Loading

Loading

Update as of July 30 – Industrial Metals Trends – July 2025

In July, the metals market showed a generally positive trend, especially in euros, thanks to the weakening of the European currency, which supported prices in local currencies.

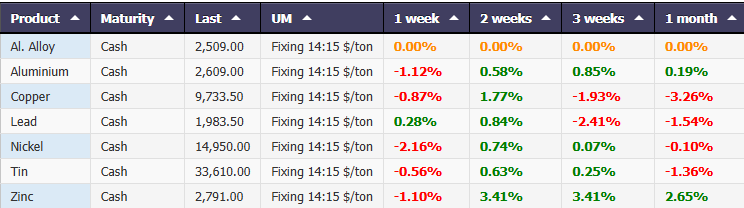

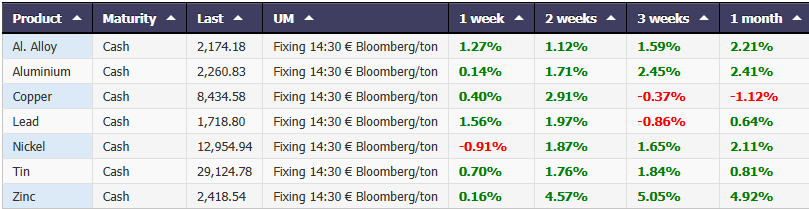

- Zinc was the best performer among base metals, with a +1.88% in USD and a significant +2.55% in EUR, supported by a strong recovery over the past three weeks.

- Primary aluminum showed a moderate monthly increase: +1.52% in USD and +2.19% in EUR, marking a steady recovery after a negative start.

- Tin gained 0.75% in USD and 1.42% in EUR, supported by stable demand in Asia.

- Lead had a mixed performance, closing at -0.86% in USD but almost unchanged in EUR (-0.21%).

- Copper remained weak, with monthly declines of -2.56% in USD and -1.92% in EUR, penalized by bearish sentiment and uncertain Chinese macroeconomic data.

- Nickel rose modestly +0.20% in USD and +0.86% in EUR, recovering slightly after a negative start.

Overall, euro-denominated metals outperformed dollar-denominated prices, a sign that the exchange rate effect played a decisive role in favor of European operators.

Performance Metals Cash $/ton – Powered by Commodity Evolution

Performance Metals Cash €/ton Bloomberg – Powered by Commodity Evolution

Copper – August Marked by Geopolitical Transition and Volatile Markets

The agreement announced on July 27 between Donald Trump and Ursula von der Leyen was supposed to bring clarity and stability to transatlantic trade relations, but in the case of copper, it has become a source of further ambiguity and disruption.

Contrary to initial expectations—which called for a 15% tariff cap on European copper—the official White House document confirmed that copper, steel, and aluminum exports will remain subject to punitive tariffs of 50%.

This inconsistency between political communication and actual content immediately fueled concern among European exporters, suggesting that copper, despite being listed among the EU’s strategic raw materials, is not among those classified as “critical” for the purposes of tariff exemptions.

The consequence was a rapid disruption of flows to the US, just as traders were attempting to anticipate the entry into force of the new measures on August 1st.

Collapse in Premiums and Uncontrolled Arbitrage

The impact on the physical market was immediate. The cif Rotterdam premium for Grade A copper fell from $185 to $167.50/ton in two weeks, highlighting depressed demand and a trading system on hold.

The most noticeable impact, however, was on the spread between the two main reference markets: the US CME and the London LME. The so-called arbitrage reached an all-time high of $2,600/ton on July 21, fueled by frenzied cathode purchases by US importers prior to the tariff crackdown.

At the same time, the US spot market exhibited chaotic behavior, with premiums fluctuating between $0.05 and $0.14/pound, depending on quantities and timing. Traders are talking about a “moving target,” where no price is reliable and any benchmark can be proven wrong the next day.

Grade A Copper Cathode – Rotterdam – Powered by Commodity Evolution

LME Copper 3 Month $/ton VS CME Copper 3 Month $/ton – Powered by Commodity Evolution

Marginal Europe, Central Asia: The Case of Scrap Copper

While European refined copper exports are suffering, US secondary copper (scrap) exports remain heavily skewed toward Asia. China absorbed 20.7% of US scrap between January and May 2025, despite a 53% drop in volumes compared to 2024.

EU countries, however, remain marginal (Belgium 5.2%, Germany 1.9%).

On the other hand, the US continues to import only from Canada and Mexico, which are not subject to the new measures. This means that European copper is excluded both as a supplier of refined copper and as a logistical alternative in the scrap sector, further exacerbating its trade marginalization.

A Collaboration Just for Show?

Despite the European Commission’s optimistic claims about a supposed “metals alliance,” the reality is that copper remains outside the tariff concessions list, making this alliance more rhetorical than operational.

The sector now finds itself in a state of “structural instability“: high tariffs, compressed premiums, rampant arbitrage, and undermined trade confidence.

As John Gross, author of The Copper Journal, has pointed out, the entire copper ecosystem—from futures prices to physical stocks—has entered a chaotic phase, devoid of any fixed points. The lack of certainty about trade rules, combined with operational volatility, risks hindering trade and investment decisions for weeks.

LME Copper – 3 month $/ton daily

August Outlook: High Volatility, Low Direction

August begins with a market that has not yet digested the regulatory shock. The confirmation of the 50% tariff has dampened the bullish expectations that had spread in the days preceding the announcement, but the impact on sentiment remains profound.

Traders have suspended a large portion of shipments to the US, while American operators are still clearing out early imports.

The price chart suggests a lack of clear directionality, with movements compressed within a congestion range between $9,600 and $9,850/ton. Downside pressures have not disappeared, but could be mitigated by physical shortages in Europe and a possible tightening of arbitrage with the CME.

With arbitrage at its highest and premiums declining, it is difficult to envision a significant rally barring sudden geopolitical events or a shock to the dollar.

Strategic Implications for European Industry

The European copper industry now faces three main challenges:

- Exclusion from the US market

With 50% tariffs, European exporters are losing competitive access to the US market, while countries like Canada are maintaining open channels. - Difficulties in transferring volumes

Demand in Asia is weak, Germany is slowing, and premiums are shrinking. Logistics options are limited and unresponsive. - Ongoing regulatory uncertainty

The ambiguity over what is considered “strategic” or “critical” in the EU classification also puts other metals at risk. Copper is a geopolitical test case for European industrial policy.

For traders and buyers, August will be the time to defend positions rather than take new ones. The most sensible strategy is to wait and see, paying attention to macroeconomic developments, CME-LME arbitrage, and European political reactions.

The promised stability has proven unstable. Copper, once again, is the barometer of global industrial geopolitics.

Price Target for August 2025 – LME Cash Copper (EUR/ton, with EUR/USD = 1.15)

Commodity Evolution is the ideal solution to support the budgeting and negotiation activities of the corporate purchasing department.

Access to the platform will allow you to view real-time prices at any time and a lot of information relating to the market of metals, steel, scrap and many other reference sectors, with more than 1,500 reference products.

Request a Free demo of our platform for one week

Disclaimer

This document has been prepared by Commodity Evolution. This document is intended for consultation by the subjects to whom it is addressed, and, in any case, is not intended to replace the personal judgment of the subjects to whom it is addressed. Although Commodity Evolution takes the utmost care in preparing this document and considers its contents to be reliable, it does not assume any responsibility for the accuracy, completeness and timeliness of the data and information contained or present on the resources and data used for the purposes of its preparation. Consequently, Commodity Evolution declines all responsibility for errors or omissions. The opinions, forecasts or estimates contained in this document are formulated with exclusive reference to the date of drafting of this document, and there is no guarantee that future results or any other future event will be consistent with the opinions, forecasts or estimates contained herein. Any information contained in this document may, after the date of drafting of the same, be subject to any modification or update, without any obligation to communicate such modifications or updates to those to whom this document has previously been distributed. This publication is provided to you for information and illustration purposes only, and does not constitute in any case an offer to the public of financial products or promotion of investment services and/or activities either towards persons resident in Italy or persons resident in other jurisdictions. Commodity Evolution, nor any of its directors, representatives or employees assume any type of liability, in whole or in part, for damages (including, by way of example, damages for loss or lack of earnings, interruption of business, loss of information or other economic losses of any nature) arising from the use, in any form and for any purpose, of the data and information contained in this document.