Loading

Loading

Aluminium will be the hardest hit with tariffs of 200% on imports of Russian metal, effective 10 March, and on imports of any third country products containing Russian metal, effective 10 April.

Aluminium will be the hardest hit with tariffs of 200% on imports of Russian metal, effective 10 March, and on imports of any third country products containing Russian metal, effective 10 April.

Tariffs on imports of other metals, such as copper and lead, will double to 70%, while nickel will be subject to a 35% duty. The comprehensive package of sanctions and trade measures, announced on the anniversary of the Russian invasion of Ukraine, covers more than 100 metals, minerals and chemicals.

The market reaction was muted. The duties on aluminium were widely expected and are unilateral US trade measures, not formal sanctions like those briefly imposed on Russian producer Rusal in 2018 with chaotic impact.

The LME was pressured to suspend all deliveries of Russian aluminium into its global warehouse network, but rejected the proposal in November. The LME does not believe that the recent US announcement changes this position, as many US consumers had already ‘self-suspended’ against Russian metal.

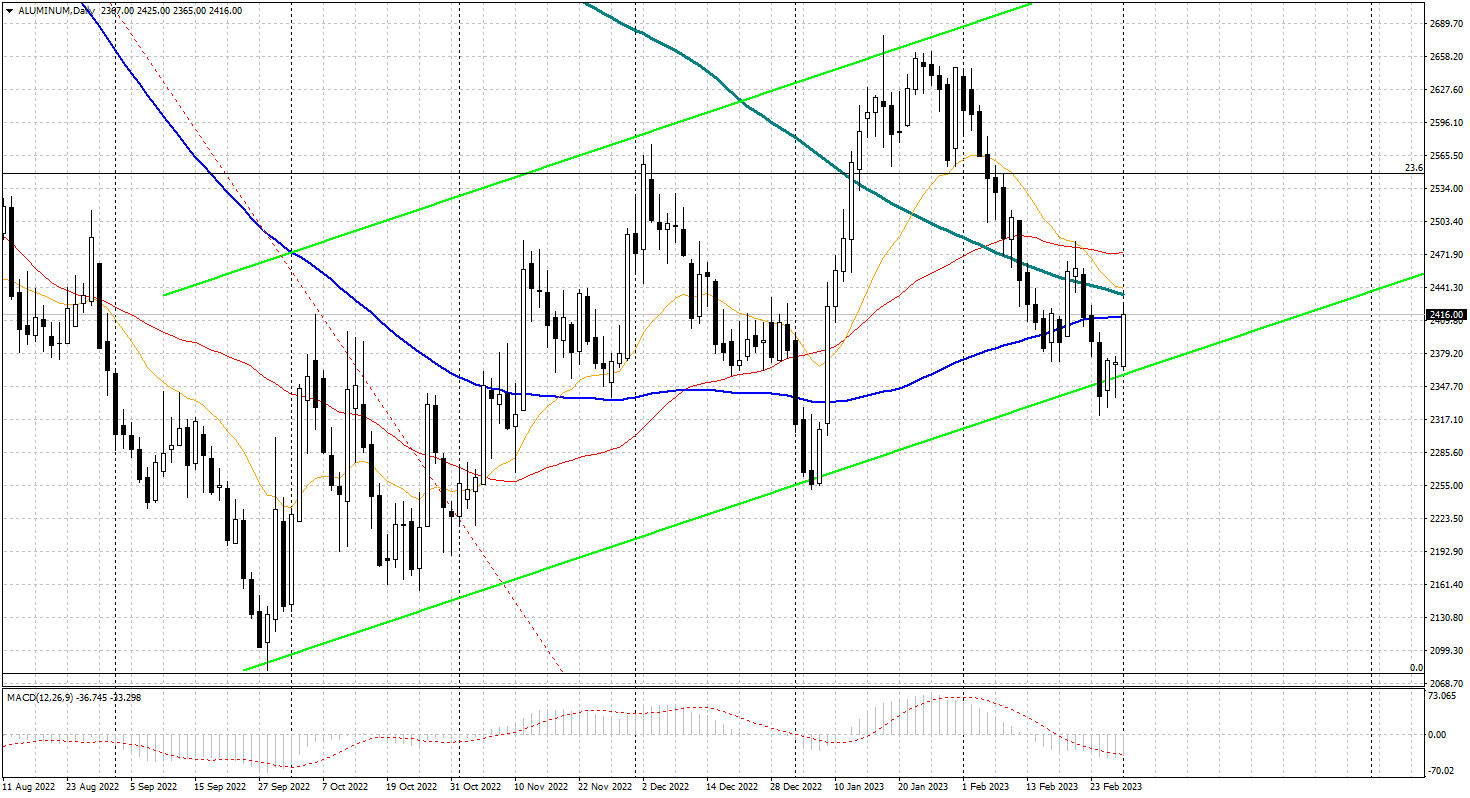

The LME’s three-month aluminium price was the subject of a flurry of selling in the hours following the 24 February announcement, in what appeared to be a mass dumping of Russian brands by securities lenders.

Aluminium will be the hardest hit with tariffs of 200% on imports

The result was an explosion in the cash-three-month contango to $50.50 per tonne at the weekly close, the widest since 2013, when there were over five million tonnes of LME aluminium stocks to finance. The gap narrowed marginally on Monday, when the time spread closed the day at $46.75 per tonne.

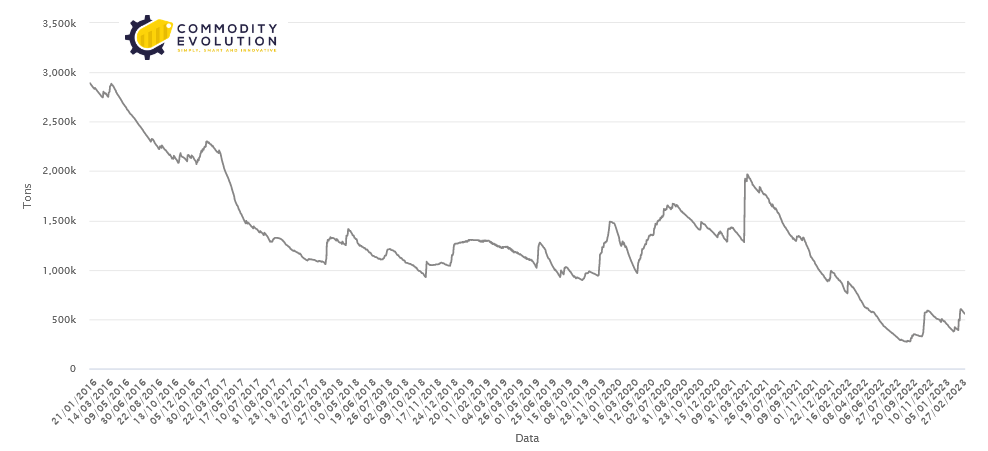

This sort of ‘super contango’ is the market’s cry for lenders to pick up spare metal, particularly Russian metal. At the end of January, LME warehouses held 93,750 tonnes of Rusal aluminium, 41% of the total escrow stock of 231,125 tonnes.

Since then, warranty stocks have grown to 443,675 tonnes, following strong warranty activity at the Malaysian port of Klang (121,150 tonnes) and the South Korean port of Gwangyang (107,900 tonnes).

Deliveries to Gwangyang would consist of Russian aluminium delivered by Glencore, which has a long-term off-take agreement with Rusal.

Aluminum Warehouse tons

Trade tariffs are not sanctions, and there is no reason why this metal will not find financing, but Friday’s collapse in the cash price suggests that the liquidity pool may have shrunk.

The US said it had calibrated its import duties ‘to impose costs on Russia while minimising costs to US consumers’.

US imports of Russian raw aluminium fell sharply after the country imposed sanctions on Rusal in 2018, although they were lifted the following year.

Russian metal flows amounted to 744,000 tonnes in 2017. Last year it was only 209,000 tonnes and Russia had dropped to fifth place among suppliers, according to the Aluminum Association.

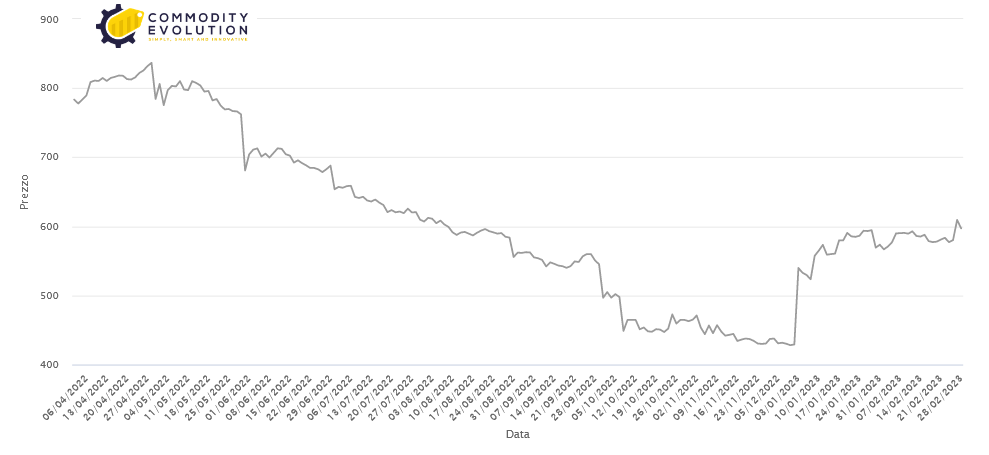

This tonnage will have to be replaced by other supplier countries, sustaining the premium for physical metal in the US market.

Aluminium premium Us MidWest – euro/ton

Asian buyers, on the other hand, can buy spot metal at a premium of $72 per tonne right now or $85-86 per tonne if they have a quarterly delivery contract.

US consumers could take a double hit, as duties will be extended in April to any aluminium product that includes Russian metal, wherever it was manufactured. The US imports a wide range of semi-finished products, including sheets, tubes, wire, plate, rods and bars.

But it is worth mentioning that Rusal produces almost four million tonnes of aluminium annually, most of which is exported. Only a fraction of these tonnes is imported directly to the US as raw metal.

The only way out for the supplier countries is for them to also impose minimum tariffs of 200% on their imports of Russian aluminium. Aluminium now seems to be part of the wider geopolitical rift opening across the critical minerals spectrum as the West seeks to reduce its dependence on China and Russia.