Loading

Loading

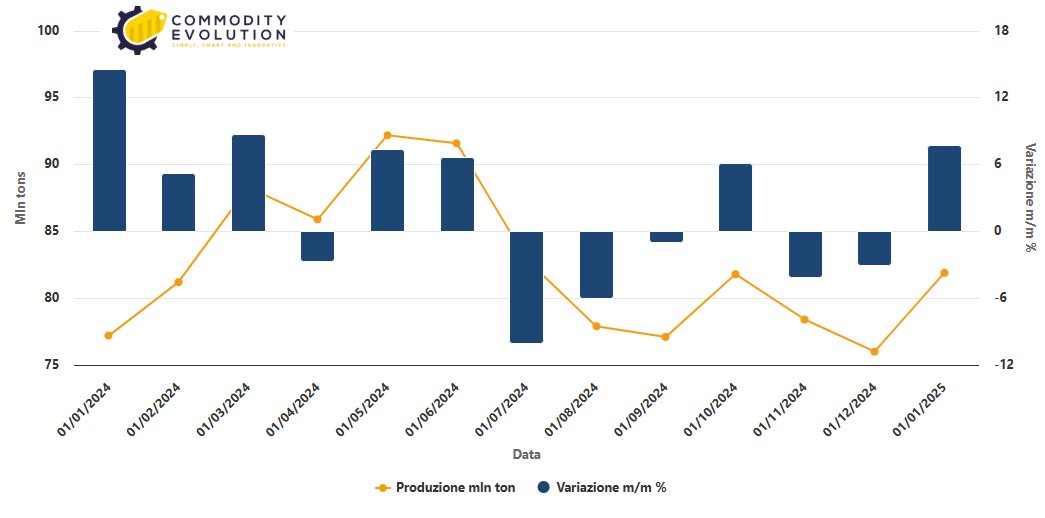

The World Steel Association (worldsteel) has released the report on global crude steel production for January. According to the released data, global production reached 151.4 mln tons, registering a 4.6 percent increase over the previous month.

However, on a year-on-year basis, it shows a decline of 4.4 percent, a sign of an economic and production environment that is still settling down.

World Crude Steel Production – Powered by Commodity Evolution

Production in Asia: Generalized Decline, Growth for India

Asia, the main steel production area globally, recorded a 4.5 percent decrease in production compared to January of the previous year, reaching a total of 112.3 million tons.

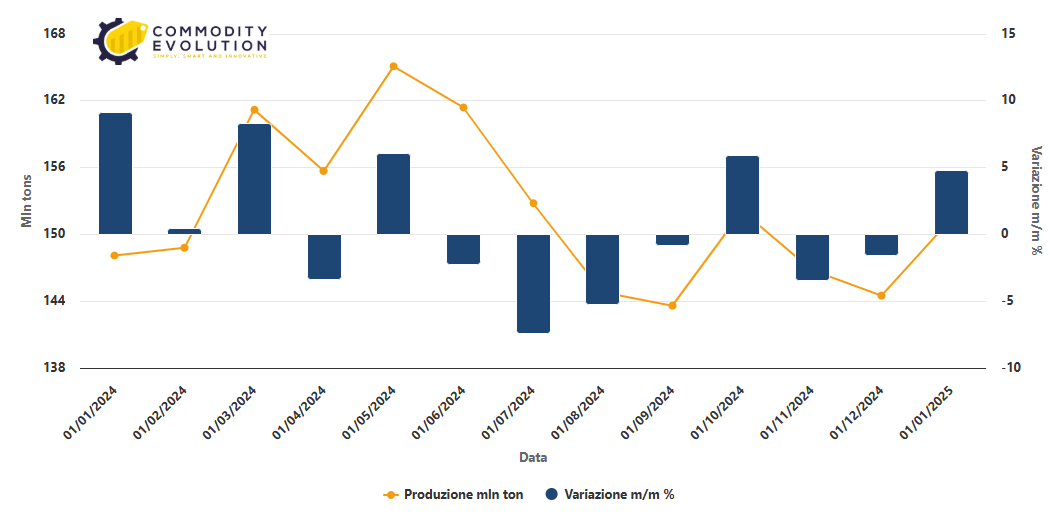

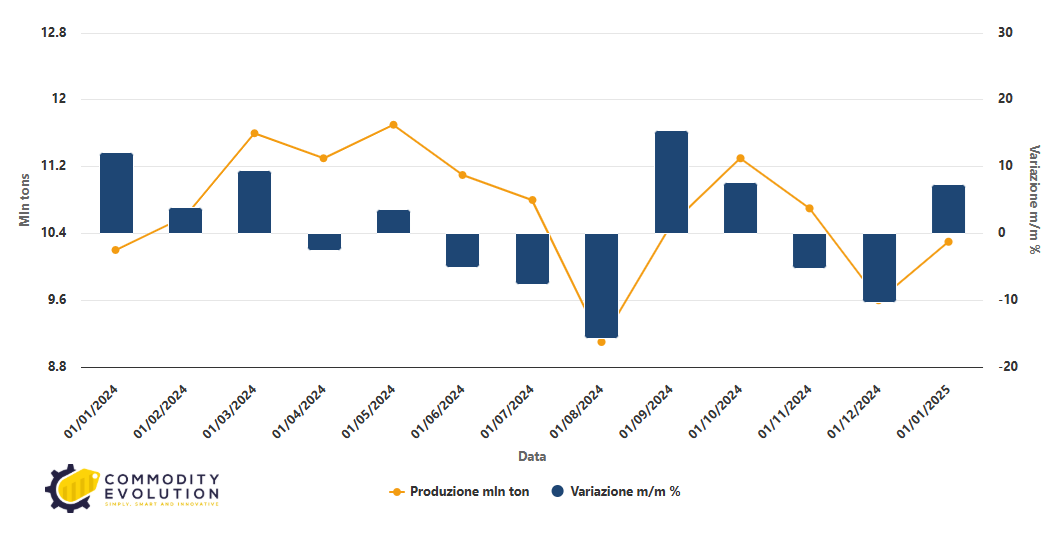

- China: China’s production, which accounts for the most significant share of global output, declined 5.6 percent year-on-year, stopping at 81.9 million tons. This decline is attributable to a number of factors, including reduced domestic demand, government-imposed environmental restrictions, and moderate post-pandemic economic recovery.

China Crude Steel Production – Powered by Commodity Evolution

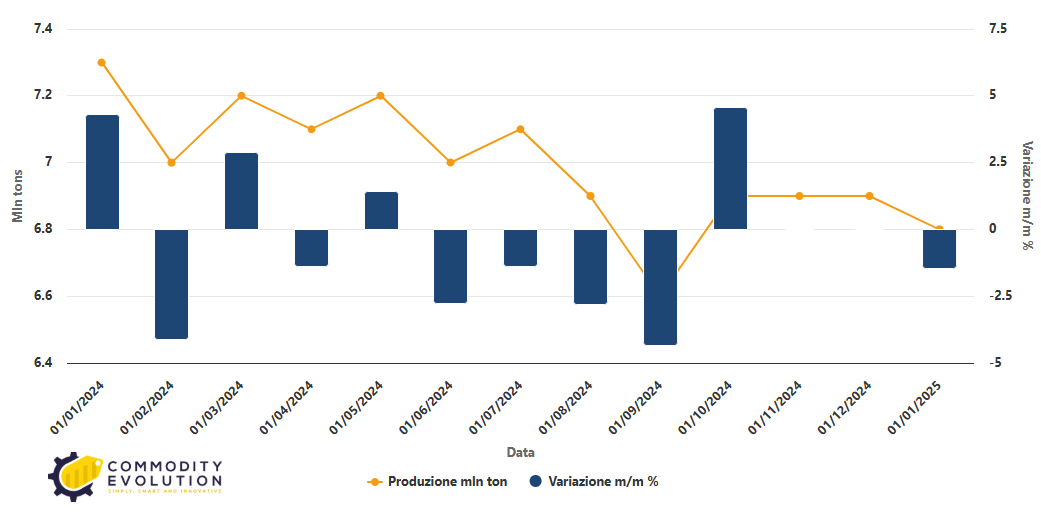

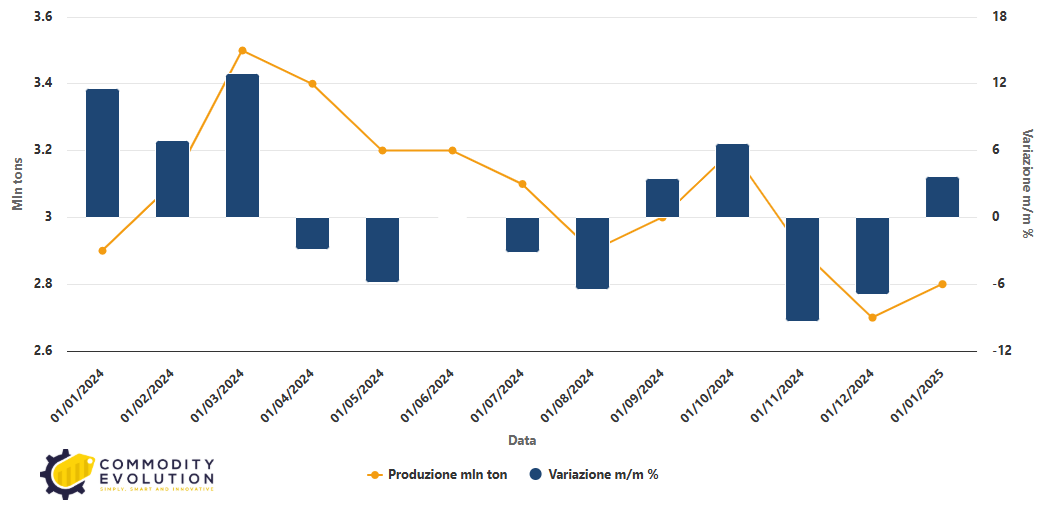

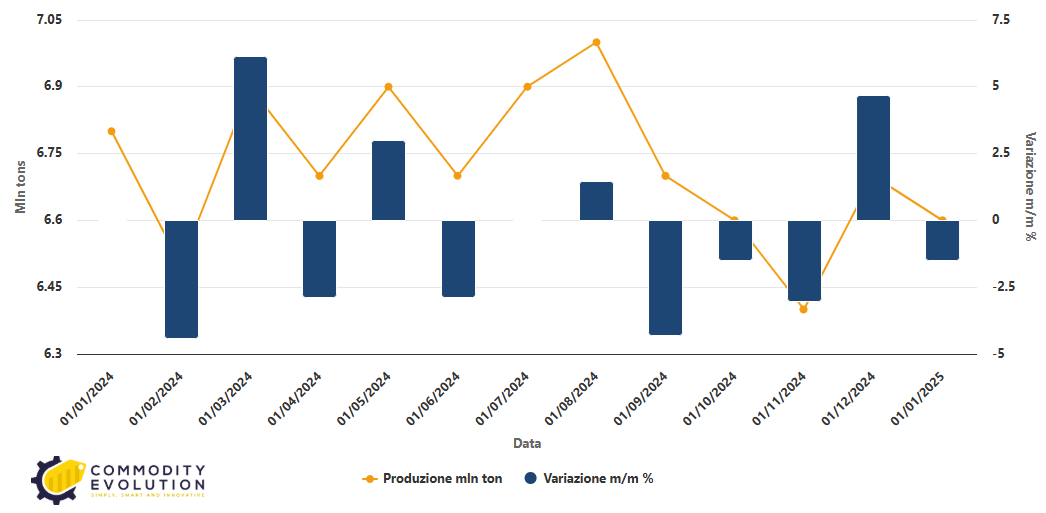

- Japan: Japanese production fell 6.6 percent from January 2024 to 6.8 million tons. Japan’s steel sector continues to suffer from global competition and decreased demand from the automotive and construction industries.

Japan Crude Steel Production – Powered by Commodity Evolution

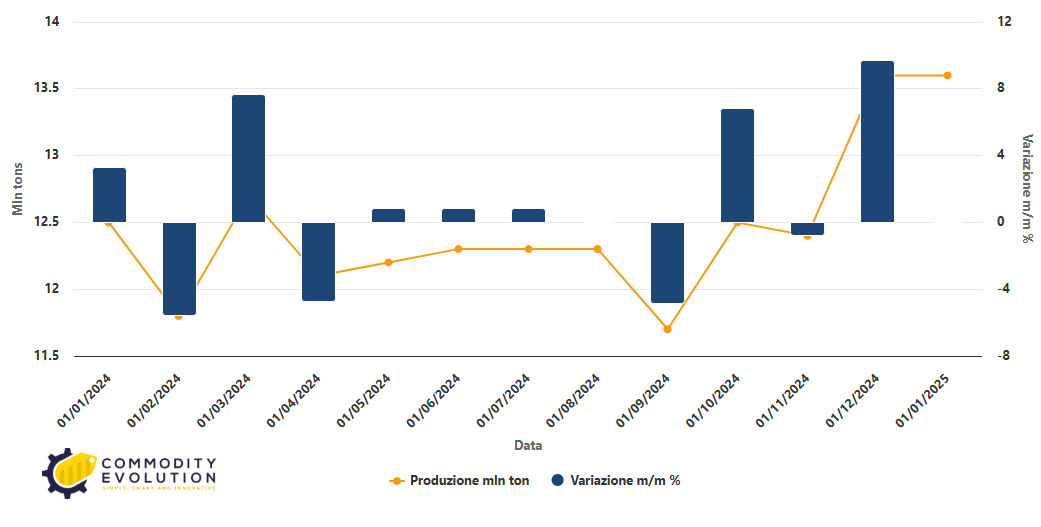

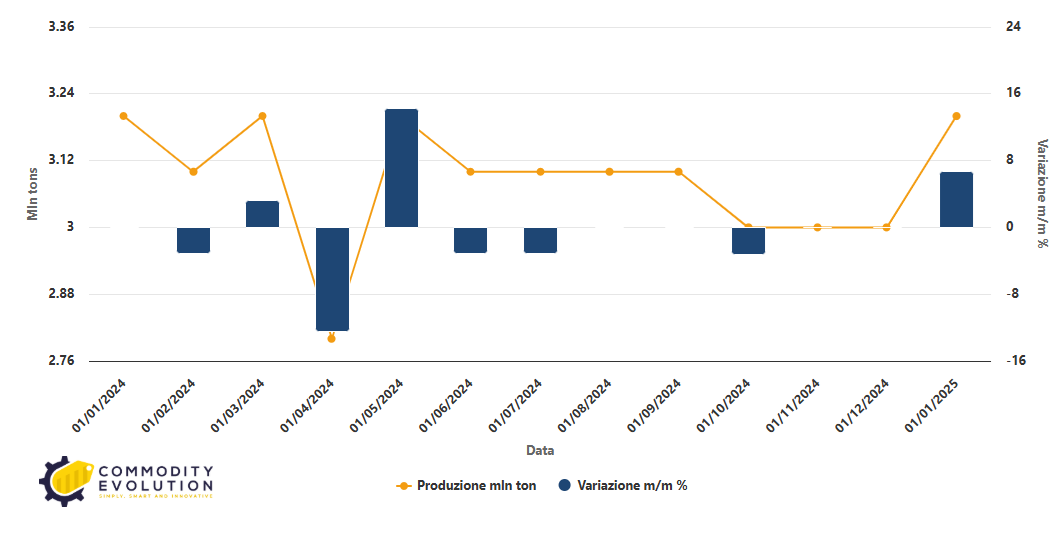

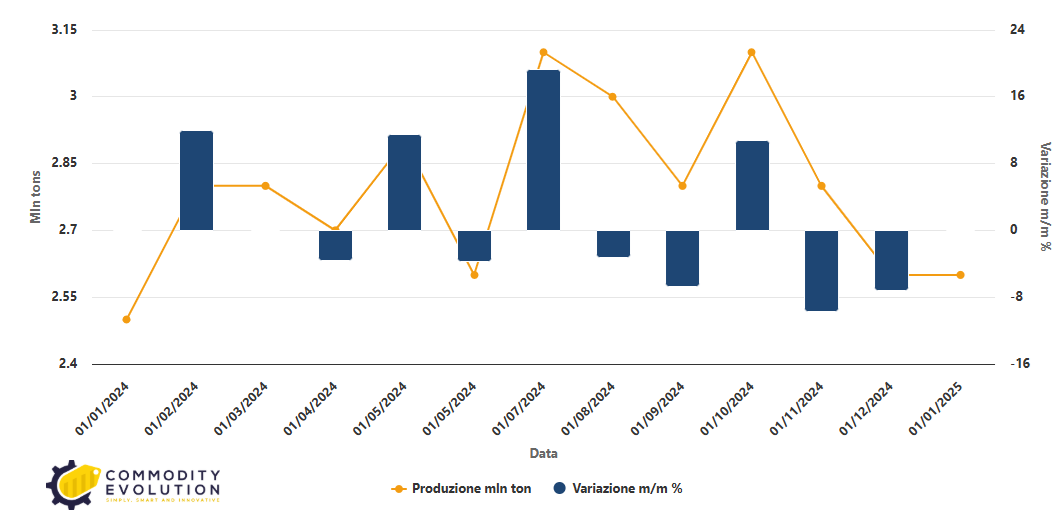

- India: Bucking the trend of other Asian countries, India recorded 6.8 percent year-on-year growth, producing 13.6 million tons. This increase was boosted by sustained infrastructure investment and increased domestic demand.

India Crude Steel Production – Powered by Commodity Evolution

- South Korea: South Korean production declined significantly by 8.8 percent to 5.2 million tons. This result reflects a contraction in exports and a slowdown in industrial activities.

European Union: Production Down with Germany in Difficulty

European Union (EU-27) countries recorded a total production of 10.3 million tons of crude steel in January, down 3.3 percent from the same month a year earlier.

EU-27 Crude Steel Production – Powered by Commodity Evolution

- Germany: Europe’s largest economy showed an 8.8 percent decline, stopping at 2.8 million tons. The crisis in the manufacturing sector, rising energy costs and reduced domestic and foreign demand contributed to this contraction.

Germany Crude Steel Production – Powered by Commodity Evolution

Turkey and CIS: Between Decline and Moderate Growth

- Turkey: Turkey’s steel sector declined 1.2 percent, with production at 3.2 million tons. Turkey is facing economic difficulties, including high inflation and reduced exports.

Turkey Crude Steel Production – Powered by Commodity Evolution

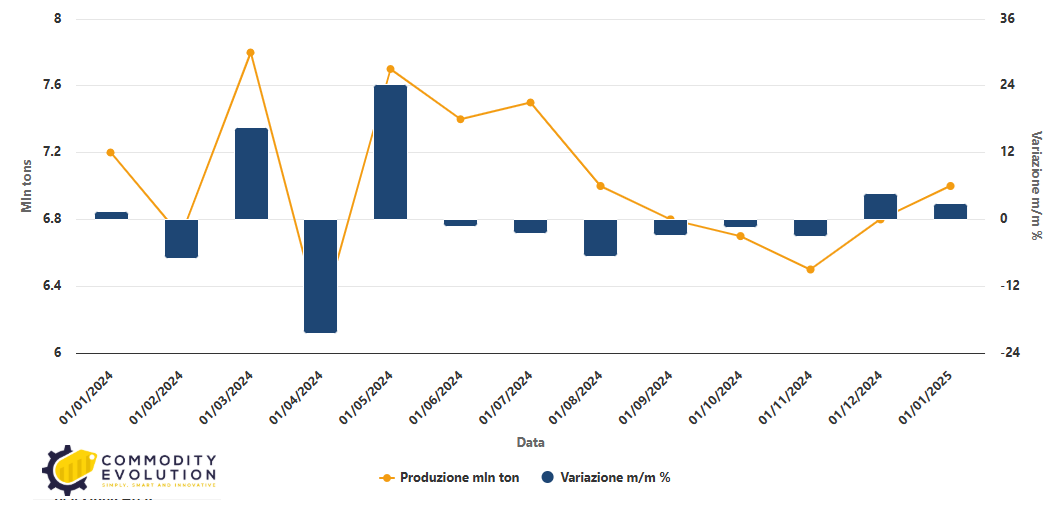

- Commonwealth of Independent States (CIS): Production in the CIS increased 1.4 percent year-on-year to 7 million tons. However, within the area, Russia saw a slight contraction of 0.6 percent, with an estimated production of 6 million tons. This result is influenced by economic sanctions and logistical difficulties related to the geopolitical environment.

C.I.S. Crude Steel Production – Powered by Commodity Evolution

North and South America: Different Trends between the United States and Brazil

- North America: Overall production decreased by 0.5 percent to 9 million tons.However, the United States recorded a slight increase of 1.2 percent to 6.6 million tons of production. The U.S. market is benefiting from steady demand in the construction and infrastructure sector.

US Crude Steel Production – Powered by Commodity Evolution

- South America: Production dropped significantly by 9.8%, stopping at 3.2 million tons. Brazil, the region’s main producer, suffered a 4.5 percent drop to 2.6 million tons. Economic difficulties and reduced external demand weighed on the sector’s performance.

Brazil Crude Steel Production – Powered by Commodity Evolution

Africa and the Middle East: Significant Contractions

- Africa: Crude steel production decreased 3.5 percent year-on-year to 1.9 million tons. The African steel sector continues to be affected by economic and infrastructure instability.

- Middle East: The region experienced a 15.3 percent decline, with total production at 4.2 million tons. Lower domestic demand and unstable trends in the raw materials market contributed to this contraction.

An Evolving Sector

Data on crude steel production in January reflect a global context still characterized by economic uncertainties and structural difficulties.

While some countries, such as India and the United States, are showing signs of growth, other economies, including China, Germany and Brazil, are facing significant challenges. The steel industry remains a key sector for global economic development, and its evolution will be closely linked to macroeconomic factors, trade policies and infrastructure investment in the coming months.