Loading

Loading

Shanghai, China’s most internationalised city and the largest steel trading hub in eastern China, has been under a strict lockdown since 28 March to combat the worst outbreak of COVID-19 ever seen in terms of the number of infections. The citywide blockade has nearly halted steel delivery and consumption in Shanghai, and the impact has spread to other regions of the country.

Shanghai introduced four blockade days in the eastern and western half of the city in succession from 28 March, but they were soon extended and replaced with a general blockade covering the entire city from 5 April. There is no news about the end of the blockade, as new daily infections continue to grow steadily.

Transport, especially by truck, has been banned, except for those delivering essential goods. Thus, the delivery of steel and raw materials by truck was stopped, and warehouses for the steel trade were closed. Outdoor construction activities were also suspended during the blockade.

The steel market has been almost stopped, there are no purchases by end users and speculative trading also remains quiet.

Baoshan Iron & Steel Co (Baosteel) in Shanghai, a subsidiary of the world’s largest steel producer, China Baowu Steel Group, is the only steel mill in Shanghai. Its steel plant, with a finished steel capacity of about 16 million tonnes per year, produced normally until 8 April, avoiding the interruptions caused by the pandemic outage.

The company planned ahead by stocking up on raw materials for up to 14 days of use before the blockade. And essential working personnel are also quarantined on site to ensure that normal production is maintained.

Baosteel’s steel plant and its application of industrial robots allow remote control of operations and therefore requires fewer employees on site.

In addition, Baowu’s platforms for unloading and transporting raw materials to the plants are in normal operation, with special licences granted by the government to ensure that the extra raw material can be delivered on time.

However, stagnating demand for steel and transport disruptions have slowed the delivery of steel products to the market, which has led to stocks of finished steel piling up.

Other steel mills that rely heavily on trucks to transport raw materials have not been as fortunate as Baosteel, as various restrictive measures have also been introduced locally to prevent the spread of the virus, although the number of infections has been much lower than in Shanghai.

Two steel mills, Xusteel Group and Zhongxin Iron and Steel Group in Jiangsu, eastern China, both announced on 6 April that they were shutting down a 1,280 cubic metre blast furnace for maintenance.

Some Chinese analysts believe that COVID-19 has had a more direct impact on steel demand than on supply, but in the meantime China’s domestic steel prices have been supported mainly by market expectations and high production costs, rather than their real fundamentals.

Shanghai is one of the largest steel consumption bases in China, and its blockage has dragged down the country’s overall steel consumption.

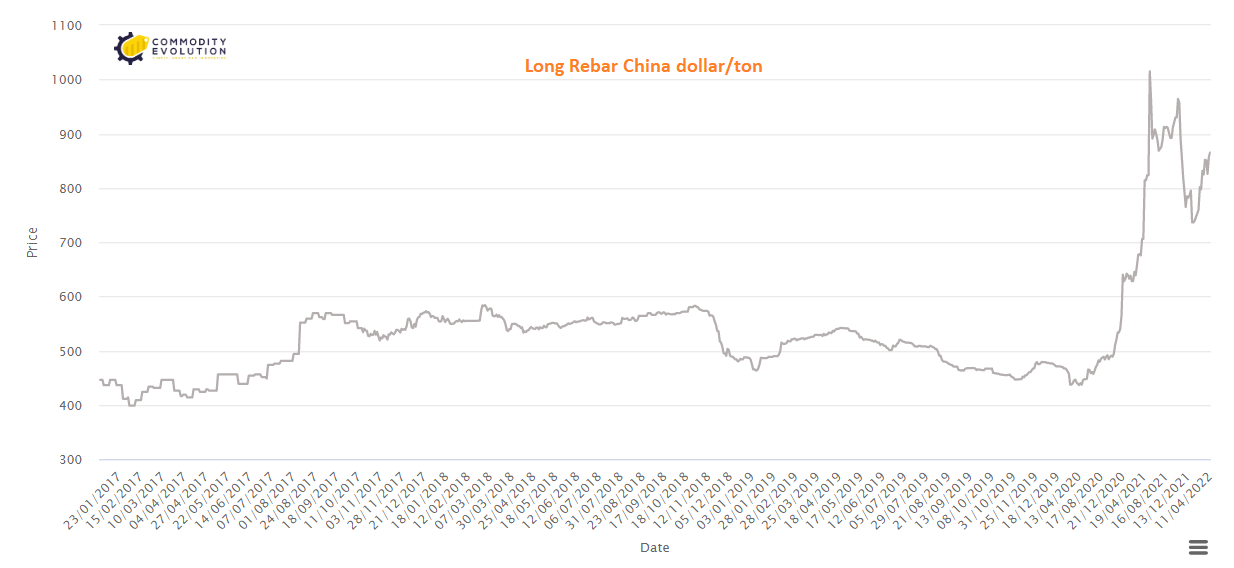

The daily trading volume of rebar, wire rod and coiled bars for construction in China from 28 March to 8 April during the blockade averaged 174,423 tonnes per day, down 36% from a year earlier.

This year, the market’s focus is really on the demand side, as it is almost certain that Chinese mill production and the country’s steel supply will recover, although it remains unclear how much demand will improve this year.

That’s different from last year, when the market’s focus was on the supply side, as participants in the entire steel market wondered whether China’s order to cut crude steel production in 2021 from the previous year would be realised.

In terms of steel demand this year, there has been a stark contrast between a strong expectation of steel demand with a number of stimulus policies that are or will be introduced by Beijing and the reality that steel demand is still largely held back by the pandemic.

he optimistic outlook may continue to support steel prices for now. However, if steel demand turns out to be less good than expected or if the freeze lasts longer than expected, until April or even May, the traditional peak season for steel consumption, the market may then see some price correction.