Loading

Loading

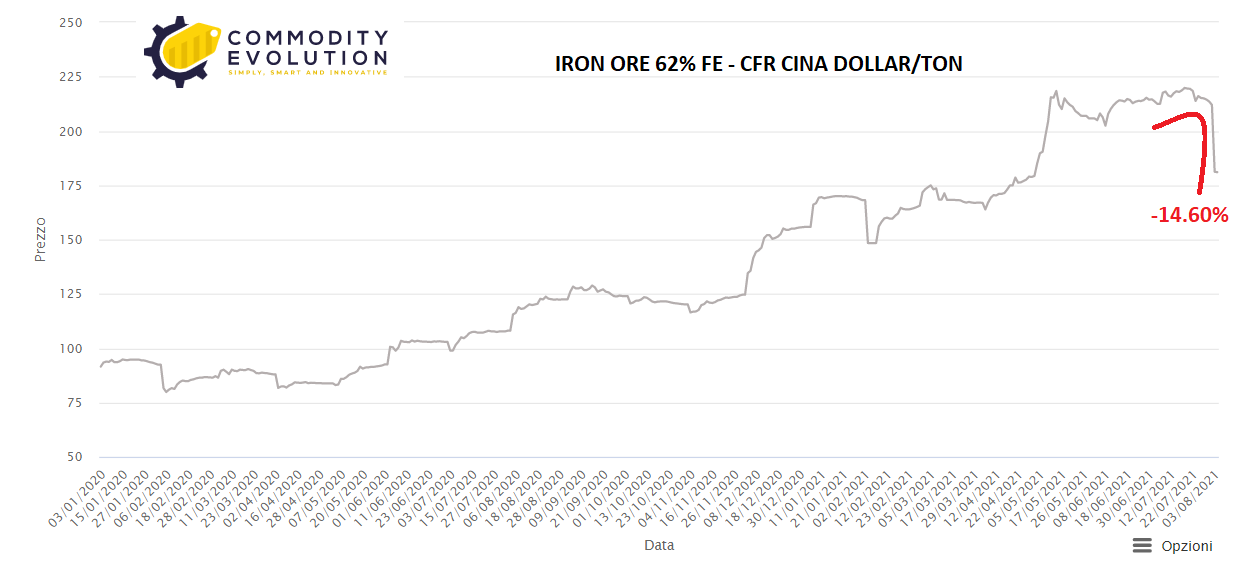

In August, it will be difficult to see much growth in Chinese iron ore demand when most steel mills are under pressure to control steel production.

This month, any increase in domestic steel production from newly added capacity will also be quite limited. Meanwhile, the strong pressure from the central government to reduce steel production until the end of the year is expected to further decrease the output of steel mills.

On the other hand, steel production could still be supported by improving steel margins if steel prices remain high. As a result, iron ore demand is expected to remain essentially flat compared to July.

Daily production of molten iron declined further last month: total volume at the 247 blast furnace mills surveyed nationwide averaged 2.33 million tons per day from July 2-29, down about 40,675 t/d from the June 4-July 1 average volume.

The decline was mainly due to the fact that blast furnace operations at some steel mills in northern China were temporarily suspended around July 1 for the celebration of the 100th anniversary of the founding of the Chinese Communist Party.

Then, in response to Beijing’s pledge to reduce domestic steel production from the 2020 level, many provinces began asking local steel mills to reduce production during this six-month period. This has seen many steel mills revise their steel production plans for the coming months, with some even starting to cut production quickly as demand for steel in the summer is low anyway.

As for ore supplies this month, some increase in iron ore shipments to China from both Australia and Brazil is expected. Domestic production of iron ore concentrates may also recover, with mining operations gradually resuming at some mines in North China’s Shanxi Province and elsewhere.

Most underground iron ore mining operations were halted in July after an accident at a local underground iron ore mine on June 10.