Loading

Loading

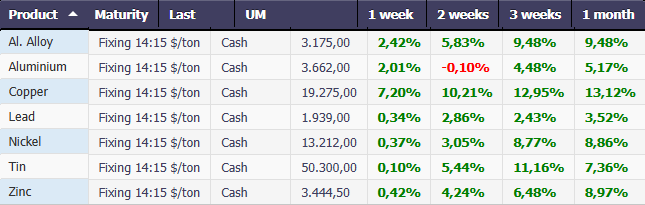

The start of April marks a shift in tone for non-ferrous metals listed on the LME, with a broad-based recovery in both dollar and euro prices. After weeks of weakness in the previous period, the sector is now showing signs of strengthening in the short and medium term, albeit with varying degrees of intensity across metals.

In dollar terms, the movement appears particularly solid. Nickel leads the rise with a monthly performance of +13.12%, followed by copper (+8.86%) and zinc (+8.97%), all signs of renewed industrial reactivity. Tin also shows a significant recovery (+7.36%), while aluminum moves more gradually (+5.17%), confirming a more stable trend compared to other metals.

In the short term, weekly changes confirm the positive trend: nickel records a strong +7.20%, while the rest of the sector moves with smaller but widespread increases, a sign of a market regaining momentum.

Euro: The Recovery Consolidates and Broadens

The euro reading further reinforces this scenario. The exchange rate effect contributes to amplifying certain dynamics, but does not alter the underlying picture: the rise is consistent and across the board.

Nickel remains the best-performing metal also in euro (+10.69% monthly), followed by zinc (+6.63%) and copper (+6.52%). Tin also maintains a strong pace (+5.06%), while aluminum shows a more modest recovery (+2.91%), consistent with its more defensive nature.

A Sign of Recovery, But Yet to Be Confirmed

The overall message is clear: the non-ferrous metals sector is experiencing a technical and cyclical rebound, with widespread signs of strengthening across all major commodities.

However, the nature of this movement must be interpreted with caution. The strength of nickel and copper suggests a possible improvement in industrial expectations, but the still moderate momentum of aluminum indicates that demand is not yet fully consolidated.

In this context, the ongoing recovery represents an initial positive sign, but not yet definitive confirmation of a reversal of the cycle. The market therefore remains in a transition phase, in which the rebound in prices must be supported by a real recovery in demand to consolidate.

Performance Metals Cash $/ton

Performance Metals Cash €/Bloomberg

Copper: An Increasingly Complex Market Amid Constraints and Fragility

The global copper market is entering a decidedly more complex phase, in which traditional supply and demand logics are no longer sufficient to explain price movements.

Geopolitical tensions, rising energy costs, and macroeconomic uncertainty are redefining the balance of the entire supply chain, creating a context in which growing supply risks coexist with still-fragile demand.

The result is a difficult market to read, where signals are often conflicting and the direction less predictable than in the past.

The Sulfuric Acid Concern and Production Pressure

One of the most critical issues emerges on the production side, particularly for the SX-EW segment. In key countries such as Chile and the Democratic Republic of the Congo, the real constraint is no longer just the cost, but the very availability of sulfuric acid, an essential component of the extraction process.

The problem arises upstream: supplies of sulfur, from which the acid is derived, have been affected by logistical disruptions in the Middle East, generating a ripple effect along the entire supply chain.

In the short term, many operators are still managing to maintain production levels thanks to inventories, but the situation remains fragile: the sustainability of supply in the medium term is increasingly uncertain.

Sulfuric Acid 78%-80% – Europe $/ton

Persian Gulf: A Systemic Risk to Supply

Making the situation even more delicate is the strong geographic concentration of sulfur supply. The Persian Gulf accounts for approximately a quarter of global production, making the system particularly exposed to regional shocks.

In this context, the sulfuric acid market is assuming an increasingly central role, becoming a leading indicator of tension in the copper sector, sometimes even more relevant than traditional fundamentals.

China: An Increasingly Unstable Equilibrium

Chinese dynamics are further increasing uncertainty. In recent years, China has assumed a key role as an exporter of sulfuric acid, but early signs in 2026 point to a possible shift in strategy.

The decline in exports suggests a growing focus on domestic supply security, with the risk of reducing global availability.

This factor could amplify supply pressure, making the market even more unstable and dependent on political decisions.

Negative Treatment Charges: A Signal of a Distorted Market

Supply-side tensions are also clearly reflected in the concentrate market. Treatment charges have fallen into negative territory, indicating a profound imbalance between smelting capacity and raw material availability.

In this scenario, smelters are paying to secure concentrate, reversing the traditional market dynamic.

Rising sulfuric acid prices are partially offsetting this pressure, but they are creating a growing dependence on an external and volatile factor, increasing risks in the medium term.

Energy and Logistics: Widespread Pressure Across the Supply Chain

At the same time, energy costs continue to be a cross-cutting driver. Rising oil, diesel, and transportation prices are impacting every stage of the value chain.

The consequences are clear:

- Higher production costs;

- Slower and more expensive logistics;

- Pressure on margins.

In many mining areas, diesel plays a particularly critical role, amplifying the overall cost impact.

Global Demand: Weak and Highly Price-Sensitive

While the supply side appears fragile, the demand side offers little stability. The global economic slowdown and geopolitical tensions are reducing operators’ visibility and confidence.

In Asia, and especially in China, a very clear dynamic emerges: demand is extremely responsive to prices.

- Falling prices → Rebounding purchases;

- Rising prices → Rapidly declining demand.

This behavior highlights opportunistic, rather than structurally sound, demand.

Physical Premiums and Regional Signals

Demand dynamics are also reflected in physical premiums:

- stability in Shanghai, a sign of a precarious balance;

- a marked decline in Southeast Asia, where final demand remains weak.

In some cases, operators are even postponing shipments, highlighting a still-uncertain consumption environment.

China Copper Premiums $/ton

Copper: Between Technical Rebound and Structural Fragility

After weeks of high volatility, 3-month LME copper is consolidating above $13,000/t, recently closing around $13,155/t.

The chart clearly shows how, after the sharp decline recorded between late March and early April, the market responded with a well-structured technical rebound, quickly returning to previous levels.

However, this recovery is taking place within a context that remains far from linear.

Technical Structure: Recovery Underway But Without Breakout

From a technical perspective, the movement of the last few days shows:

- a recovery above the short-term moving average;

- an improvement in momentum (as evidenced by the lower indicator);

- a return to the key resistance area.

The area between $13,200 and $13,500/t represents a critical zone, already tested several times in recent months without a definitive breakout.

The lack of acceleration above these levels suggests that the market is entering a phase of high-tension sideways movement, rather than a new structural uptrend.

Copper LME – 3 month $/ton

Price Target for May 2026

Given the current structure, three main scenarios can be identified for the month of May:

Base Scenario

- Range: $12,700 – $13,500/t;

- A sideways market, with unconfirmed breakout attempts;

- Volatility related to macroeconomic and geopolitical news.

China: Destocking Underway But Weak Demand

In China, the market is in a transitional phase between destocking and demand uncertainty. Domestic prices are hovering around 3,290–3,300 yuan/t, supported by a reduction in company inventories.

However, demand remains the main source of weakness:

- Operators are purchasing cautiously;

- volumes remain limited;

- visibility is limited.

On the export front, prices are hovering around $483/t FOB, with offers as high as $490–500/t, but high logistics costs are holding back competitiveness.

At the same time, the issue of green steel is emerging, with premiums of up to 800 yuan/t, introducing a new structural component in prices linked to the energy transition.

Momentum and Positioning: Signs of Recovery But Not Yet Solidity

The momentum indicator shows a clear reversal from the April lows, returning to positive territory. This suggests that the market has regained strength in the short term, but has not yet built a sufficiently solid base.

In other words, the current movement appears more like a technical rebound than the start of a new bull cycle.

Fundamentals and Technical: Only Partially Aligned

Technical analysis integrates perfectly with the fundamental framework already highlighted.

On the one hand, supply factors continue to support the market:

- Tensions over sulfur and sulfuric acid;

- high energy costs;

- logistics challenges.

On the other hand, demand remains the main source of uncertainty:

- price-sensitive behavior in China;

- weakness in Southeast Asia;

- a still fragile macroeconomic environment.

This explains why, despite the recovery in prices, the market is unable to develop a strong upward trend.

Conclusions: May Will Be a Test Month

May will be a key month for copper.

The market is currently in an intermediate position:

- strong enough to recover in the short term;

- but not solid enough to sustain a structural breakout.

The $13,500/t threshold will be the level to monitor: a convincing break would open the way for further increases, while a failure could quickly push the market back toward lower support.

Consistent with fundamental analysis, copper remains a market driven by opposing forces: supply constraints on one side, fragile demand on the other. And it is precisely this unstable equilibrium that will continue to define price movements in the short term.

Commodity Evolution is the ideal solution to support the budgeting and negotiation activities of your corporate purchasing department.

Access to the platform allows you to view real-time prices and comprehensive market information for metals, steel, scrap, and many other sectors, with more than 1,500 products.

Request a Free Demo

Disclaimer

This document was prepared by Commodity Evolution. It is intended for consultation by those to whom it is addressed and, in any case, is not intended to replace the personal judgment of those to whom it is addressed. While Commodity Evolution has taken the utmost care in preparing this document and believes its contents to be reliable, it assumes no responsibility for the accuracy, completeness, or currency of the data and information contained therein or on the resources and data used to prepare it. Consequently, Commodity Evolution declines all liability for errors or omissions. The opinions, forecasts, or estimates contained in this document are expressed exclusively as of the date of this document’s preparation, and there is no guarantee that future results or any other future events will be consistent with the opinions, forecasts, or estimates contained herein. Any information contained in this document may be subject to changes or updates after the date of its preparation, without any obligation to communicate such changes or updates to those to whom this document has previously been distributed. This publication is provided to you for information and illustration purposes only and does not constitute a public offering of financial products or a promotion of investment services and/or activities, either to residents of Italy or to residents of other jurisdictions. Neither Commodity Evolution nor any of its directors, representatives, or employees assumes any liability, in whole or in part, for any damages (including, but not limited to, damages for loss of profits, business interruption, loss of information, or other economic losses of any nature) arising from the use, in any form and for any purpose, of the data and information contained in this document.