Loading

Loading

Update as of December 01 – Industrial metals trend – November 2025

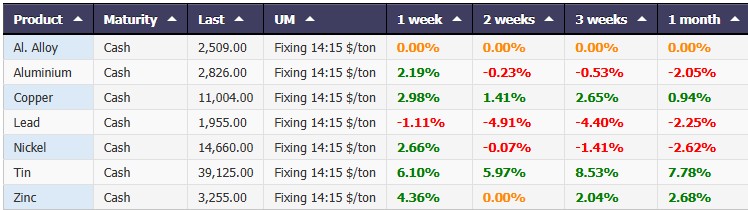

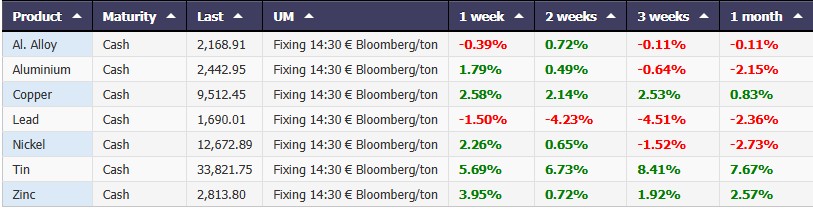

Over the past month, the industrial metals complex has exhibited mixed performance, reflecting a fragile balance between more constructive macroeconomic signals and real demand that, especially in Europe, is still struggling to consolidate. Analysis of performance in dollars and euros reveals a consistent picture: some metals have had a strong month, while others continue to move in a downward trend that has persisted for weeks.

Among the best performers, tin stands out, the undisputed star of the period. Supported by the renewed dynamism of the electronics sector, the metal posted a gain of nearly 8% in both dollars and euros, confirming its role as the sector’s driving force. This result reflects market optimism regarding the recovery in demand for components and semiconductors, after months of high volatility.

Zinc is also in positive territory, rising approximately 2.6% in both currencies. The movement, less dramatic than that of tin, is nevertheless significant: it suggests a market that is gradually absorbing surpluses and regaining a certain balance between supply and industrial use, especially in Asia.

Copper, a barometer of the global economy, closed the month with a more modest gain—around 1%—but still positive. The moderate growth reflects a more stable sentiment, with traders observing improved trading fluidity between the LME and SHFE and less negative signals on the Chinese macroeconomic front.

By contrast, three metals continue to show structural weakness. Aluminum fell just over 2% in both dollars and euros, penalized by a still-sluggish real demand environment in Europe, high inventories in China, and industrial sentiment struggling to establish a more solid trajectory.

Nickel’s decline was even more pronounced, falling between -2.6% and -2.7%, weighed down by the ample availability of Indonesian products and depressed NPI prices, which continue to exert pressure on the global market.

Lead also contracted, dropping by around -2.3%. The traditional battery sector shows no signs of recovery, and the metal is suffering as a result, moving within a well-established downward trend.

Overall, the month was characterized by a clear on the other, a group—aluminum, nickel, and lead—still struggling with a fragile equilibrium and with downward pressures affecting their performance.

Industrial Metals Cash Performance $/ton – Powered by Commodity Evolution

Industrial Metals Cash Performance €/ton Bloomberg – Powered by Commodity Evolution

Italian Scrap Metal – A Calm Only Seemingly Ahead of the December

No surge, no acceleration: over the past week, the Italian ferrous scrap market has continued to move in a climate of quiet stability.

Traders speak of a “substantially balanced” phase, almost suspended, which has now lasted for several weeks without significant changes.

Yet, behind this apparent immobility, something is beginning to move.

The atmosphere of December—traditionally a complex month for the entire supply chain—brings with it an increasingly evident shift in sentiment: the horizon seems to be moving toward a bullish trend.

December Approaches: Upward Adjustments Expected

According to information gathered by Commodity Evolution, traders expect increases of between 5 and 10 euros per ton.

A limited increase, but significant when compared to a market that has remained almost flat in recent months.

“So far, we haven’t seen any real increases, except for isolated cases,” explains a steel operator. “And even if the market were to move, it would be within that range.”

A sentiment that is also strengthening thanks to signals from abroad – and especially from Turkey.

Italian Ferrous Scrap Euro/ton – Powered by Commodity Evolution

The Turkey Factor: Rising Imports and Price Pressure

Turkey, a benchmark for the international scrap market, is experiencing a decidedly more buoyant phase.

The latest HMS 1/2 80:20 transactions have exceeded the psychological threshold of $360/t CFR, a level that is also starting to influence the expectations of Italian operators.

The strengthening Turkish market, combined with European stability, is contributing to a scenario in which December appears anything but calm.

LME Steel Scrap TSI HMS 80:20 CFR – Turkey $/ton – Powered by Commodity Evolution

December: Shutdowns, Holidays, and Complicated Logistics

December is historically a challenging month for the scrap market – and 2024 will be no exception.

Many steel mills have already scheduled shutdowns and maintenance, while others have notified suppliers that they will not place contracts during the month. This decision responds to the need to optimize costs and inventories during a period characterized by fewer working days and more complex logistics.

A manager sums up the situation well: “I have given foreign suppliers the option to deliver until December 19th. From the following day, we will stop and restart on January 7th.”

In the background, foreign markets are also facing obstacles: international holidays and winter weather conditions tend to reduce material availability, increasing pressure on supplies.

Upward Pressure: Reduced Availability and Boost from Turkey

The testimonies collected by Commodity Evolution converge on one clear fact: those who need to buy scrap in December will likely have to pay more.

Limited availability, longer handling times, and price increases on foreign markets are pushing both Italian and foreign suppliers to increasingly talk of upward adjustments.

“The impression is that those who need to buy in December will have to dig deep into their pockets,” summarizes one operator.

A Supply Buffer: Ships Arriving from Abroad

A scheduled arrival could at least partially mitigate the tensions: a group of companies is expecting a shipload of scrap to dock in Marghera around Christmas, with unloading scheduled for the end of December.

This strategic replenishment will allow the steel mills involved to restart in January with well-stocked fleets, reducing the urgency to purchase in a potentially tense market.

A single ship won’t be able to rebalance the entire month, but it still represents a precious breath of fresh air.

Conclusion: Stability Is Just a Facade

The Italian scrap market appears stable, but its stability is deceptive: more than immobility, it’s a precarious balance that precedes a potential movement.

On the one hand, upward pressures are compounding:

- reduced logistics,

- production shutdowns,

- holidays, a boost from Turkey.

On the other, there are factors that could dampen the rise:

- scheduled arrivals from abroad,

- consumption slowed by shutdowns,

- some room for maneuver on inventories.

“It remains to be seen,” observes one operator, “whether this will be a flash in the pan due to holidays and logistics, or the basis from which we will restart in January.”

For now, the market remains suspended.

But December could represent the first real turning point and lay the foundation for the Italian scrap market in 2025.

Commodity Evolution is the ideal solution to support the budgeting and negotiation activities of the corporate purchasing department.

Access to the platform will allow you to view real-time prices at any time and a lot of information relating to the market of metals, steel, scrap and many other reference sectors, with more than 1,500 reference products.

Request a Free Demo

Disclaimer

This document has been prepared by Commodity Evolution. This document is intended for consultation by the subjects to whom it is addressed, and, in any case, is not intended to replace the personal judgment of the subjects to whom it is addressed. Although Commodity Evolution takes the utmost care in preparing this document and considers its contents to be reliable, it does not assume any responsibility for the accuracy, completeness and timeliness of the data and information contained or present on the resources and data used for the purposes of its preparation. Consequently, Commodity Evolution declines all responsibility for errors or omissions. The opinions, forecasts or estimates contained in this document are formulated with exclusive reference to the date of drafting of this document, and there is no guarantee that future results or any other future event will be consistent with the opinions, forecasts or estimates contained herein. Any information contained in this document may, after the date of drafting of the same, be subject to any modification or update, without any obligation to communicate such modifications or updates to those to whom this document has previously been distributed. This publication is provided to you for information and illustration purposes only, and does not constitute in any case an offer to the public of financial products or promotion of investment services and/or activities either towards persons resident in Italy or persons resident in other jurisdictions. Commodity Evolution, nor any of its directors, representatives or employees assume any type of liability, in whole or in part, for damages (including, by way of example, damages for loss or lack of earnings, interruption of business, loss of information or other economic losses of any nature) arising from the use, in any form and for any purpose, of the data and information contained in this document.