Loading

Loading

Update as of August 29 – Industrial Metals Trends – September 2025

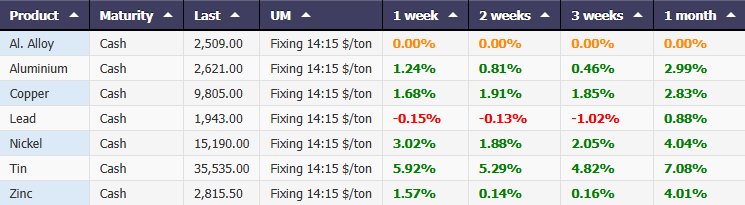

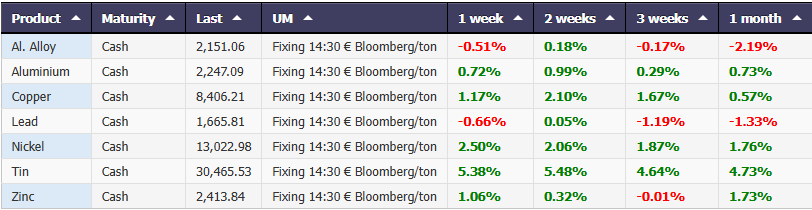

Industrial metals showed mixed trends over the past month.

In dollars, performance was overall positive: tin led the gains with a +6.40% monthly gain, followed by aluminum (+1.36%), nickel (+1.45%), and copper (+1.01%). Signs of weakness were seen in zinc (–0.16%) and, to a marginal extent, lead (+0.21%).

In euros, the dollar’s devaluation mitigated gains and accentuated losses. Tin remained the best performer (+4.41% monthly), while aluminum (–0.55%), copper (–0.88%), and zinc (–2.04%) closed in negative territory. Lead (–1.68%) and nickel (–0.45%) showed similar trends, penalized by the exchange rate.

Overall, July was a month of consolidation, with positive signs especially for tin, nickel, and aluminum, while zinc continues to show greater fragility.

Performance Metals Cash $/ton – Powered by Commodity Evolution

Performance Metals Cash €/ton Bloomberg – Powered by Commodity Evolution

US-EU Agreement: Between Diplomatic Progress and Unresolved Issues

The new trade framework between the United States and the European Union, announced on August 21, marks an important step toward greater tariff harmonization but still leaves many uncertainties unanswered.

For the European automotive sector, Washington’s decision to maintain, at least temporarily, the 27.5% tariff represents a significant setback. The proposed reduction to 15% is contingent on a European legislative move reducing tariffs on American industrial and agricultural goods: a clause that ties the future of tariffs to a complex and potentially lengthy political process.

The majority of European goods exported to the United States will instead benefit from a harmonized 15% tariff, including strategic sectors such as timber, semiconductors, and pharmaceuticals. However, for steel and aluminum, the issues remain unresolved.

Steel and Aluminum: The Burden of Section 232

European exports to the US continue to face punitive 50% tariffs under Section 232 of the Trade Expansion Act. This is compounded by a further obstacle: the expansion of the list of affected products, which as of August 18th includes 407 new customs codes for steel and aluminum derivatives.

To offset these measures, the parties have agreed to introduce tariff rate quotas (TRQs), which should allow regulated access to the US market without sacrificing a high level of protection for local producers. However, the specific parameters for their implementation remain uncertain: according to analysts at Commodity Evolution, the quotas could be based on historical volumes, while excess quantities would be subject to the full 50% tariff.

Impact on the Automotive Sector and Steel Production

The European automotive sector, which accounts for approximately 20% of the continent’s steel demand, risks significant pressure. The tariffs introduced by the Trump administration have not only penalized European exporters but have also increased costs for US producers, compressing their margins.

In 2024, European carbon steel exports to the US reached 2.5 million tonnes, up 31% compared to 2023, but still far from the pre-tariff levels of 2018, when shipments exceeded 3 million tonnes.

European Outlook

At the same time, Brussels is also preparing new measures: the public consultation on the future trade policy for steel closed on August 18, with broad consensus on the adoption of TRQs. The Commission is expected to present a definitive system by the third quarter of 2025, intended to replace the current safeguards from July 1, 2026.

The objective remains to balance protection from global production surpluses with the need to maintain an open, yet regulated, EU market.

The agreement between the US and the EU can be seen as a step towards détente, but the path to stabilizing relations is far from complete. The reduction of tariffs on automobiles remains contingent on European legislative decisions, while the TRQ system for steel and aluminum is still lacking operational details.

The coming months will be crucial to understanding whether this framework will transform into a lasting balance or whether, conversely, new trade tensions will once again dominate transatlantic relations.

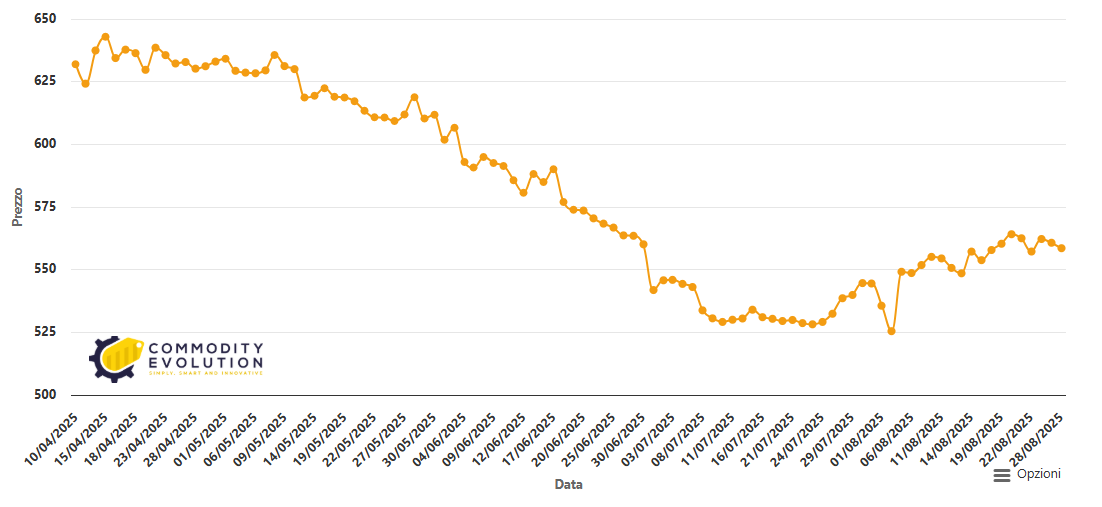

Northern European HRC Steel: Prices Near Bottom, Signs of Stabilization

Over the past few months, the European HRC (Hot Rolled Coil) market has undergone a rather marked decline. From a peak of over €640/t recorded in April 2025, prices have embarked on a steady downward trend, reaching lows in the €520–530/t range in July.

The chart clearly shows how the downward pressure was driven by weak demand and low-cost Asian imports, which significantly impacted the European domestic market. This is compounded by regulatory uncertainties related to the CBAM, the European Border Emissions Adjustment Mechanism, which will come into force in 2026 but is already influencing purchasing decisions.

Hot-Rolled Coils HRC – Northern Europe Euro/ton – Powered by Commodity Evolution

Consolidation Phase

In the final weeks of August, prices appear to have found a base, fluctuating steadily between €540 and €560/t. This sideways movement signals that the market may have already priced in most of the downward pressure, although a clear recovery momentum is still lacking.

Supply and Demand

- Weak demand: User sectors (particularly construction and automotive) remain cautious, postponing purchases while awaiting greater clarity on price direction;

- Excess supply: The influx of low-cost materials, especially from China, continues to weigh, even as the EU is considering tighter import restrictions through tariffs;

- Pressure on margins: Many European producers are currently operating near or below production costs, a condition that could lead to capacity cuts if prices remain at these levels.

Short-Term Outlook

For September 2025, the most likely scenario is a continuation of the sideways stabilization phase in the €540–560/t range, with possible technical rebounds if signs of a recovery in demand emerge. A marked strengthening in prices, however, remains linked to:

- More stringent EU measures against low-cost imports;

- A recovery in demand in the automotive and construction sectors;

- A reduction in global oversupply, particularly in Asia.

Conclusion

The HRC market in Northern Europe is currently nearing a fragile equilibrium: prices have likely bottomed out, but recovery is still uncertain and will depend both on regulatory changes and macroeconomic trends in the second half of the year.

Commodity Evolution is the ideal solution to support the budgeting and negotiation activities of the corporate purchasing department.

Access to the platform will allow you to view real-time prices at any time and a lot of information relating to the market of metals, steel, scrap and many other reference sectors, with more than 1,500 reference products.

Request a Free demo of our platform for one week

Disclaimer

This document has been prepared by Commodity Evolution. This document is intended for consultation by the subjects to whom it is addressed, and, in any case, is not intended to replace the personal judgment of the subjects to whom it is addressed. Although Commodity Evolution takes the utmost care in preparing this document and considers its contents to be reliable, it does not assume any responsibility for the accuracy, completeness and timeliness of the data and information contained or present on the resources and data used for the purposes of its preparation. Consequently, Commodity Evolution declines all responsibility for errors or omissions. The opinions, forecasts or estimates contained in this document are formulated with exclusive reference to the date of drafting of this document, and there is no guarantee that future results or any other future event will be consistent with the opinions, forecasts or estimates contained herein. Any information contained in this document may, after the date of drafting of the same, be subject to any modification or update, without any obligation to communicate such modifications or updates to those to whom this document has previously been distributed. This publication is provided to you for information and illustration purposes only, and does not constitute in any case an offer to the public of financial products or promotion of investment services and/or activities either towards persons resident in Italy or persons resident in other jurisdictions. Commodity Evolution, nor any of its directors, representatives or employees assume any type of liability, in whole or in part, for damages (including, by way of example, damages for loss or lack of earnings, interruption of business, loss of information or other economic losses of any nature) arising from the use, in any form and for any purpose, of the data and information contained in this document.