Loading

Loading

Global tin supplies could face problems later this year as the Wa region of Myanmar, which contributes 10 per cent of the world’s concentrate supplies of the metal, has decided to suspend mining operations ‘until mature mining conditions are present’ from August.

Global tin supplies could face problems later this year as the Wa region of Myanmar, which contributes 10 per cent of the world’s concentrate supplies of the metal, has decided to suspend mining operations ‘until mature mining conditions are present’ from August.

Myanmar’s suspension of tin mining in the Wa region from August 2023 is expected to put pressure on global supplies and drive up prices in the short to medium term.

According to the International Tin Association (ITA), Wa is an important tin mining district in Myanmar. It supplies a significant portion of concentrate for China, the world’s largest producer of refined tin.

In 2022, almost two-thirds of China’s imported tin concentrate came from Myanmar, totalling 48,000 tonnes. About 40,000 tonnes came from Myanmar’s mining production, with Wa’s contribution estimated at 70%.

Myanmar’s largest armed ethnic group controls the tin mining area. Myanmar has the third largest tin reserves in the world, after China and Indonesia. China is particularly dependent on Myanmar’s tin ore.

Therefore, Myanmar’s tin production is expected to decline by 30% year-on-year in 2023, down to 28 mt from 40 mt in 2022.

In the medium term, Myanmar could focus on domestic tin valorisation, following a growing trend among emerging markets globally. In the long term, Myanmar is expected to remain a significant producer of tin in the region, although political uncertainty will add downside risks to production volume.

The outlook for tin supplies was aggravated by the fact that Indonesia, the largest exporter of refined tin, considered an export ban to encourage the building of downstream processing capacity.

The ITA stated that an additional 8,000 tonnes of tin was taken from Wa’s stockpile last year when prices of the metal soared to historic highs.

A document on the suspension of mining explains the reasons for this move as a step to formalise mining. “… we could expect some restriction of supply until this is achieved”. Mines with existing licences will have three months to adapt to the new requirements,’ the ITA said.

The supply uncertainties come at a time when financial services firm Macquarie forecasts a market surplus of 5,000 tonnes, while global demand is expected at 3,62,000 tonnes.

On the other hand, analysts see demand for tin, especially from the semiconductor industry, being affected by the economic slowdown and reduced consumer spending on electronic products.

According to analysts, supplies could increase from Peru and Congo and could limit the impact of the suspension of mining activities in Wa.

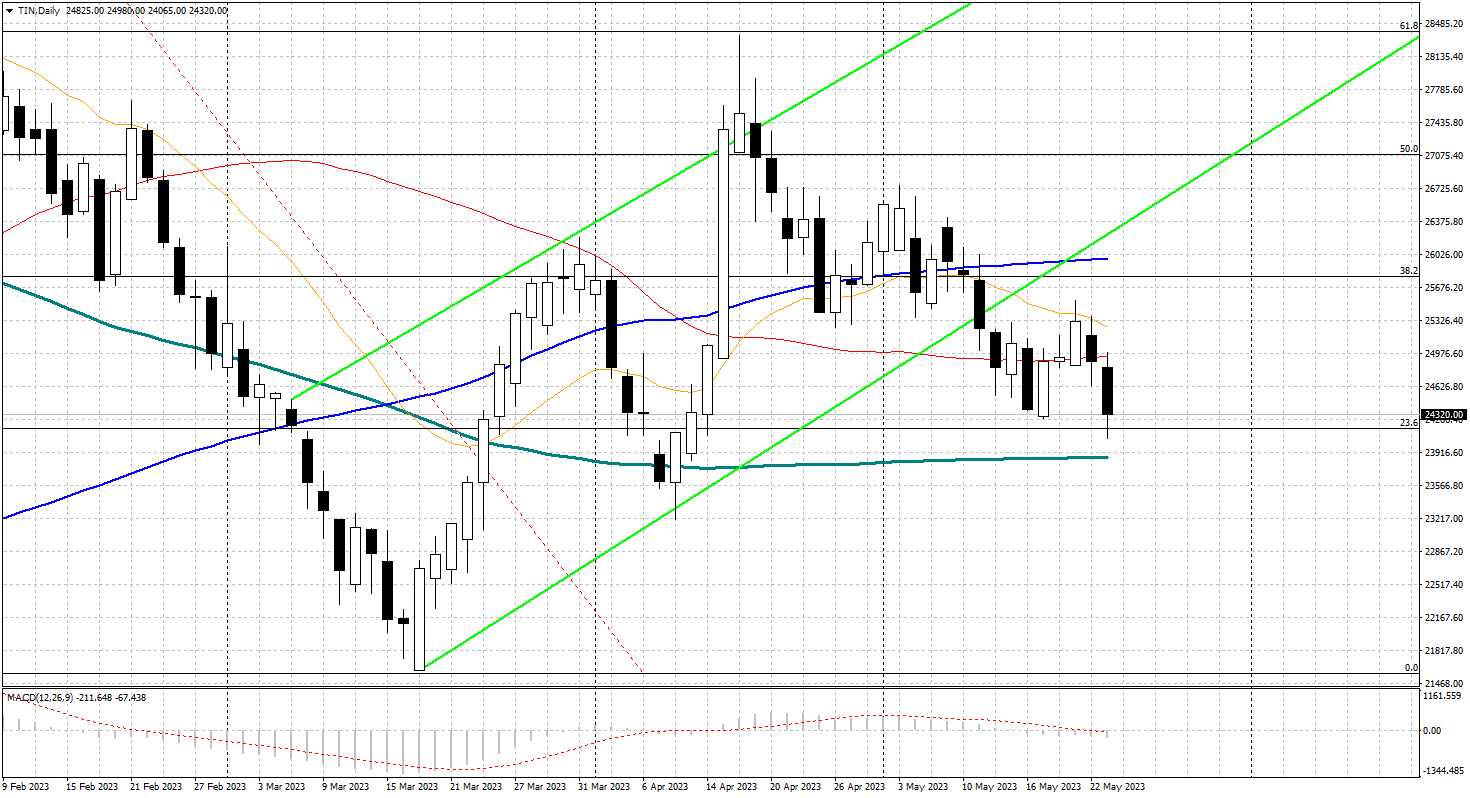

Tin prices stood at $24,370 a tonne (09:50 Italian time), below the two-month high of $28,000 recorded on 18 April after news of the Wa region’s development.

On the Shanghai Futures Exchange, the June tin futures contract fell to 197,450 Chinese yuan ($28,072) per tonne on Monday.

Tin – 3 month $/ton daily