Loading

Loading

China has decided to suspend exports of a wide range of critical minerals and high-performance magnets in an escalation of trade tensions with the United States. The news, reported by the New York Times late Sunday evening, highlights Beijing’s intention to strike hard at strategic industry sectors such as electric vehicles, semiconductors, defense and aerospace.

The measure comes in response to the tariff increase announced by former U.S. President Donald Trump, which has reignited the trade conflict between the world’s two major economies. Beijing, therefore, is counterattacking where it is strongest: in the control of rare earths and high-tech materials.

Tightening Controls On Six Heavy Rare Earths And Strategic Magnets

Earlier this month, China had already announced new export controls on six heavy rare earth metals, materials critical to the production of special magnets used in electric motors, drones, robots, missiles and spacecraft. These are key components for national security and the energy transition, areas in which Beijing holds a global leadership position.

In addition to minerals, Beijing has also decided to limit direct exports of the magnets themselves, which China dominates with a 90 percent share of global production. While these magnets represent a marginal fraction of China’s total exports, they are essential to many technology-intensive industries, making the move extremely significant strategically.

Limited Effects For China, But Strong Pressures On Trade Partners

According to the New York Times, the direct damage to China will be limited, as rare earth magnets represent a marginal share of its overall exports. However, the impact will be much more severe for its major trading partners, including the United States, Japan and Germany, which are heavily dependent on Chinese imports of these critical materials.

Chinese Ports Block Shipments: Toward a New, More Restrictive Regulatory Framework

Since the announcement of the new measures, several Chinese ports have suspended shipments of magnets and rare earths, pending the finalization of a new regulatory framework by the central government.

According to reports, the regulation being finalized could result in the permanent exclusion of some companies from access to these materials, particularly those linked to U.S. defense or U.S. military contractors.

This blockade is disrupting the supply chain in crucial sectors, just as the United States announced some tariff exemptions for electronic products. However, rare earth-based components still remain subject to the restrictions, exacerbating the situation.

Delays In Export Licenses And Risk Of Stock Depletion

According to analysts and industry representatives, the delay in issuing export licenses could last at least 45 days, a period long enough to cause global stocks of these critical materials to be depleted, especially in the West. Companies involved in robotics, drones, advanced electronics and defense are likely to experience serious production delays.

Daniel Pickard, chairman of the Advisory Committee on Critical Minerals at the Office of the United States Trade Representative and the U.S. Department of Commerce, told the New York Times, “Blocking or controlling exports will definitely have a severe impact on the United States.”

Future Of Defense Depends On Critical Materials: MP Materials’ Warning

James Litinsky, CEO of MP Materials, the only U.S. company with an active rare earth mine and refining plant in the United States, sounded an alarm: “Drones and robotics represent the future of warfare. And based on what we are seeing, critical materials needed for this supply chain are currently locked up.”

These statements highlight how U.S. industrial and technological sovereignty is heavily exposed to dependence on China, particularly for strategically important materials.

Japanese Stocks More Resilient, But West Is Vulnerable

While some Japanese companies seem relatively ready for the shock, thanks to strategic inventories built up over a year of operation, many U.S. firms are instead operating with minimal reserves.

This strategy, designed to free up working capital, is now proving risky, making many industries vulnerable to supply chain disruptions.

The impact of Chinese restrictions also extends to Germany and Japan, two of the largest users of rare earth magnets in the industrial and electronics sectors. Companies in these countries, while more prescient in their inventory management than those in the United States, still cannot escape rising costs and commercial pressure.

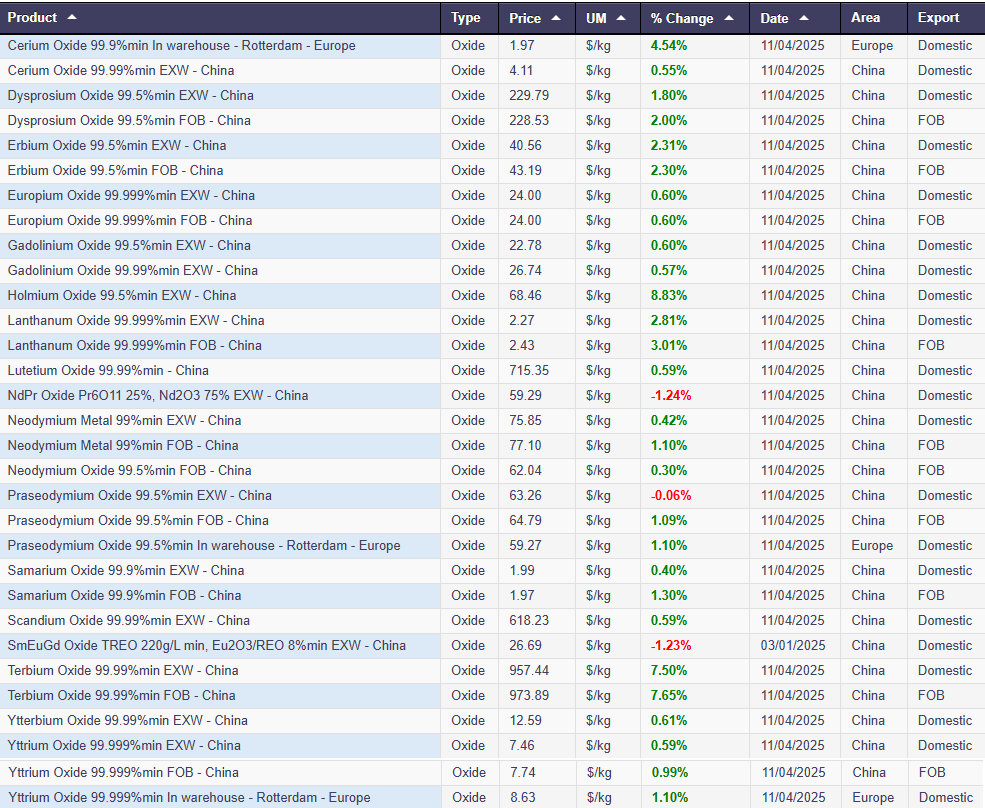

Skyrocketing Prices For Critical Metals: Dysprosium Boom

One of the first tangible consequences of the restrictions has been the soaring prices of materials under control. Dysprosium oxide, one of the key rare earths for high-performance magnets, reached about $230 per kilogram in Shanghai.

Dysprosium OX 99.5% min EXW – China $/kg – Powered by Commodity Evolution

But outside China, prices are rising even faster due to uncertainties over access and supply. This trend is a further blow to Western manufacturing companies, which are now facing rising costs at a time when margins are already under pressure from ongoing trade wars.

Leopard-Spotted Enforcement: Disparity in Controls Among Chinese Ports

According to reports in the New York Times, enforcement of restrictions is uneven among different Chinese ports. Some ports of call appear to allow magnets with minimal traces of heavy rare earths to leave, while others require strict controls to verify full compliance with the new regulatory framework.

This uneven approach is fueling confusion among exporters and international customers, creating customs delays and uncertainty in trade contracts.

Rare Earth Oxide $/kg – Powered by Commodity Evolution

Ganzhou And Jiangxi: Strategic Nodes Of Chinese Supremacy In Rare Earths Rare

China’s dominance in the rare earths sector is not limited to the possession of mineral resources alone, but extends along the entire value chain, from refining to the production of advanced components. This primacy is rooted in two key geographic pillars:

- Jiangxi province, rich in heavy rare earth deposits;

- The city of Ganzhou, considered the heart of global high-performance magnet production.

It is in Ganzhou that strategic companies such as JL Mag Rare-Earth, a direct supplier to electric car giants such as Tesla and BYD, operate. The ability of these companies to transform raw materials into advanced magnets for electric motors is an unattainable competitive advantage for many other industrialized countries.

A Strategic Dependence That Triggers the Race to Diversification

The current situation has reignited the debate on the need for the West to diversify its sources of supply. But building an alternative supply chain-from mining to magnetization-requires years of investment, technological know-how, and political support. Currently, no Western country has a complete supply chain that can compete with China.

In this scenario, Beijing shows it is ready to use its technological-industrial leadership as geopolitical leverage, blocking access to materials the world increasingly needs.

Conclusion: Trade War Enters the Era of Strategic Minerals.

China’s restrictions represent a new level of intensity in the global trade war, shifting the conflict from tariffs on consumer goods to contention over control of critical future resources. Drones, electric cars, robotics, defense-all strategic sectors of modern industry rest on materials that, for now, remain firmly in Beijing’s hands.

The United States and its allies are now called upon to respond: reorganizing their supply chains, increasing strategic inventories, promoting domestic mining research, and forging alliances with alternative suppliers will be mandatory steps if they are not to remain hostage to this new dependence.

Detailed timeline of Chinese restrictions on rare earths from 2010 to the present, with focus on key events, strategic motivations, and geopolitical impacts:

2010 – Informal Embargo Toward Japan

- Event: China informally blocks rare earth exports to Japan after a diplomatic clash over disputed islands in the East China Sea;

- Rationale: Geopolitical pressure and response to a maritime incident;

- Impact: First real “trade weapon” used by Beijing in the rare earths sector. Japan begins to diversify supplies.

2011 – Official Export Quotas And Export Licenses

- Event: Beijing introduces official export quotas and a strict licensing system;

- Rationale: Officially to protect the environment and manage finite resources. Unofficially, to consolidate control over the value chain;

- Impact: Explosion in global prices. Rare earth research boom outside China (e.g., Molycorp in the U.S.).

2012 – Recourse to WTO By U.S., European Union And Japan

- Event: Major trading partners sue China at the World Trade Organization (WTO) for discriminatory trade practices;

- Reason: Allegations of violating free trade rules;

- Impact: Initiation of international legal dispute over control of strategic raw materials.

2014 – Defeat Of China At WTO And Removal Of Quotas

- Event: WTO condemns China, declaring restrictions illegal;

- Consequence: Beijing is forced to remove quotas and liberalize exports;

- Alternative Tactic: Tightening environmental controls and domestic consolidation of the industry.

2017 – Domestic Consolidation And Increased Environmental Control

- Event: China launches a campaign to combat illegal mining, shutting down dozens of unauthorized mines and refineries;

- Rationale: To rationalize the industry, improve environmental reputation, and increase production quality;

- Impact: Decreased overall supply and increased dependence on Chinese licensed suppliers.

2019 – Threat To Suspend Exports To The United States

- Event: During the tariff war with the Trump administration, China openly threatens to halt rare earth exports to the US;

- Rationale: Retaliation for U.S. duties on Chinese technology and industrial goods;

- Impact: Increased strategic tensions. U.S. begins funding domestic mining and refining (e.g., MP Materials).

2021 – Tightening Rules For Export Of Technology Related To Rare Earths

- Event: Beijing implements new restrictions on rare earth separation and refining technologies;

- Rationale: Protection of national expertise and strategic control over know-how;

- Impact: Difficulty for new Western entrants, who struggle to replicate Chinese refining.

2023 – Creation Of A Single National Holding Company: China Rare Earth Group

- Event: Merger of three state-owned giants to create a public monopoly giant;

- Rationale: Consolidation of the entire rare earth industrial chain into a single Beijing-controlled entity;

- Impact: Greater coordination and ability to globally influence prices, volumes, and strategies.

2024 – First Restrictions On Critical Metals Like Gallium And Germanium

- Event: China introduces limits on exports of gallium and germanium, used in chips, lasers and military devices;

- Rationale: Retaliation for U.S. restrictions on semiconductor exports to China;

- Impact: Alarm among Western hi-tech companies and in defense sectors.

2025 – Blockade Of Heavy Magnets And Rare Earths And New Customs Controls

- Event: Beijing suspends exports of a wide range of heavy magnets and rare earths, imposing new export controls and clearances;

- Rationale: Retaliation against the Trump administration’s increase in U.S. tariffs;

- Impact: Supply chain disruptions in electric cars, drones, semiconductors and defense. Sharply rising global prices.