Loading

Loading

The most non ferrous metals show positive weekly changes, but with significant corrections over the medium term (3 weeks – 1 month). This indicates that the market is experiencing a technical rebound after a period of structural weakness, with mixed signals on the strength of real demand and the global macroeconomic outlook.

Metals Quoted in Dollars ($/ton) – Fixing 14:15 LME

Tin +4.84% (1 week) | -7.85% (3 weeks) | -10.95% (1 month) → After a marked slump in March, tin rebounds sharply in the last week, but the damage remains extensive. The recovery may reflect a mix of technical hedging and modest industrial reactivations.

Zinc +3.09% (1 week) | 0.87% (3 weeks) | -8.13% (1 month) → Technical rebound also for zinc, which however remains among the worst monthly performers in USD currency, a sign of supply-side pressure and slowdowns in Asian demand.

Nickel +0.16% (1 week) | +7.59% (3 weeks) | -1.69% (1 month) → Nickel in US dollar terms is showing a gradual recovery since mid-April, but is still unable to break through the psychological $16,000 threshold, blocked by strong technical resistance.

Lead +3.70% (1 week) | +5.26% (3 weeks) | -2.05% (1 month) → Lead in good shape, supported by demand for conventional batteries. Monthly losses are moderate.

Copper +2.87% (1 week) | +6.12% (3 weeks) | -3.81% (1 month) → Copper in technical recovery, but still fragile on a monthly basis. Market faces mixed macro data and volatile sentiment.

Primary Aluminium +3.11% (1 week) | +2.13% (3 weeks) | -1.41% (1 month) → Primary aluminium in US dollar terms is holding up well, benefiting from the green environment, but slightly down on a 1-month basis.

Performance Metals Cash $/ton Bloomberg

Metals Quoted in Euro (Euro/ton) – Fixing 14:15 Euro Bloomberg

These euro prices are also affected by the EUR/USD exchange rate, which can amplify or dampen metal movements relative to the LME fixing in euros.

Zinc +3.11% (1 week) | -2.59% (3 weeks) | -12.45% (1 month) → The sharpest decline in the euro currency basket. Despite a good weekly rebound, the monthly slump indicates strong weakness in the European market.

Tin +4.85% (1 week) | -11.01% (3 weeks | -15.14% (1 month) → Weaker than the dollar price: this suggests that the strengthening of the dollar has penalised the euro fixing, amplifying the drawdown.

Copper +2.89% (1 week) | +1.97% (3 weeks) | -7.74% (1 month) → Again, copper in EUR shows more pronounced weakness than the LME quote.

Nickel +0.18% (1 week) | +3.90% (3 weeks) | -6.16% (1 month) → Nickel in EUR also shows a larger monthly decline against the USD, a sign that the recent recovery was not enough to offset the initial April drop.

Primary aluminium +3.13% (1 week) | -1.37% 3 weeks) | -3.19% (1 month) → Similar dynamics to that seen in dollar, but with slightly larger monthly loss in euro.

Performance Metals Cash €/ton Bloomberg

Nickel Market: Between Temporary Surplus And Structural Deficit

The nickel market is now at an historic crossroads. After years of surplus and weak demand, profound challenges are on the horizon that could radically transform the global balance of supply and demand.

Geopolitical factors, new tax regimes in Indonesia, international trade tensions and the acceleration of the energy transition are set to redefine the strategic role of nickel over the next decade. In this complex scenario, investors, producers and end-users must prepare for increasing volatility and the risk of structural shortages.

Current Surplus, But a Crisis on the Horizon

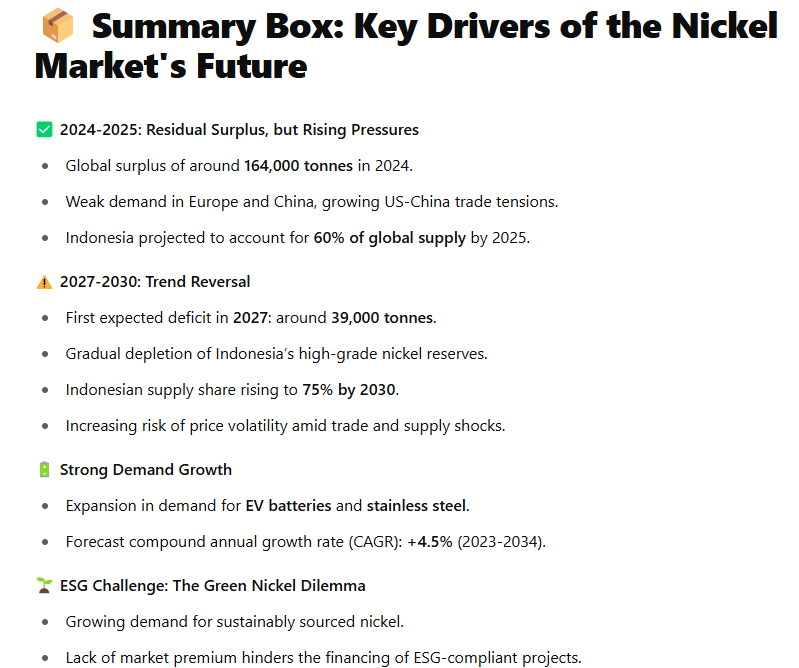

Today, the global nickel market still lives in a state of apparent abundance. According to the latest available data, 2024 closed with a surplus of around 164,000 tonnes, down from the all-time high of 179,000 tonnes reached in 2023. However, this surplus is gradually eroding, helped by demand that, while weak in Europe and China, remains solid in some industries.

Analysts warn that this surplus phase is set to come to an end within a few years. According to Mark Travers, CEO of Brazilian Nickel, the global market could face a deficit as early as 2027, with an estimated shortage of around 39,000 tonnes, which is set to expand rapidly to require more than half a million additional tonnes by 2034.

This imbalance will be the result of insufficient investment in new mining projects, demand driven by the electrification of transport and stainless steel production, and the progressive control of major production sources by a few countries.

Indonesia And China: The Dominance Of The Supply Chain

One of the main dynamics shaping the market concerns the growing hegemony of Indonesia and China in nickel production. Over the past decade, Indonesia has become the world’s largest nickel producer, relying on aggressive industrialisation policies and close cooperation with Chinese operators.

Already today, much of Indonesia’s production is bound by long-term contracts that favour Chinese operators, reducing the availability of ‘free’ nickel on the global market. By 2025, it is estimated that Indonesia will account for about 60% of world production, rising to 75% by 2030.

This dominance is based not only on mining, but also on increasingly developed local refining, geared towards value-added products such as ferronickel, nickel matte and nickel pig iron (NPI), which are crucial for the production of batteries and stainless steel.

However, there are also risks for Indonesia itself. According to Travers, the country’s high quality nickel reserves could be depleted in less than two decades, forcing the extraction of lower quality materials, with higher costs and greater environmental impacts.

New Royalty Policies in Indonesia: Impacts on Costs and Competitiveness

In this context, the Indonesian government announced a proposed royalty revision that could have a significant impact on the global market. Currently, the royalty for nickel ore is set at 10%, but the new structure envisages progressive rates up to 19%, depending on the market price.

For derivative products such as ferronickel, NPI and nickel matte, royalty increases between 5% and 7% are also planned. This system is intended to guarantee the state higher revenues in times of high prices, without unduly compromising the competitiveness of companies.

While these measures could strengthen Indonesia’s fiscal position, they also risk significantly increasing costs for producers, reducing operating margins and potentially slowing down new mining investments at a time when the world market would need to expand supply.

Demand Supported By Batteries And Stainless Steel

With supply becoming increasingly uncertain, demand for nickel is poised for robust growth. Despite the recent success of LFP (lithium-iron-phosphate) batteries, Travers believes that energy-dense, nickel-based batteries will continue to increase their market share, particularly in high-end electric vehicles and industrial applications.

He estimates that the compound annual growth rate of primary demand for nickel will be 4.5 per cent between 2023 and 2034. This increase will be driven not only by batteries, but also by stainless steel production, which today accounts for about 70 per cent of global nickel demand.

In other words, the energy transition and industrialisation in emerging countries will continue to support demand for this strategic metal, adding pressure to an already strained supply.

Regional Markets: US, Europe and China under Pressure

In the US, the new trade tariffs announced by President Donald Trump triggered slight upward pressure on nickel cathode premiums, which rose.

In Europe, premiums also rose. In Rotterdam, the premium on cathodes rose to EUR 340/tonne. In China, liquidity remained extremely tight, due to unfavourable import arbitrage penalising imports of refined nickel. All this contributes to an unstable equilibrium picture: while the global surplus still covers demand, any shock (tariffs, supply restrictions, geopolitical tensions) could quickly alter the price balance.

Nickel Brichette Premium – Rotterdam euro/ton – Powered by Commodity Evolution

Challenges For Sustainability: The ‘Green Nickel’ Dilemma

A topic of growing importance is ‘green nickel’, i.e. nickel mined and processed with high environmental and social standards. However, the market has not yet adequately rewarded these practices, and most contracts still only focus on price, not sustainability.

This presents a challenge for Western mining projects, which rely on ESG responsibility to differentiate themselves from Asian production. Without long-term contracts that recognise the added value of green nickel, many projects risk remaining financially unsustainable, further exacerbating the risk of future shortages.

Detailed Forecast – LME Nickel at 3 Months $/tonne | May 2025

Detailed Forecast – LME Nickel at 3 Months $/tonne | May 2025

The end of April 2025 for nickel presents a market in a settling phase, following the recovery in the second half of April. Prices have rebounded from lows in the $13,800/mt area, reaching and stabilising around $15,600-15,700/mt. However, the most recent technical elements suggest that the rebound may have petered out in the short term.

Two key barriers delimit the price trajectory:

- The SMA 50 (50-day simple moving average), currently at $15,734/mt, serves as the first short-term dynamic resistance;

- The SMA 200, at $15,999/mt, represents medium-term strategic resistance, which has not been breached in months and has repeatedly rejected breakout attempts.

In the meantime, the MACD (Moving Average Convergence Divergence), while remaining above zero, is slowing down, with a decreasing divergence between the two lines (MACD and Signal Line) and a histogram that tends to compress: a classic sign of positive momentum that is losing strength.

LME Nickel – 3 month $/ton daily

Base scenario: Cautious lateralisation between $15,200 and $15,900/mt

In the short term, the technical setup and the lack of concrete macro catalysts suggest a continuation of the sideways consolidation, with contained fluctuations between:

- Key technical support at $15,200/mt;

- Technical resistance zone between 15,800 and 15,900 $/ton.

This range could hold for most of the month, with markets waiting for fundamental developments, such as:

- Confirmation of new Indonesian royalties on matte and ferronickel;

- News on the US-China trade front or tariff decisions;

- China import/export data and LME stocks.

IIn the absence of surprises, prices could therefore stagnate in this channel, with isolated volatility spikes but no decisive breaks.

Commodity Evolution is the ideal solution to support the budgeting and negotiation activities of the corporate purchasing department.

Access to the platform will allow you to view real-time prices and a wealth of information on the market for metals, steel, scrap and many other sectors at any time, with more than 1,500 reference products.

Request a no-obligation One-week free demo of our platform

Disclaimer

This document has been prepared by Commodity Evolution. This document is intended for consultation by those to whom it is addressed, and, in any event, is not intended to replace the personal judgment of those to whom it is addressed. Although Commodity Evolution has taken the utmost care in the preparation of this document and considers its contents to be reliable, Commodity Evolution nevertheless assumes no responsibility for the accuracy, completeness and timeliness of the data and information contained in or present on the resources and data used for the purpose of its preparation. Accordingly, Commodity Evolution disclaims all liability for errors or omissions. The opinions, forecasts or estimates contained in this document are made with reference only to the date of preparation of this document, and there can be no assurance that future results or any future events will be consistent with the opinions, forecasts or estimates contained herein. Any information contained in this document may, subsequent to the date of preparation of this document, be subject to any changes or updates, without any obligation to notify those to whom this document was previously distributed of such changes or updates. This publication is provided to you for information and illustration purposes only and in no way constitutes an offer to the public of financial products or promotion of investment services and/or activities either to persons residing in Italy or to persons residing in other jurisdictions. Commodity Evolution, nor any of its directors, representatives or employees assumes any liability whatsoever, in whole or in part, for any damages (including, without limitation, damages for loss or loss of profits, business interruption, loss of information or other economic loss of any nature whatsoever) arising out of the use, in whatever form and for whatever purpose, of the data and information contained in this document.