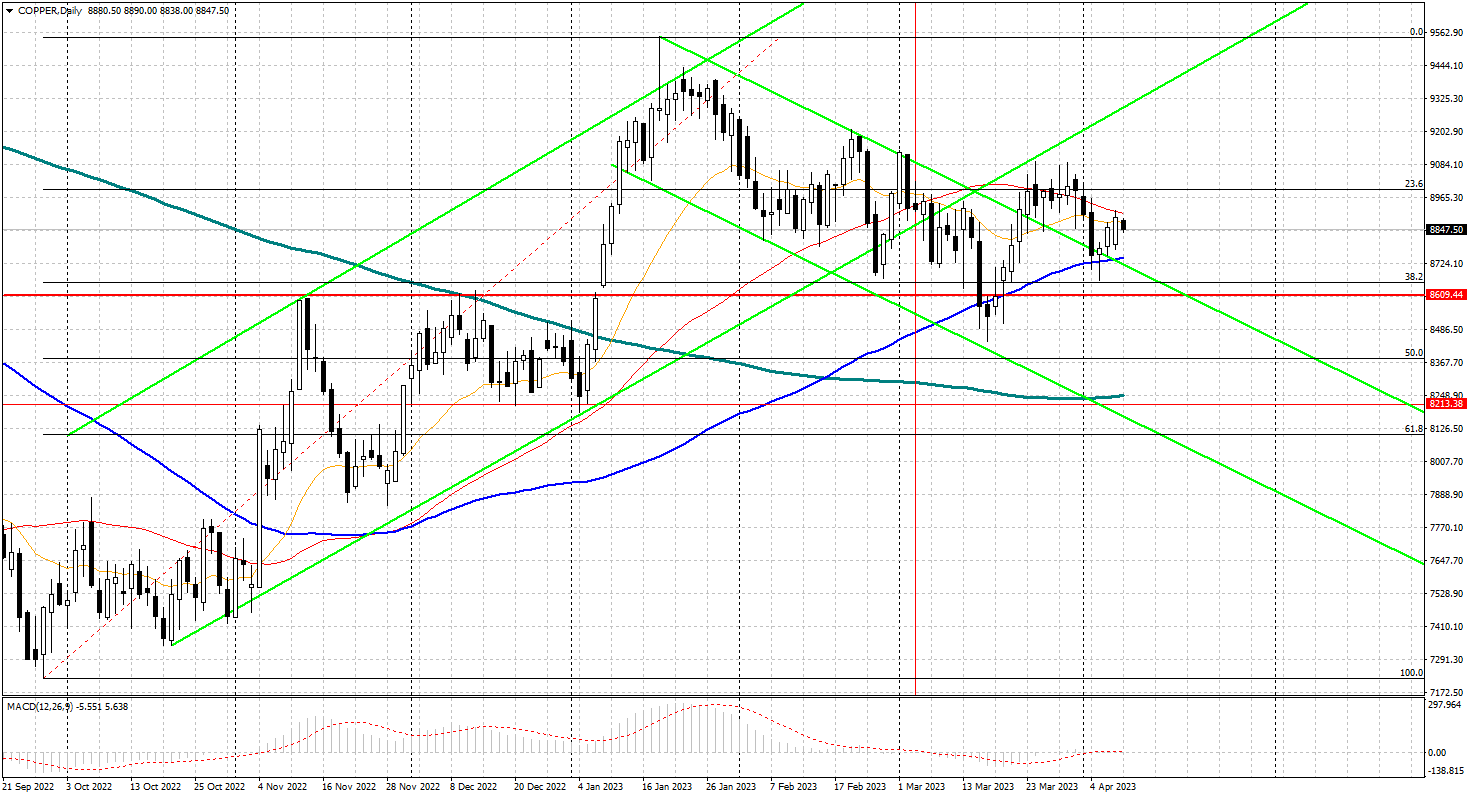

Copper prices continued to swing sideways last month, creating uncertainty and risk. Meanwhile, traders and investors continue to closely monitor the market for any signs of a breakout in either direction.

As prices move sideways, the copper market remains poised between worsening economic conditions in the West and a long-term bull narrative fuelled by an expected supply shortage. According to the International Monetary Fund, the world looks set for a sharp slowdown, the slowest economic growth since 1990.

In fact, Managing Director Kristalina Georgieva warned that growth could reach just 3% in the next five years. The slowdown is mainly due to high inflation, rising interest rates and the growing impact of multiple global crises.

In the US, the recent collapse of Silicon Valley Bank has already created a drag on lending, which will dampen domestic growth. Meanwhile, recent production cuts by OPEC+ will add upward pressure to global inflation.

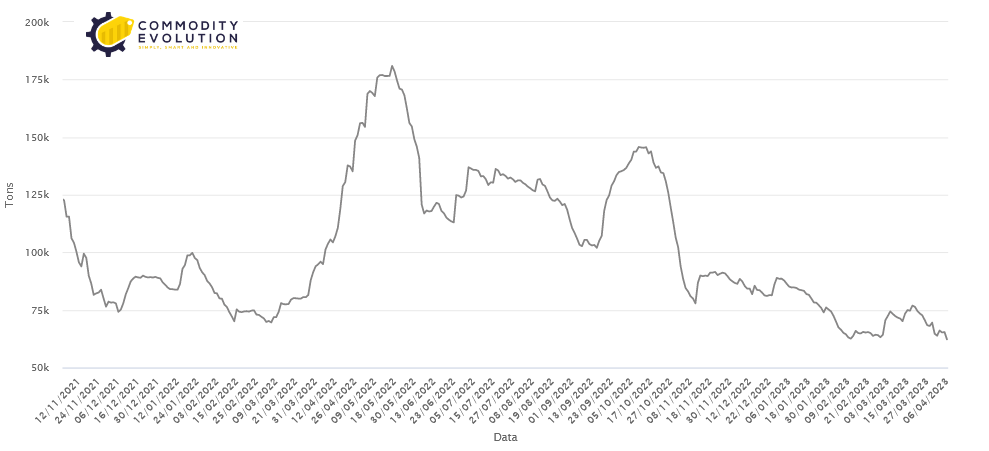

The reason why copper prices have not yet seen a significant downward breakout is partly because the global economic outlook does not paint the full picture. For example, LME stocks continue to fall and are now at their lowest levels since 2005.

Lme Copper stocks

In fact, many projections suggest that the ongoing transition to renewable energy will see demand continue to grow. Moreover, experts predict that demand will outstrip supply for the rest of the decade.

Although economic constraints may dampen demand at the consumer level, government-funded infrastructure projects will provide a strong counterbalance. Meanwhile, China’s economy continues to recover, albeit slowly, increasing pressure on supply. Simply put, copper supply is not sufficient to support growing global demand.

Of course, the long-term bullish narrative does not necessarily mean that copper prices are set to rise. Investment funds have already started to move away from bullish bets on copper. The investment community has turned sharply short on CME copper for the first time in five months.

Historically, US recessions are always associated with a decline in copper prices. This is a phenomenon that many investors seem to expect in a worsening economic outlook. However, the scarcity of supply will limit the extent of this downturn, should it materialise.

On the supply side, Chile, the world’s largest copper producer, could provide little relief. According to the Chilean Copper Commission, production fell by 3.4% in February. Although the commission still expects production to grow over the next seven years, numerous delays in various mining projects will slow down growth more than initially expected.

Meanwhile, the turmoil in Peru seems to have subsided as production resumed at the copper mines affected by the blockades. While the risk of stoppages remains, both Las Bambas and Antapaccay have gradually resumed mining in recent months and are now operating at full capacity.

In February, according to data from Peru’s National Institute of Statistics and Information, copper production increased by 10.8% year-on-year. This came after production had declined in January. To further relieve global supply, the Peruvian Ministry of Energy and Mines announced that 39 new copper mining projects will become operational in 2023.

Copper – 3 month $/ton daily